What is your answer to the question: How close are we to full capital liquidity?

It has to depend on which countries are involved, what time frame, etc. Entitled “Measuring Financial Integration:

More data, more countries, more expectations”Hiroshi Ito and I tackle the problem of liquidity and fungibility (Frankel’s terminology) by relying on a key decomposition:

items in [square bracket] and <尖括號> Relevant to the question of why the interest rate adjusted for the expected exchange rate is different. Frankel (1983) defines zero coverage spread as perfect capital liquidity and zero exchange rate risk premium as perfect capital substitutability, and I retain this terminology and the associated decomposition for this discussion.

Covering spreads used to be attributed to the presence or threat of capital controls being imposed. More recently, they may arise (in the real world) due to frictions caused by capital requirements and other regulations, associated liquidity issues, and default risks. The exchange rate risk premium—the deviation between forward discounting and expected depreciation—is associated with the risk of holding money and was modeled early on as a covariance of returns to wealth, or more recently (1990s) to consumption Growing return covariance.

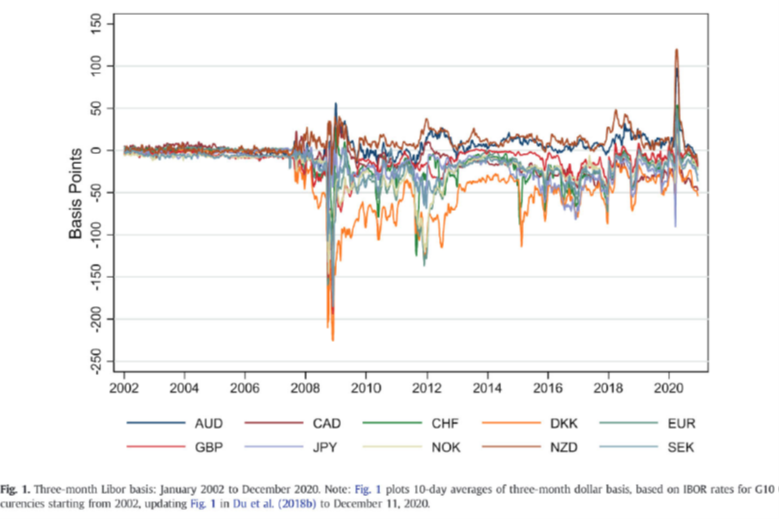

By the criteria of holding at par, liquidity appears to have declined after the GFC, as shown in this chart by Cerutti et al. express.

figure 1: Covers interest differential, basis points. Source: Cerutti et al. (2021).

While financial capital is now less free to move, it is important to understand that to some extent this development has been intentional; that is, the deviations in recent years have been partly driven by The likelihood of a crisis arising from capital requirements (see Wu and Schleger, 2021).For emerging markets where six different factors come into play, see the author’s paper Guy Kez and Ozildeham (2021), JIFMIM 2023).

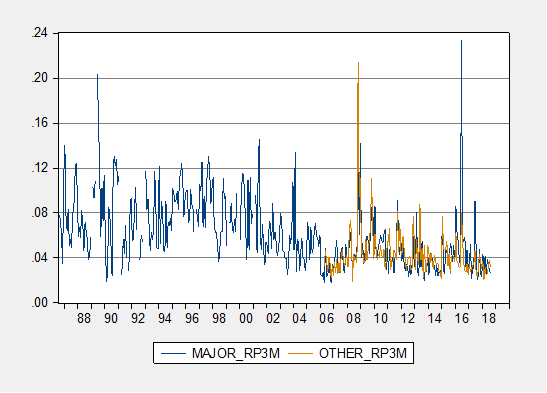

For the second item, regarding exchange rate risk, we abandon the assumption of rational expectations and use survey data to assess the size of the short-term (3-month) exchange rate risk premium, and find that it has generally declined in the past three decades for major currency pairs. On the other hand, for emerging market and developing country currencies (against the US dollar), there has been little change on average over the past two decades.

figure 2: Average absolute outstanding spread between advanced economy currencies (blue) and emerging market currencies (tan), annualized. Calculated using survey data. source: Chin and Ito (2023).

These are measures of CIP and UIP deviations. They do not directly inform the question of “what is the slope of the BP=0 schedule” in the IS-LM-BP=0 model. But they do show that the BP=0 line is unlikely to be perfectly flat, even for advanced economies that lack capital controls.

The lecture notes on IS-LM-BP=0 (aka Mundell-Fleming) are as follows:

{kind=link}

{kind=link}