Today, we are pleased to introduce to you the Christian Hoink [1] and Luke Rossi Bank of Italy. The views expressed in this note are solely those of the author and do not necessarily reflect those of the Bank of Italy.

The recent high inflation on both sides of the Atlantic has sparked active discussion among economists and policymakers about the drivers of rising inflation expectations, in particular about the role of supply and demand contributions. This column summarizes new evidence from a recent paper in which we feed financial data into structural models and attempt to inform the above debate. The results show that over 2021-23, inflation expectations in the US are held steady by domestic demand, whereas in the EA, inflation expectations mainly reflect the role of supply shocks and, more recently, a strong increase in demand factors. Our evidence also suggests that monetary policy shocks gradually help moderate inflation expectations in the two jurisdictions, albeit at different times and in magnitude.

In early 2021, the ECB’s medium-term inflation expectations were at historically low levels, and prolonged deflation led the ECB to first cut its key interest rate to negative levels in 2014, followed by a series of other unconventional measures. The post-pandemic recovery, supply chain bottlenecks, and higher energy prices (especially after the Russian invasion of Ukraine) have triggered a sharp and long-term rise not only in inflation data, but also in inflation-linked swaps (ILS), which reflect real inflation. And long-term growth expectations plus an unobservable inflation risk premium that varies over time. Inflation expectations in the US start at higher levels in the EEA in 2021, but generally follow a similar pattern.

This increase has fueled debate about the underlying structural drivers of the dynamics of inflation expectations. In a post-COVID-19 hyperinflationary environment, an assessment of inflation expectations, especially the risk that they may become unanchored, is crucial for central banks. However, disaggregating the relative contributions of supply and demand factors is challenging because supply and demand shocks occur simultaneously. In addition, interconnected financial markets transmit shocks to individual economies; this makes it important to consider spillovers when identifying structural shocks. In particular, it has been documented that the U.S. economy plays a central role in financial markets, and developments in the country affect the rest of the world through financial linkages (Rey, 2016; Farhi and Werning, 2014; Bruno and Shin, 2015).

Identifying the role of supply and demand shocks in inflation expectations

In a recent paper (Hoink and Rossi, 2023) We propose a method for assessing the structural drivers of inflation expectations, as measured by inflation-linked swaps. To this end, we estimate a Bayesian vector autoregressive (BVAR) model for the two economies based on daily asset price changes in the euro area (EA) and the United States (US). Shocks are identified using notation and magnitude constraints (Arias et al., 2018), while also accounting for international spillover effects. In particular, the identification builds on theoretical insights that suggest that asset prices (including the ILS rate) respond in specific patterns to each of the different shocks that may hit the economy. The use of daily data also provides a real-time narrative that avoids the lag in release and low availability that plague macroeconomic data.

By making reasonable assumptions about how stock prices, bond yields, and ILS co-variate with these shocks, incorporating inflation expectations, it is possible to clearly distinguish supply and demand innovations. Favorable EA demand and supply shocks have a positive impact on stock prices. However, they have opposite effects on long-term yields and inflation expectations. A positive demand shock raises inflation expectations and long-term yields. Conversely, a favorable supply shock lowers inflation expectations.

Drivers of market-based inflation expectations in the euro area and the United States

We use our model to examine the drivers of the recent surge in inflation expectations in the United States and the euro area, focusing on two issues. First, what are the fundamental reasons for the rise in inflation expectations? Second, has monetary policy effectively contained the surge in inflation since the monetary policy tightening process started?

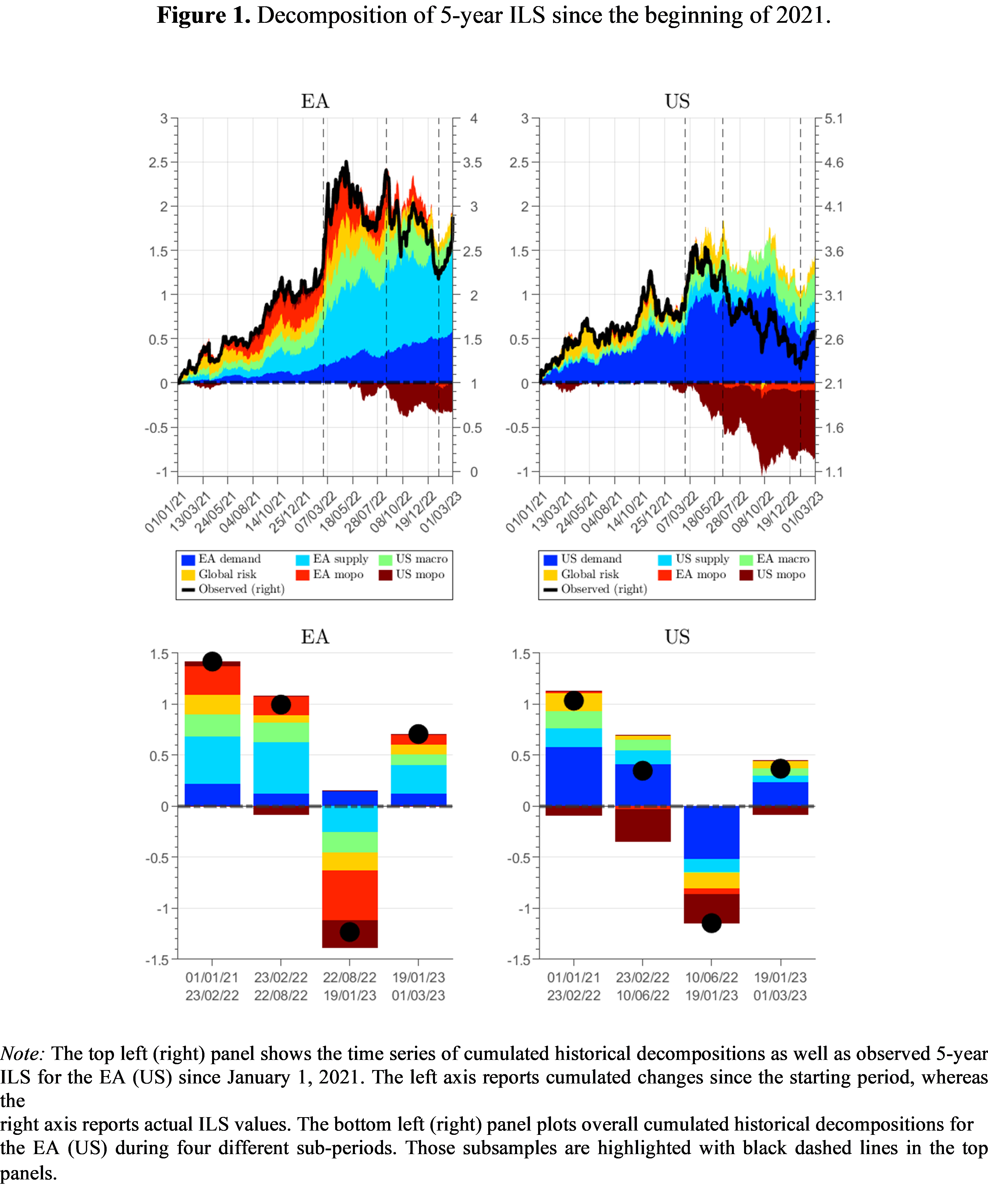

According to our estimates, the structural drivers of medium-term inflation expectations in the US and the euro area contrast sharply, as reflected in the cumulative historical decomposition (Chart 1). In the Euro Area (EA), the dynamics of the 5-year ILS since early 2021 can be divided into four sub-periods.

- From Jan 1, 2021 to Feb 23, 2022, the day before the Ukraine invasion, Eurozone 5-year inflation expectations rose by 140bps, mainly due to supply-side factors (50bps), which is likely Related to bottlenecks, and relative to historical norms, monetary policy remains relatively accommodative (30 bps).

- From the beginning of the war in Ukraine (24 February 2022) until 28 August 2022, supply shocks are again the strongest driver of EA’s medium-term inflation expectations. The contribution of EA demand shocks is relatively small but consistently positive, so the build-up during 2022 likely reflects a gradual improvement in business cycle conditions.

- The third period (22 August 2022 to 1 January 2023) is characterized by a marked decline in inflation expectations from the peak reached in August 2022. The model attributes this to the reduced contribution of supply shocks (likely related to favorable energy price dynamics), as well as the combined effect of negative EA effects and US monetary policy shocks. In total, inflation expectations have fallen by 120 bps since August 2022, of which 75 bps can be attributed to monetary policy tightening in EA (50 bps) and US (25 bps), and 25 bps to supply-side stress relief.

- The final phase begins on January 19, 2023 and shows a rise in inflation expectations, most likely due to higher-than-expected core inflation data, which could lead financial market participants to reassess their views on the degree of stickiness of inflation and uncertainty about tightening end of cycle.

Although the dynamics of medium-term inflation expectations in the United States are qualitatively similar, the underlying drivers are markedly different. The right panel of Figure 1 shows the dynamics of US medium-term inflation expectations.

- From the beginning of 2021 to the outbreak of the war in Ukraine, US inflation expectations rose, mainly due to domestic demand (60 bps) likely related to the unprecedented fiscal stimulus package provided by the US government and the subsequent strong rebound in consumption. Supply-side factors related to bottlenecks in production chains or changes in energy prices account for only a small proportion (20 basis points).

- Overall inflation expectations have risen since the outbreak of the Ukraine war, despite two opposing forces pushing inflation expectations in different directions: on the one hand, demand has continually met inflation expectations; on the other hand, demand has continued to increase inflation expectations. On the other hand, the Fed has taken a more aggressive stance in dealing with rising prices, which has put a firm and strong brake on price increases (-30 bps). Compared with the ECB, the Fed started the tightening process earlier (March 2022) and more aggressively, which is reflected in the earlier and stronger impact of US monetary policy shocks on easing domestic inflation expectations, and the impact on the euro area. Spillover Effect. Again, during this period, US supply-side factors played a smaller role than demand-side factors.

- Inflation expectations have eased since their last peak in June 2022 amid ongoing tightening monetary policy shocks and subdued domestic demand pressures. The spillover effects of EA monetary policy shocks do not contribute significantly to the development of US inflation expectations in 2022, which appears to be in stark contrast to the effect of US monetary policy shocks on EA inflation that we observe. Similar to EA, the rise in global risk appetite also exacerbated the decline in inflation expectations during this period.

- Since January 19, 2023, U.S. medium-term inflation expectations have soared, with stronger-than-expected consumer and producer prices, consumption and labor market data, but to a lesser extent also affecting international inflation. (EA Macro and Global Risks) Demand Factor.

in conclusion

In the post-epidemic high inflation environment, monitoring inflation expectations is crucial for the central bank. In our paper, we propose a method to quantify the structural drivers of EA and US inflation expectations, measured in real time through inflation-linked swaps. We decompose its day-to-day fluctuations into domestic, foreign and global shocks through a Bayesian VAR model.

From early 2021 to mid-2022, medium-term inflation expectations in the euro area rose mainly in response to adverse supply shocks, while the contribution of demand shocks in the euro area rose gradually during 2022, reflecting improving business cycle conditions. Our evidence also demonstrates strong spillover effects of US monetary policy on EA inflation expectations since the second half of 2022, and a strong easing effect of EA monetary policy tightening. In the United States, by contrast, inflation expectations have been held steady by the impact of domestic demand shocks until the end of October 2022, and have been subdued by tightening monetary policy shocks since March 2022, when the Fed began its tightening cycle.

bibliography

- Arias, Jonas E., Juan F. Rubio-Ramirez, and Daniel F. Wagoner (2018), “Inference of Structural Vector Autoregressions Based on Symbolic and Zero-Restricted Recognition: Theory and Applications” Econometrics,roll. 86(2), pp. 685-720.

- Brandt, Lennart, Arthur Saint Guilhem, Maximilian Schröder, and Ine Van Robays (2021), “What Drives Euro Area Financial Markets? The Role of U.S. Spillovers and Global Risks”, ECB Working Papers SeriesNo. 2560, May.

- Bruno, Valentina, and Hyun Song Shin (2015), “Capital Flows and the Risk-Taking Channel of Monetary Policy”, vol. Journal of Monetary Economics71, 119–132.

- Cecchetti, Sala, Adriana Grasso and Marcelo Perricoli (2022). “Objective Inflation Expectations and Inflation Risk Premium Analysis”, topic of discussion (Italian Economic Working Paper Series)1380, Bank of Italy, Economic Studies and International Relations.

- Cieslak, Anna, and Andreas Schrimpf (2019), “Non-monetary news in central bank communication”, vol. Journal of International Economics118, 293–315.

- Cieslak, Anna, and hao Pang (2020), “Common Shocks for Stocks and Bonds”, vol. SSRN Electronic Journal2020.

- Degasperi, Riccardo (2021), “Using OPEC Announcements to Identify Expected Shocks in Oil Markets”, vol. oil draft.

- Farhi, Emmanuel, and Ivan Werning (2014), “Dilemma rather than trilemma? Capital controls and the exchange rate of capital flow volatility”, vol. IMF Economic Review2014, 62(4), 569–605.

- Jarocinski, Marek, and Peter Karadi (2020), “Deconstructing Monetary Policy Surprises—The Role of Information Shocks”, vol. American Economic Journal: Macroeconomics12(2), 1-43.

- Rey, Helene (2016), “International Transmission Channels of Monetary Policy and Mundell’s Trilemma”, vol. IMF Economic Review64(1), 6-35.

- Venditti, Fabrizio, and Giovanni Furio Veronese (2020), “Real-time shocks to global financial markets and oil prices”, vol. SSRN Electronic Journal2020.

- Visco, Ignazio (2023), “Inflation Expectations and Monetary Policy in the Euro Area”, vol. 95the th Distinguished Lecture by Robert Mundell at the International Atlantic Economic ConferenceMarch 23, 2023.

notes

[1] Directorate General of Economics, Statistics and Research of the Bank of Italy. We thank Martina Cecioni, Stefano Neri, Pietro Rizza, Massimo Sbracia, Alessandro Secchi, and Fabrizio Venditti for their helpful comments and suggestions. Fabrizio Venditti shared the MATLAB code.

The author of this article is Christian Hoink and Luke Rossi.

{kind=link}

{kind=link}