Divisia M4 Are error-correction models from quantity theory or old-style expectations and supply shock-enhanced Phillips curves better suited for the post-2019 period (using 1998-2019 data)? A: The Phillips curve works better.

In fairness to quantity theory, I tested for cointegration between the PCE deflator and M4 divided by GDP (thus imposing a unit coefficient on GDP). Johansen maximum likelihood usually detects cointegration. Then I estimate an error correction model:

D.pt = 0.114 – 0.016(point-m+y)t-1 + 0.224Dpt-1 – 0.001Dricet-1 + 0.222D.the yt-1

adjust-R2 = 0.13, SER = 0.0036, DW = 1.90, NOb = 88

and the Phillips curve:

D.pt = 0.002 + 0.020(yypot)t-1 + 0.077PIet-1 + 0.0008GSCPIt-1 + 0.0009GSCPIt2 + 0.019D.pOilt + 0.006D.pOilt-1

adjust-R2 = 0.69, SER = 0.0021, DW = 1.98, NOb = 88

Where p is the log PCE deflator, Δp is q/q inflation, rice is the logarithm of the M4M divisia, the y is the logarithm of real GDP, the ypot is potential GDP (CBO), PIe is Michigan expected inflation, ΔpOil is the quarterly growth rate of oil prices, and GSCPI is the New York Fed Global Supply Chain Stress Index.

Note that there is some truth to the estimates of the quantity theory/divisia model. The statistical significance and negative coefficient of the error correction term suggest that in the long run, the price level will rebalance by about 1.6% per quarter. (Interestingly, both GDP and money recovered faster than prices.)

Phillips curve fitting is much better with adj-R2 0.69. The output gap has a significant and positive coefficient. Expected inflation also came along with oil prices.

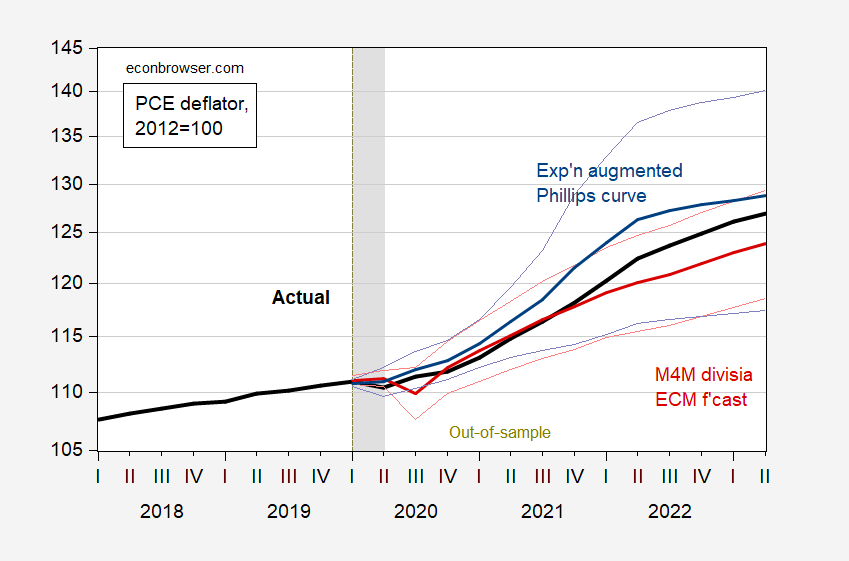

How do these two empirical models compare?out-of-sample forecasts (strictly speaking, two afterwards historical simulation, since the right-hand variable is taken as given).

figure 1: PCE deflator (black bold), quantity theory/division model (red), plus/minus one standard error band (pink line), expectations and cost-push shock-enhanced Phillips curve model (blue), plus/minus One standard error band (light blue line), all 2012 = 100. Recession peak-to-trough dates as defined by NBER are grayed out. Source: Author’s calculations.

In other words, the Phillips curve actually predicts price levels very well, contrary to claims that inflation is not well predicted. In fact, if it had been known that oil prices would rise in early 2022 and that supply chain pressures would increase in 2021, it would not be surprising if inflation persisted.

{kind=link}

{kind=link}