I was asked by a reporter today if this time is different, especially given all the positive consistent metrics (Q3) The current gross domestic product (GDP) is 5.6% few weeks; Fed staff upgrades Q4/Q4 growth rate, Goldman puts recession probability at 15%). I’m (I hope correct) wary.

First, as I pointed out a month ago, using the standard probability model’s 50% threshold suggests a recession in Q4 2023 – we’re not in one yet, let alone have data on it.

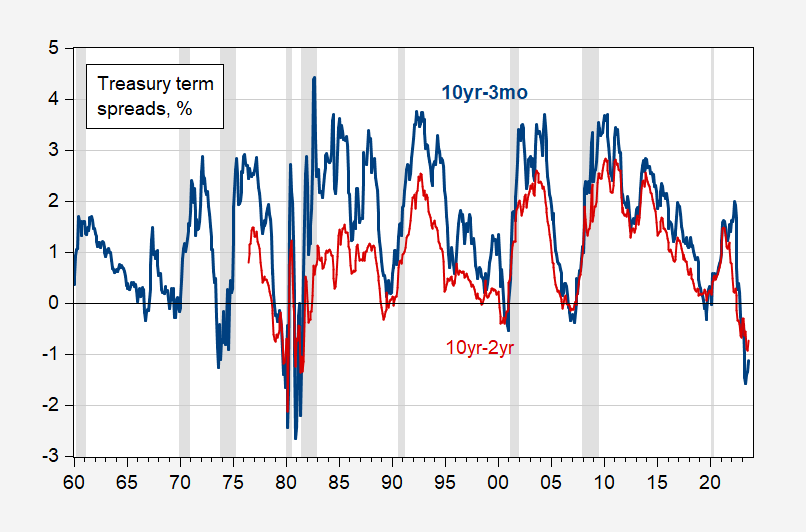

Second, the two term spreads I focus on – 3m10s and 2s10s (10yr-3mo, 10yr-2yr spreads respectively) have a pretty good track record. Since 1960, only 1 false positive in 3 minutes and 10 seconds and no false negatives. Since June 1976, there has only been one missed recession between 2 and 10 years (2020).

figure 1: 10-year to 3-month treasury bond spread (bold blue), 10-year to 2-year (red), both expressed as a percentage. Recession peak-to-trough dates as defined by NBER are grayed out. Sources: Treasury Department, calculations from FRED, NBER, and authors.

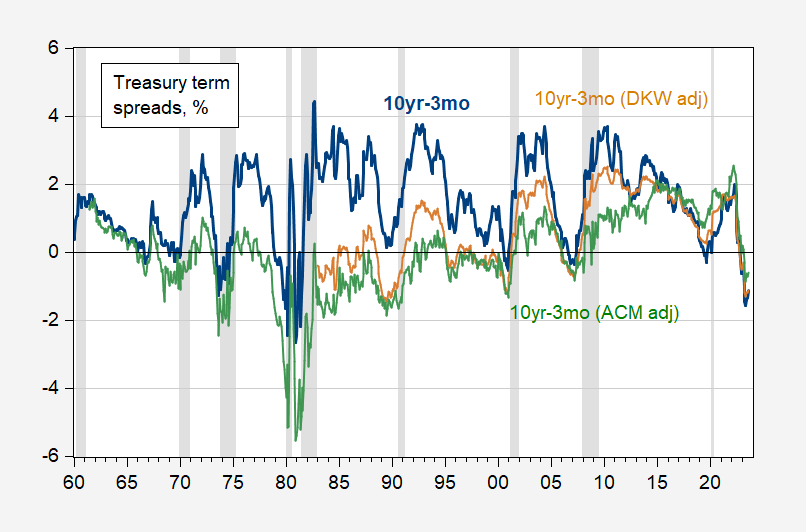

The main argument I hear for why 2023 might be different is that the term premium has been distorted by quantitative easing and tightening. One way to get around this is to adjust the 10-year rate by subtracting the (estimated) term premium.

figure 2: 10Y to 3M Treasury Spreads (Blue Bold), 10Y to 3M Adjusted by D’Amico-Kim-Wei/Board Real/Inflation Risk Premium (Tan) Adrian-Crump-Moench New York Fed periodic premium (green) adjustments, all in %.nitrogenRecession peak-to-trough dates as defined by BER are grayed out. Source: Treasury via FRED, Federal Reserve Board adopts FRED, the fedNBER, and author’s calculations.

Note that the implied term premiums are different, so it is unclear whether premium adjustments would tell a significantly different story about reversal predictive power. The DKW-adjusted spread has forecast 3 of the past 4 recessions (it missed the 2020 recession), but there are also some false positives. ACM adjusted spreads spent too much time in negative territory for some time before 2000 to be of much use.

Of course, these spreads both show statistical significance in the probability regressions, but the pseudo R2 is significantly lower than the unadjusted spread (about 0.18 vs. 0.28).

under any circumstances King and Hamilton (2002) Note that the term premium has predictive power for future economic activity (separately from recession), so it is unclear whether it should be excluded from the regression.

So, I’m not sure why it should be different this time. That being said, the term “link between interest rate differentials and recessions” is a historical correlation, and the past seven years have indeed been remarkable.

{kind=link}

{kind=link}