The SAARs of the Atlanta Fed, New York Fed, and St. Louis Fed are 2.1%, 2.51%, and 1.9%, respectively.

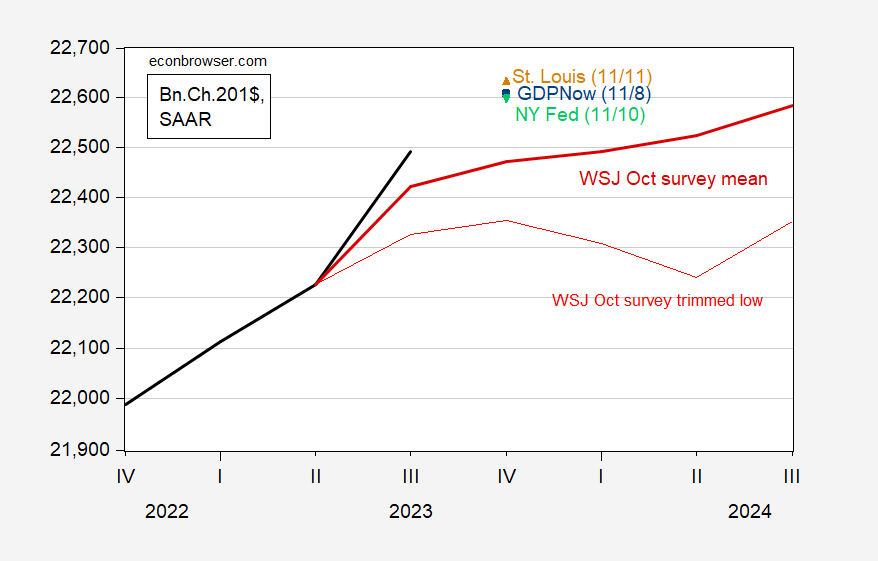

figure 1: GDP report (bold black), GDPNow for 11/8 (blue square), New York Fed live forecast as of 11/10 (green inverted triangle), St. Louis Fed news live forecast (brown triangle), Wall Street Journal survey average (dark red bold), 20% of the Wall Street Journal survey Jonathan Holt/Scotiabank (light red) was slashed by 20%, all in billions of dollars in 2017, SAAR. Level calculated based on pre-released GDP data. Note the logarithmic scale. Source: BEA Q3 2023 Advances, Federal Reserve Bank of Atlanta, Fed, Federal Reserve Bank of St. Louis via FREDThe Wall Street Journal and the author’s calculations.

As of November 4, the latest weekly reading (annual growth) is 2.07% (via Lewis Mertens Stocks New York Fed Weekly Economic Index), -0.02% below trend Baumeister-Leiva Leon-Sims Weekly Economic Conditions Indicator. This means that we are essentially in trend growth according to the BLLS indicator.

These numbers are interesting in the context of term spread recession odds exceeding It will reach 50% around December this year, and the possibility of a widening term spread (FCI, debt service ratio) crossing that threshold in April 2024. So just because we haven’t seen a sharp decline in growth doesn’t mean we’re out of the woods yet.

{kind=link}

{kind=link}