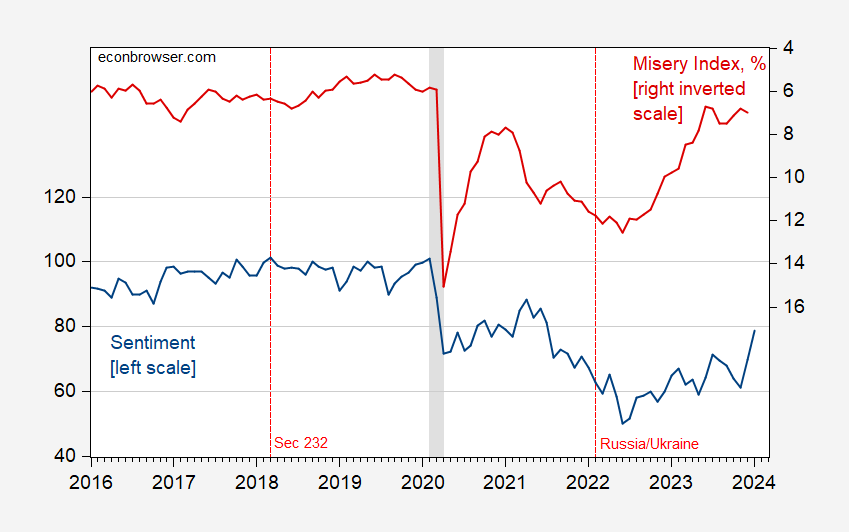

One of the recent mysteries is the discrepancy between conditions (e.g., as measured by the Misery Index) and measured consumer sentiment. Figure 1 shows the Michigan sentiment index (FRED variable UMCSENT) compared with the sum of the inflation rate and unemployment rate for the period 2016 to February 24, 2001. The jump in UMCSENT is 9, which is about 2 standard deviations (2016-23 period), while the December deviation jumps almost two standard deviations and makes up the difference to some extent.

figure 1: University of Michigan Consumer Confidence) (FRED Series UMCSENT) (blue, left scale) and Misery Index, % (red, inverted right scale). NBER-defined recession peak-to-trough dates appear gray. Source: University of Michigan, calculations from FRED, BLS, NBER, and author.

The pain index is inverted, so higher values represent lower pain. Relative to measured economic sentiment, the misery index began to rise around mid-2022. Using a standard OLS regression to analyze distress over this period, starting around mid-2022, the residuals are significantly different from zero. Another way to put it is that as of December 2023, UMCSENT's forecast reading was 88, while the actual reading was about 70.

An interesting fact is that the correlation between UM and UMCSENT inflation expectations is high, rising from zero in 2016-2019 to 0.70 in January 2020-2024. This shows the huge impact of inflation. Another way to look at this is to compare normalized betas before and after the pandemic. The betas of unemployment and inflation were roughly the same before the pandemic. As of January 2020, the inflation beta is approximately 4 times the unemployment beta.

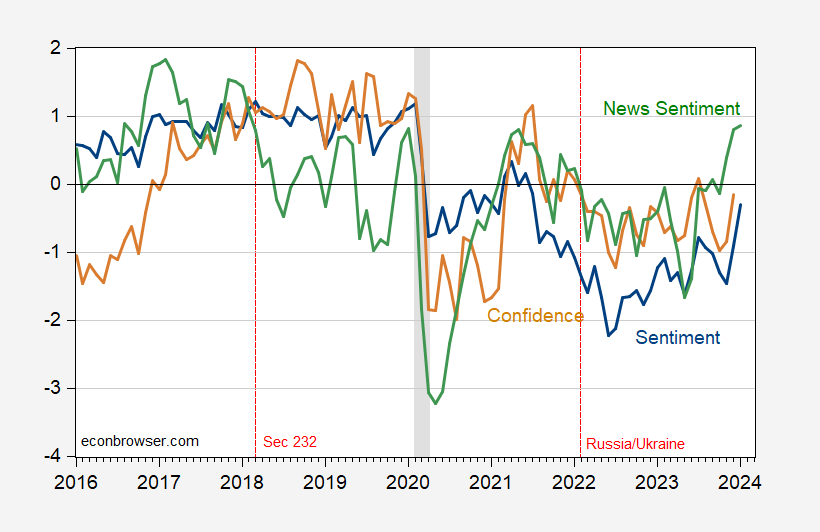

What about other sentiment indicators? The SF Fed News Sentiment Index is a text-based indicator. In Figure 2, I show the (derogated, standard deviation-normalized) UMCSENT, Conference Board confidence index, and news sentiment index.

figure 2: University of Michigan consumer confidence (blue), Conference Board consumer confidence (tan) and Shapiro, Sudhoff, and Wilson (2020) Daily news sentiment index (green), both deflated and normalized by standard deviation (for the sample period shown). The December observations in Michigan are preliminary. December News Index observations are as of January 7, 2024. NBER-defined recession peak-to-trough dates appear gray. Source: U.Mich (from FRED), The Conference Board (from Investing.com), SF FedNBER, and author's calculations.

While the Michigan Sentiment Index tracks news indexes, there are partisan differences. During this sample period, the adjusted R2 The regression coefficient of Democratic sentiment on news index returns is approximately 0.35. A similar regression using Republican sentiment has an adjusted R2 0.04. (Regression of the Confidence Council Consumer Confidence Index on News Sentiment has an adjusted R2 0.19). So basically, Republican sentiment cannot be statistically explained by word-based news sentiment. This is consistent with Republican sentiment being unaffected by economic news, or Republicans interpreting economic news differently than Democrats (or independents, adjusted R).2 is 0.19).

More on the emotional partisan divide, here.

{kind=link}

{kind=link}