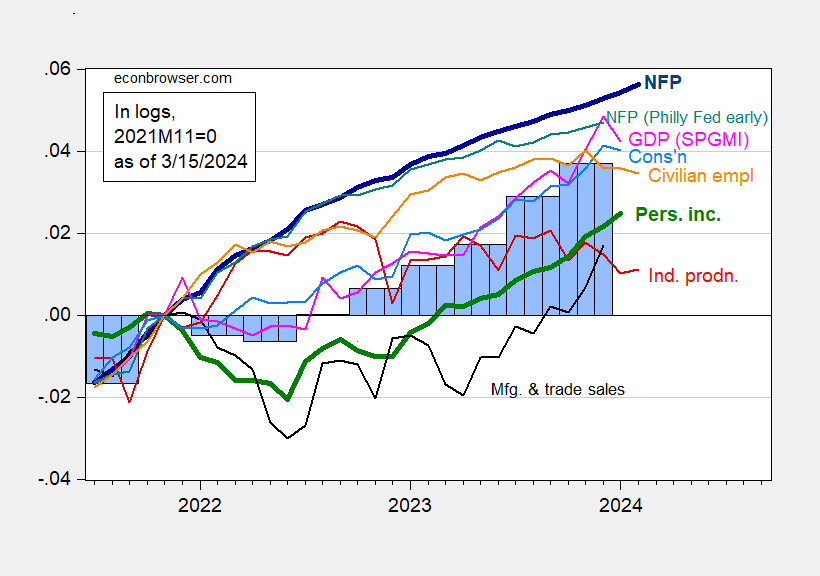

Industrial production was close to consensus, while manufacturing unexpectedly rose (+0.8% quarter-to-quarter and 0.3% quarter-on-quarter). Here's a picture of the key indicators followed by the NBER Business Cycle Dating Committee, along with monthly GDP from the SPGMI (formerly from Macroeconomic Advisers and IHS-Markit).

figure 1: CES nonfarm payrolls (bold blue), Philadelphia Fed early benchmark (cyan), civilian employment (orange), industrial production (red), 2017 personal income excluding current transfers (bold green), Manufacturing and trade sales in 2017 Ch.2017$ (black), 2017 Ch.2017$ consumption (light blue), 2017 Ch.2017$ monthly GDP (pink), the third release of GDP (blue bar), all logarithms normalized to 2021M11=0. Data source: U.S. Bureau of Labor Statistics (BLS) through FRED, Federal Reserve, BEA 2023 Q4 2nd Edition, S&P Global Market Insights (Nigerian macroeconomic consultant, IHS Markit) (3/1/Released in 2024) and the author's calculations.

I included the Philadelphia Fed's early benchmark CES series (not state-by-state aggregate) to examine whether the BLS birth/death model created too many jobs for the official series (see Yesterday's post).

Notably, industrial production has been sluggish over the past year or so. Industrial production includes manufacturing, mining and utilities. I think it would be interesting to see the relationship between real value added reported with a larger lag and industrial production (which is an aggregate indicator).

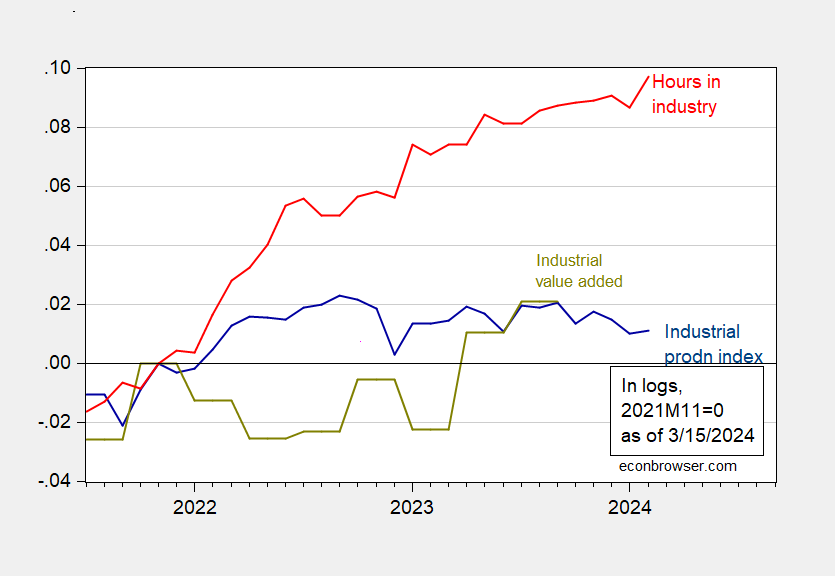

figure 2: 2017 Index of Industrial Production (blue) and Industrial Value Added (Manufacturing, Mining and Utilities combined)$ (yellow-green), Industrial Weekly Production and Total Hours of Non-Supervisory Workers (red), all expressed in terms of The number indicates 2021M11=0. Note: Industrial value added is calculated based on a simple sum of its components rather than using the Tornqvist approximation. Industrial work hours include logging (about 7% of employment in the mining and logging industry). Source: FRB, BLS via FRED, BEA, and author's calculations.

Since the end of 2021, the trends in the industrial value added and production index have varied, but are roughly at the same level as in the first quarter of 2021 in the third quarter of 2021. In contrast, working hours continue to increase.

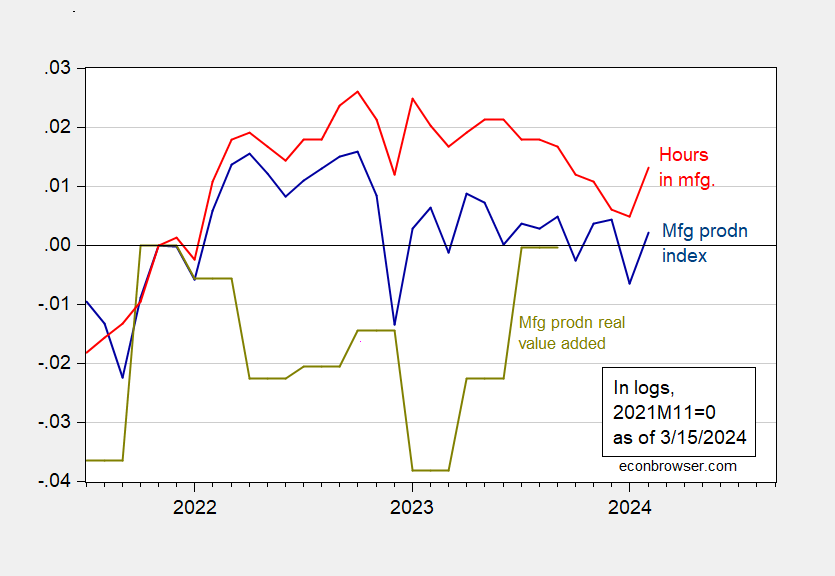

The difference is smaller in manufacturing.

image 3: 2017 Manufacturing Production Index (blue) and Manufacturing Value Added in Dollars (yellow-green), Total Manufacturing Weekly Production Hours, and Unsupervised Workers (red), all in logarithms, November 2021 = 0. Source: FRB, BLS via FRED, BEA, and author's calculations.

Manufacturing value added did fall during 2022, but has since rebounded so that relative to November 2021 levels it is about the same level as manufacturing production. From a business cycle perspective, the rebound in production and hours worked suggests the economic slowdown has eased (one shouldn't draw too many conclusions from one month's worth of data, especially preliminary numbers).

{kind=link}

{kind=link}