It doesn't always work.

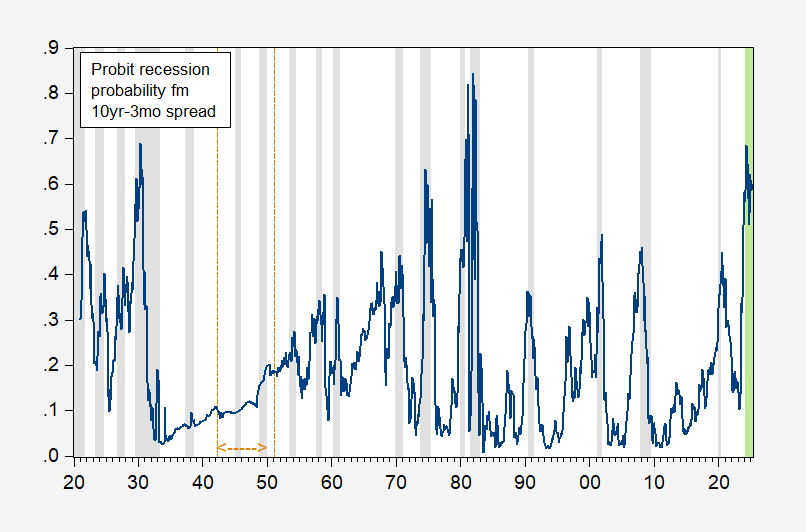

figure 1: The probability that the 10-year 3-month Treasury spread will decline one year earlier (blue). NBER-defined recession peak-to-trough dates appear gray. Light green shaded areas represent out-of-sample periods. The orange dotted line indicates the Fed reached agreement on interest rates. Source: NBER and author's calculations.

Estimated probabilistic regression:

Pr(Record=1) = -0.29 – 0.49 spread

pseudo-R2 = 0.13, Nobs = 1238, Smpl is spreadetc. 1921M02-2024M02. Bold indicates significance at 5% msl.

(Data Note: Shiller's ten-year spread. FRED (TB3MS) three-month rates since April 1934; three-month returns from January 1920 to March 1934 from NBER MacroHistory Database/Friedman- Schwartz.)

Obviously this is not a good fitting specification for this sample period. That’s the point—the success of the term spread predictor is somewhat period-specific. M03

This makes sense given the period from April 1942 to March 1951 when the Fed fixed short-term interest rates and limited long-term interest rates. Then the coefficient on term spread has the wrong sign and is not statistically significant. But in fact, the (constant coefficient) norm didn't work very well in 1934-1941 either.

{kind=link}

{kind=link}