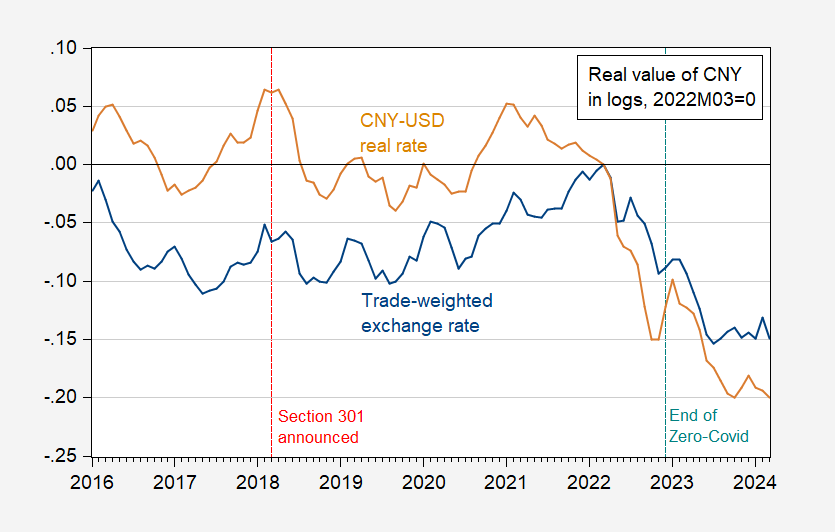

There's been a lot of discussion about China's overcapacity and the resulting pressure on the U.S. and other markets. Here is a picture of China’s real exchange rate.

figure 1: China's trade-weighted CPI deflates the real exchange rate (blue), China-US bilateral CPI deflates the real exchange rate (tan), expressed in logarithms. Up means the RMB appreciates. The authors adjust China's CPI using X-13. Data sources: BIS, FRB, BLS (via FRED).

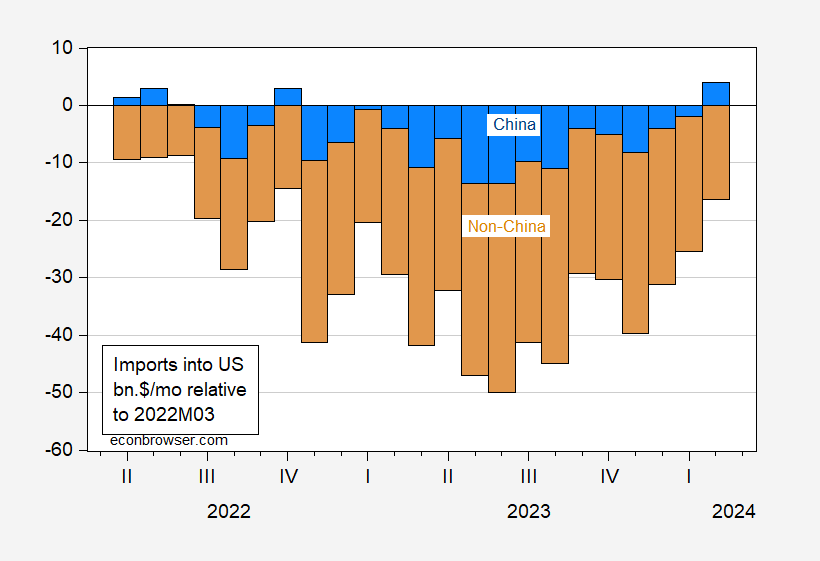

In principle, I would prefer to use PPI to deflate real interest rates and even unit labor cost deflation (see this Paper), but these are harder to come by. The China trade-weighted value of the yuan has fallen 15% in logarithmic terms since its recent peak in March 2022. By comparison, the bilateral real exchange rate fell by 20%. Starting from 2021M02, it will be 25%. Interestingly, imports from China (as shown in trade statistics) are not that different from March 2022:

figure 2: Change in imports from non-China ($bn/month) relative to change in imports from China (brown bar) in March 2022 (blue bar). Imports from China are goods, customs basis; total imports of goods and services, balance of payments basis. The authors use X-13 to seasonally adjust China's merchandise imports. Source: Census Bureau, BEA, via FRED.

Having said that, it is clear that many Chinese goods are entering the United States through third countries (transshipment or production transfer). Indeed, what we would rather see is the added value of imports from China; as far as I know, such latest data are not readily available.

Even so, bilateral value-added flows would not show overall pressure on tradable prices, since Chinese imports would likely depress global trade prices and thus increase U.S. imports.

Is the RMB undervalued?More on this later (for a review of earlier methods, see here).Newest Treasury report from November.this BigMac Index, using December datashowing an underestimation of 26.3% using the Payne effect.

{kind=link}

{kind=link}