Final numbers from the University of Michigan's May survey are out. Here are a few pictures of expected inflation rates over the next year.

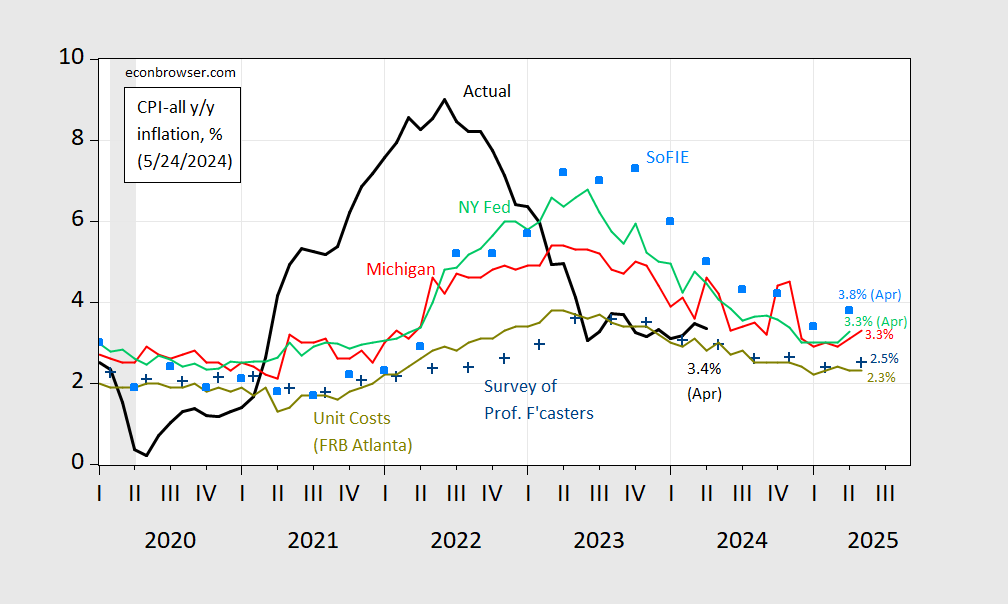

figure 1: Relative to actual CPI inflation (bold black) and expected inflation from the University of Michigan (red), Federal Reserve Bank of New York (light green), Survey of Professional Forecasters (blue+), Coibion-Gorodnichenko SoFIE mean (sky blue (colored squares), and the unit cost growth rate (yellow-green), both expressed in %. Source: BLS, University of Michigan, via FRED, Philadelphia Fed, Federal Reserve Bank of Atlanta, Federal Reserve Bank of Clevelandand the author's calculations.

Note that there is one series that is not related to CPI, the unit cost series from the Atlanta Fed's Business Inflation Expectations Survey. The fact that the series did not exceed expected inflation suggests that there is no strong cost-price spiral.

Interestingly, May's SPF was a full percentage point lower than the Michigan survey median. While SPF values are typically lower than the Michigan (or New York Fed) indicator, SPF values have been closer to actual values in recent quarters.

Interestingly, Survey of Inflation Expectations of Firms (SoFIE) developed by Olivier Coibion and Yuriy Gorodnichenko Still higher than the consumer/household measure (these are previously reported means and medians; see Discussion here).

Bottom line: While inflation is expected to rise in May, it is not as high as previously expected (3.3% final in Michigan, 3.5% preliminary). The median survey of professional forecasters was 2.5%, just shy of the CPI inflation target implied by the 2% PCE deflator.

{kind=link}

{kind=link}