Today we are happy to introduce a guest contribution Carla Wimer (president, U.S. Asian Economic Research Council).

Asian economies have weathered the pandemic in very different ways. In one extreme case, the Philippines’ GDP contracted by 9.5% in 2020, while on the other hand, Bangladesh’s GDP increased by 3.8%.This article is taken from the highlights published in the 3-part series Asian Economic Blog It assesses the various channels through which the pandemic affects the economy and considers fiscal and monetary policy responses in the context of policy space. 1

The virus itself seems to be a channel with a rather weak impact on GDP growth. To be sure, in this case, China, Taiwan, and Vietnam have low infection rates and good GDP growth. However, Thailand’s infection rate is also very low, but GDP contracted by 6.1%, while Bangladesh, which has a moderate incidence, achieved the best GDP performance in the region.

As shown in Figure 1, liquidity loss is a clearer channel to influence GDP growth. Liquidity losses in the Philippines and India exceed 40%, and both variables are at the negative end. In the opposite extreme case, Taiwan and Vietnam caused liquidity losses of less than 10% while GDP growth was positive.

data source: Loss of liquidity based on “retail and entertainment” and “workplace” indicators, Google; GDP growth, IMF World Economic Outlook.

The decline in exports as a channel of influence seems to be mixed, although this situation is close to extreme. Due to its heavy reliance on service exports, the exports of the Philippines and Thailand were hit hardest, with a decrease of about 20% in 2020-the Philippines’ exports are in various forms, while Thailand is concentrated in the tourism industry. China, Taiwan and Vietnam have all achieved positive export growth to support their positive GDP growth.

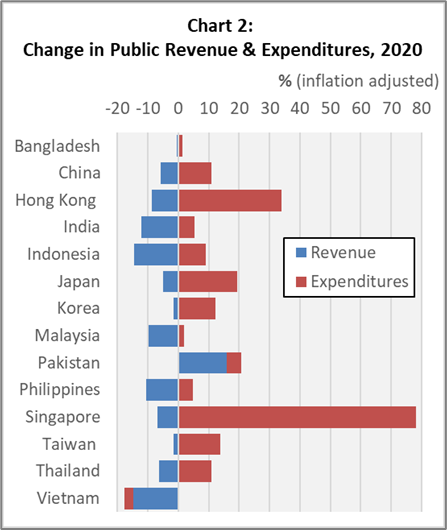

As shown in Figure 2, the few governments that have room to do so vigorously mobilize fiscal policy. However, most governments are constrained by budget constraints. Singapore, which has a long history of budget surpluses, can use accumulated funds to increase spending by nearly 80% without worrying about borrowing costs. The same is true in Hong Kong, where government debt is negligible, which greatly increases spending. Elsewhere, budgets are tighter, especially considering that revenues in India, Indonesia, the Philippines, and Vietnam have fallen by more than 10%.

data source: International Monetary Fund Financial Monitoring.

Before the pandemic, all regions except Taiwan had basic budget deficits, but most were still within the scope of maintaining a stable debt-to-GDP ratio. In 2020, the deficit soared above this sustainability threshold, and Taiwan once again became the only exception. In most cases, the budget seems to be back on the track of sustainable development within a few years, with China being an exception. China’s basic deficit reached 10.4% of GDP in 2020, and it seems that it will far exceed the 2.8% sustainability threshold for some time to come.

With monetary policy support, Asian central banks have lowered policy interest rates and made asset purchases. Figure 3 shows the broad increase in the central bank’s asset growth rate in 2020. In the Philippines and Indonesia, central banks have taken extraordinary steps to provide loans directly to the government to meet public spending needs. In Bangladesh, the central bank vigorously intervened in the foreign exchange market to absorb the surge in net foreign exchange inflows.

data source: International Monetary Fund Monetary and Financial Statistics.

The expansionary policy of the United States has provided liquidity for the global capital market and sufficient room for monetary policy. In this context, Asian economies have a balance of payments surplus, and central banks tend to appreciate currency appreciation or, in a few cases, a slight devaluation. In Bangladesh, India and Singapore, the accumulation of reserves as measured by the balance of payments exceeds 20% of the reserve stock.

If inflation in the United States rebounds and the Federal Reserve subsequently tightens monetary policy, Asian central banks will face pressure to follow suit to prevent capital outflows. Therefore, the race to advance together in vaccinating the population is underway so that all of us can get out of the crisis while the macro policy is normalized.

This article is written by Carla Wimer.

1. Asia Economic Blog, “Pandemic Economy, 2020”

Part 1: Covid Cases, Mobility and Export

Part Two: Fiscal Policy

Part Three: Monetary Policy

↩

{kind=link}

{kind=link}