This is a title Current article today.

If rents continue to rise, this could be bad news for those seeking housing and the country’s inflation outlook. Rental costs play a huge role in the consumer price index, so their significant rise may help keep the closely watched government price index higher, which has already risen sharply.

The CPI of shelters has risen more slowly than the CPI of reduced shelters, so the argument of this article must be-as the temporary upward pressure on goods and services outside the shelters dissipates, the increase in CPI shelters has exceeded previous expectations. And it is expected to last longer than previously expected-this is reasonable given the strong wages and high demand.

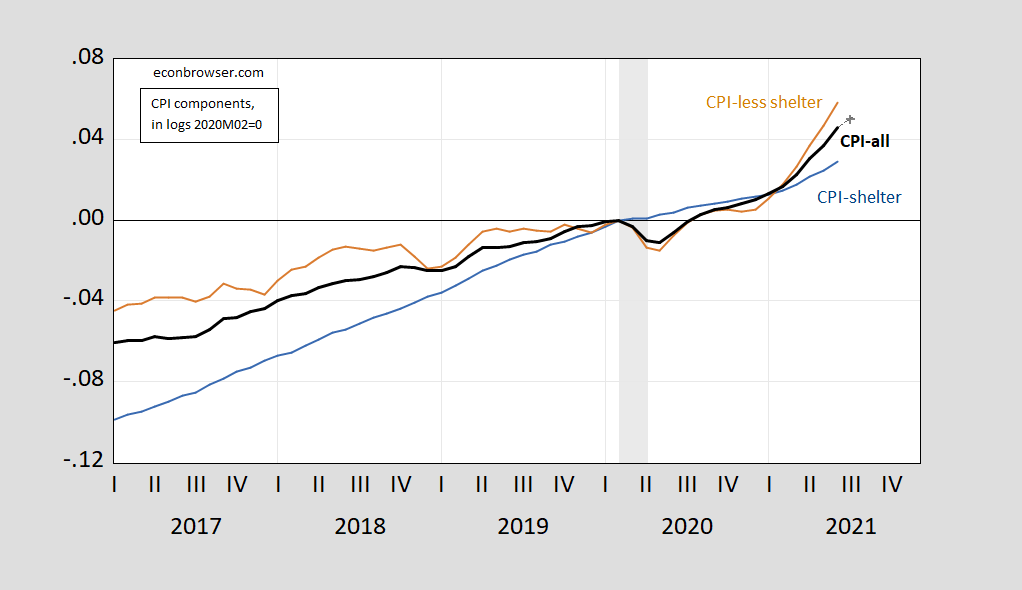

First, what each index has done since 2020M02.

figure 1: CPI-refuge (blue), CPI-less refuge (brown), CPI-all cities (black bold), CPI-all July nowcasts (gray +), all in the log, 2020M02=0. The decline date defined by NBER is shaded in gray. Source: BLS through FRED, Cleveland Federal Reserve, NBER and author’s calculations.

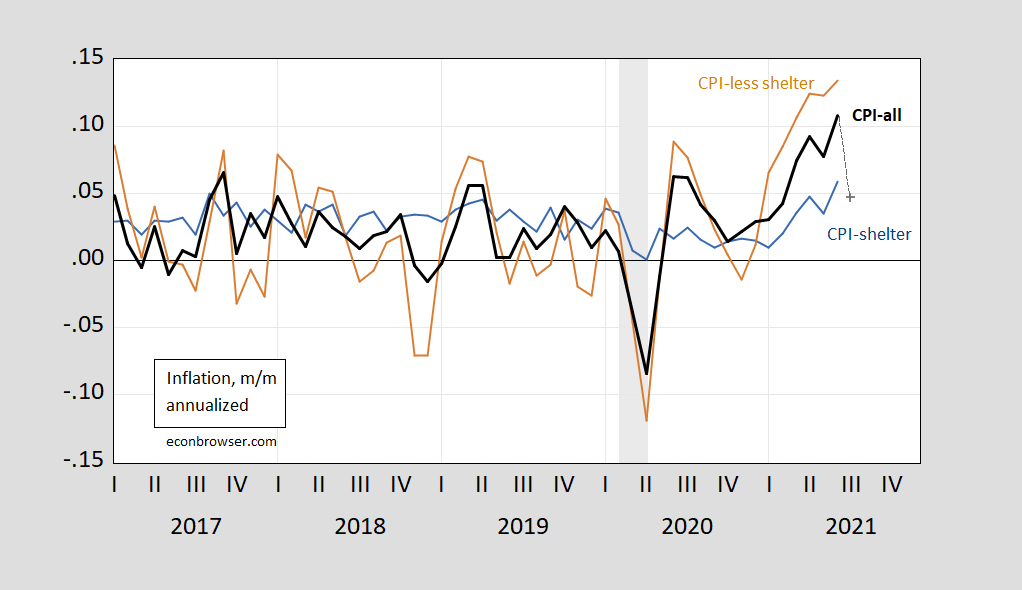

Since the NBER peaked in February 2020, the CPI risk reduction and hedging component has risen by 5.8%, while the CPI risk aversion component has risen by 2.9%. In recent months, the month-on-month ratio of the CPI excluding housing inflation has consistently exceeded the housing portion of the CPI. The Cleveland Fed’s CPI nowcast shows a sharp deceleration in July.

figure 2: CPI-shelter (blue), CPI-less-shelter (brown), CPI-all cities (black bold), CPI-all Cleveland Federal Reserve Nowcast (grey+) month-on-month annualized inflation, all calculated using logarithmic difference . The decline date defined by NBER is shaded in gray. Source: BLS through FRED, Cleveland Federal Reserve, NBER and author’s calculations.

From 1986 to 2019, the persistence of m/m CPI-shelter inflation was lower than that of CPI-less housing (measured by the AR(1) coefficient), so the hypothesis of a temporary jump in housing costs is reasonable. However, the special conditions surrounding the pandemic mean that people will not want to rely on this historical model to maintain.

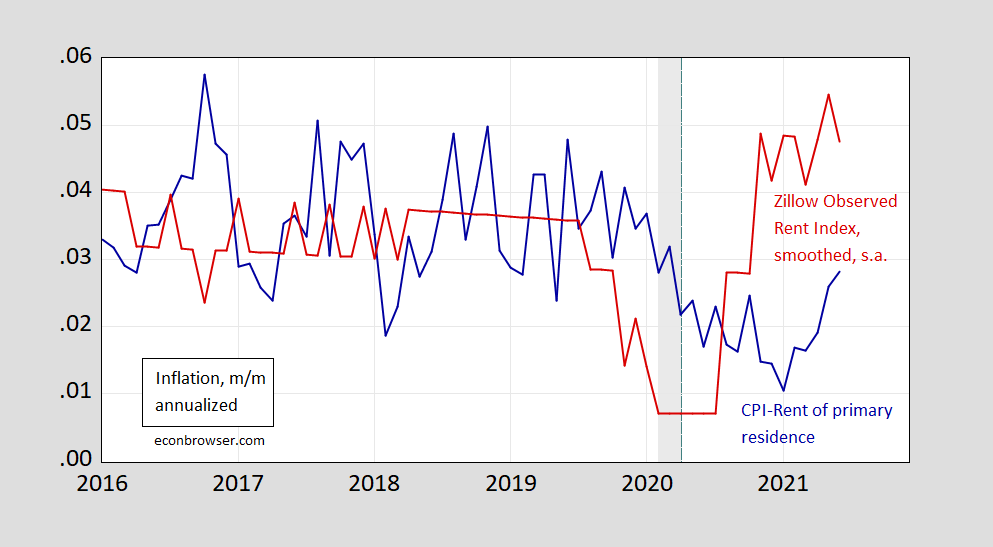

The New York Times article cited Zillow’s statistics (especially the smoothed, unseasonally adjusted series*). I am not sure how useful the Zillow series is for predicting the CPI rent component. Figure 3 plots the m/m growth rate (seasonally adjusted) of the Zillow series and the CPI rent of the main residential component.

image 3: CPI rents (blue) and Zillow Observed Rent Index (ZORI) monthly annualized inflation, smoothed and seasonally adjusted (red), are calculated as logarithmic differences. The decline date defined by NBER is shaded in gray. The green dashed line at the break in the ZORI method. Source: BLS through FRED, Zillo, And the author’s calculations.

In terms of ring frequency, there is no relationship between the two series; there is a frequency at 12 months. Overall, whether housing will maintain high inflation for longer than originally expected seems to be an open question.

* Please note that for some strange reason, the 12-month change in the smoothed Zillow series without seasonal adjustment does not look like the 12-month change in the seasonally adjusted smooth Zillow series.

{kind=link}

{kind=link}