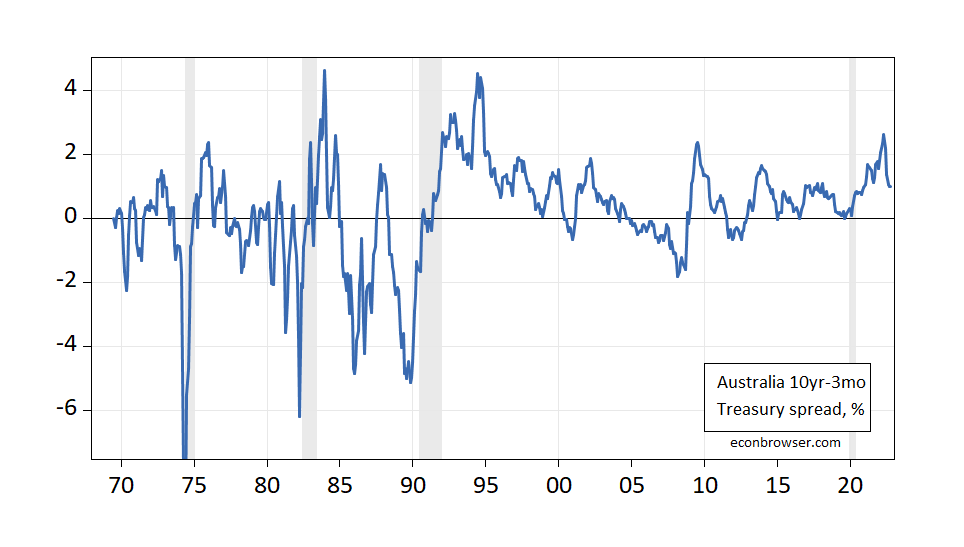

Here is a picture of Australia’s 10-year to 3-month term spread:

figure 1: 10yr-3mo Australian government bond spread, % (blue). ECRI recession dates from peak to trough are shaded in gray. Sources: OECD Key Economic Indicators, ECRI and authors’ calculations.

Probabilistic model for estimating 1968-2021 returns (assuming no recession through December 2022):

Probability (economic recessiont+12) = -1.585 – 0.253 spreadTon + yout+12

McFadden2 = 0.13, NObs = 630.The coefficient is significant at 5% msl bold. Spreads are in percentage points.

While this gap is statistically significant, it would completely miss the 2019-2020 recession. In fact, even using a threshold as low as 20%, the model misses the 2008 recession.This result partially confirms Not Trampis’ point of view; however, rising 3-month Treasury rates also do not appear to be a good predictor of recession.

Notice Karunaratni (2002) does show that, for data prior to 1997, the spread is indeed a good predictor of growth and recession. However, his definition of a recession is based on two consecutive quarters and thus differs from the approach using the NBER or ECRI indicators.

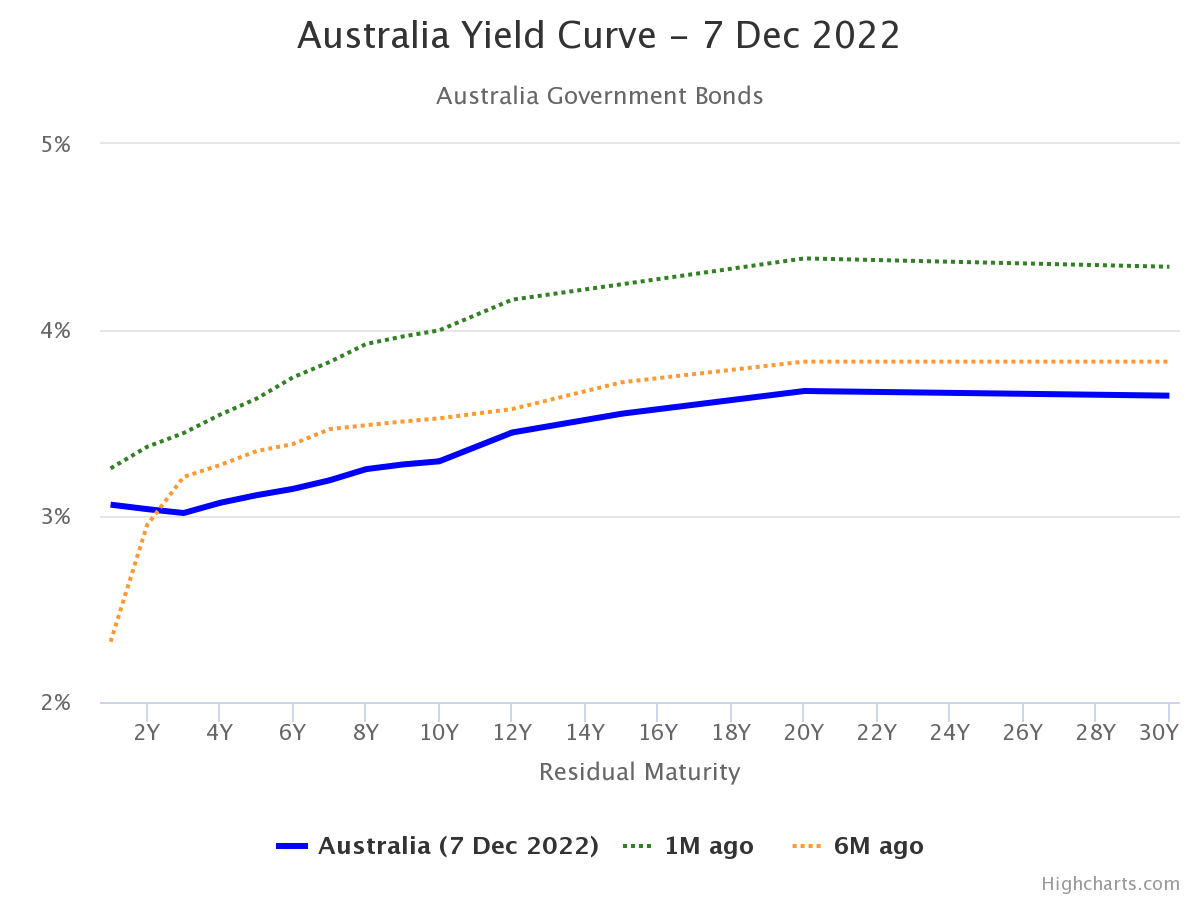

Australian yield curve as of today:

resource: worldgovernmentbonds.com.

The inversion is 3yr-2yr; the curve is indeed much flatter than it was 6 months ago.

{kind=link}

{kind=link}