These relate to the early-release numbers due tomorrow, and recall that they will be revised twice before the end of September as new data arrives.Views have changed slightly since then 5 days ago.

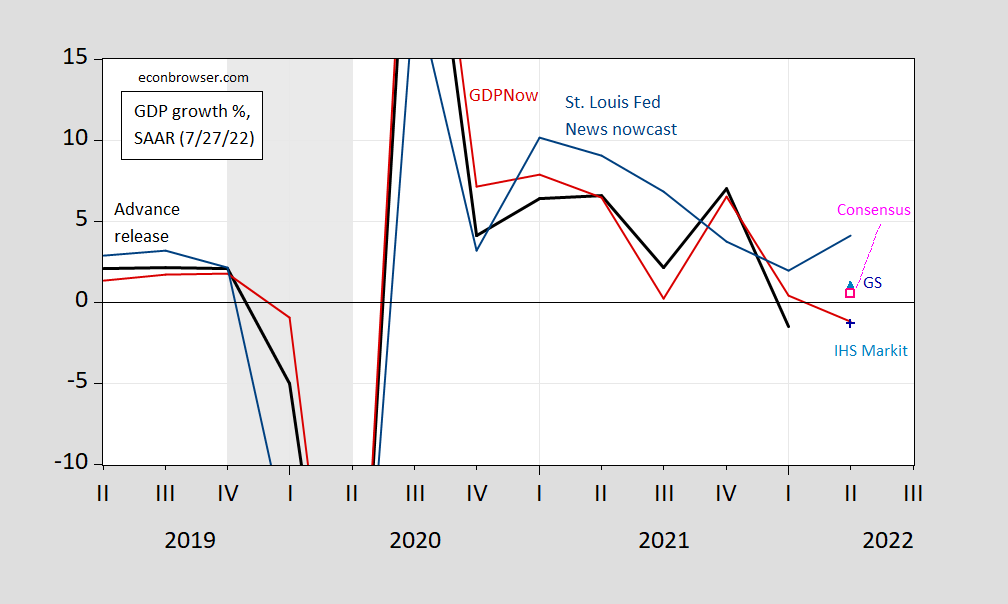

figure 1: Real advance GDP growth (black), Atlanta Fed GDPNow 7/27 (red line), St. Louis Fed News 7/22 (turquoise line), IHS Markit 7/27 (sky blue triangle), Goldman Sachs 7/27 27 (blue+), Bloomberg consensus as of 7/27 (pink open squares), all in %, with NBER-defined peak-trough recession dates shaded in gray. sal. Source: BEA (via ALFRED), Atlanta Fed, St. Louis Fed (via FRED), IHS-Markit, Goldman Sachs, Bloomberg, and NBER.

since last post On 7/22, GDPNow rose from -1.6% on 7/19 to -1.2% on 7/27. IHS Markit rose from -2% to -1.2%. Goldman Sachs has risen from +0.5% to +1%. As of this morning, the Bloomberg consensus is +0.5% (all growth rates are Q/Q SAAR).

Bloomberg rightly pointed out that, according to the Bloomberg consensus, “U.S. economy sees narrow range to avoid back-to-back contractions” (Instead of “recession”, because the NBER can still determine that a recession has begun, depending on what other indicators show).

{kind=link}

{kind=link}