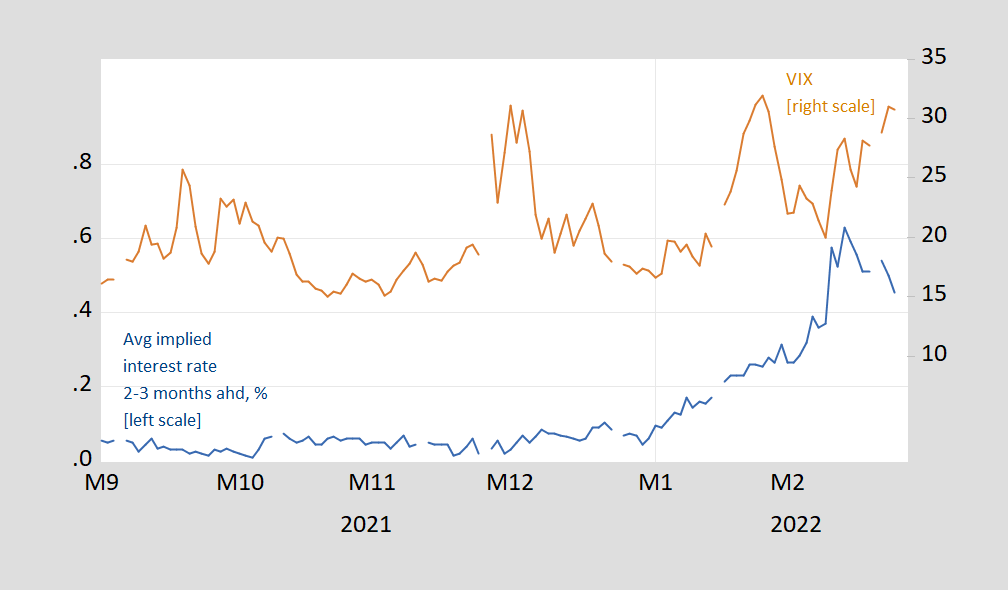

Implied Treasury yields for the next 2-3 months based on 3-month and 1-month yields have declined over the past two days.

figure 1: Implied Treasury yield, percentage (blue, left scale) and VIX (right scale) for the next 2-3 months. Sources: Treasury, CBOE, via FRED, and author’s calculations.

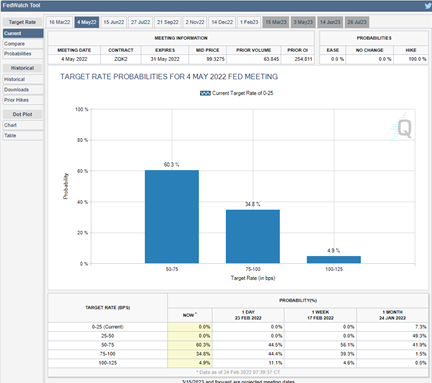

Note that the implied rate for the May FOMC meeting fell from 2/23 to 2/24.

resource: CME FedWatch Toolaccessed 24 February 2022.

While front-month WTI futures settled above $95, the implied probability of a 75-100bps fed funds rate fell from 44.4% to 34.8%, while the 50-75bps probability rose from 44.5% to 60.3%/bbl. So, as far as the market is thinking about the Fed’s direction, for now, the uncertainty of the war is dominating a potential oil-induced cost-push shock.

{kind=link}

{kind=link}