The ruble has stabilized near pre-invasion levels, and Russia’s central bank cut its policy rate to 17 percent. How is this going?

Looking at just these two variables, one might think that Russia has subtly stabilized its economy.However, these two variables are only two components of exchange market stress (discussed at the end of this article). postal), sometimes measured as:

Electromagnetic Pulse = αΔs – βΔresource + γΔA generation

where α, β, and γ are parameters that are usually inverses of the variances of the correlated variables, and resource (foreign exchange reserves normalized by monetary base) and A generation May be related to the core country (usually the US).

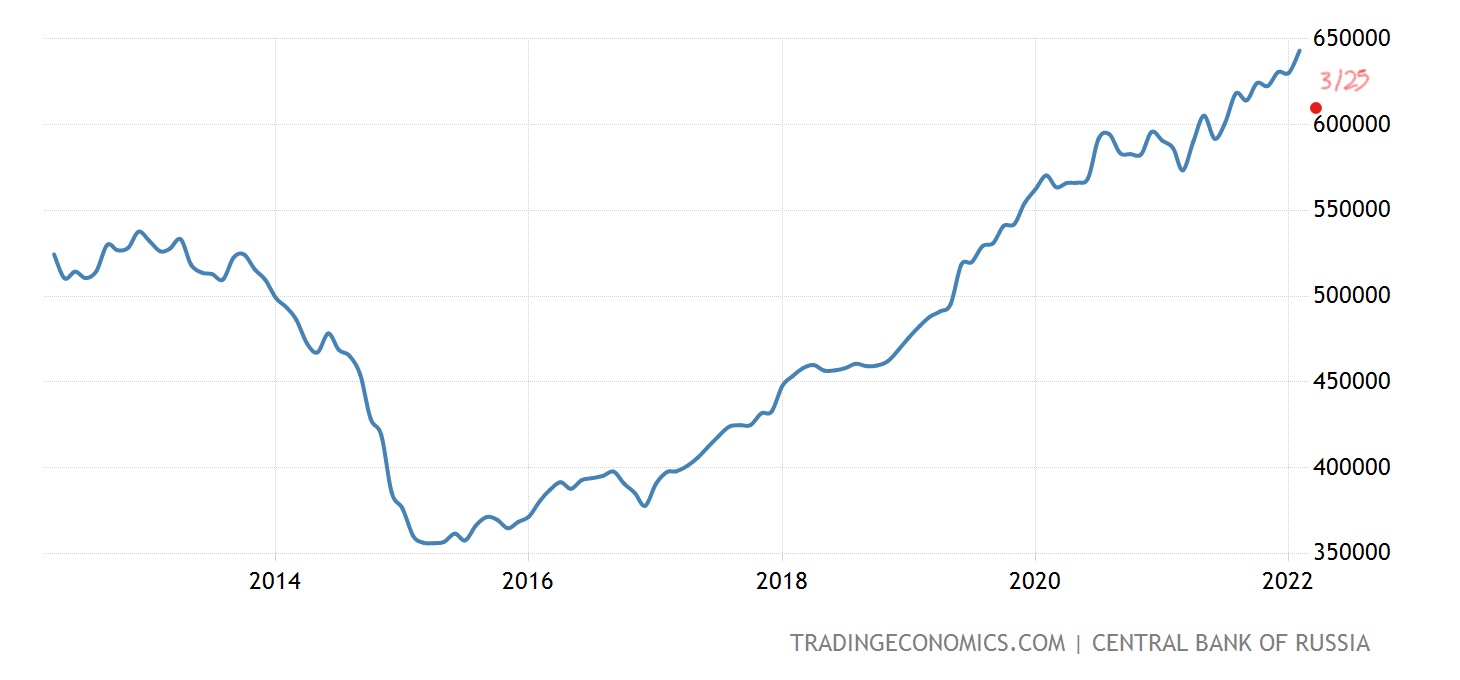

What does the reserve look like? The Central Bank of Russia had been reporting the matter until about March 25th. Here’s what we think is Russia’s chart as of that date (about $604.4 billion, as indicated by the red dots in the chart below, down $38.8 billion from the end of February).

While this may not seem like an overwhelming drop, there are two things to keep in mind. First, the $38.8 billion (reported) loss occurred in 3-1/2 weeks. Second, Russia is unable to tap all of the remaining $604.4 billion in international reserves due to large reserves held offshore by other central banks and private financial institutions.

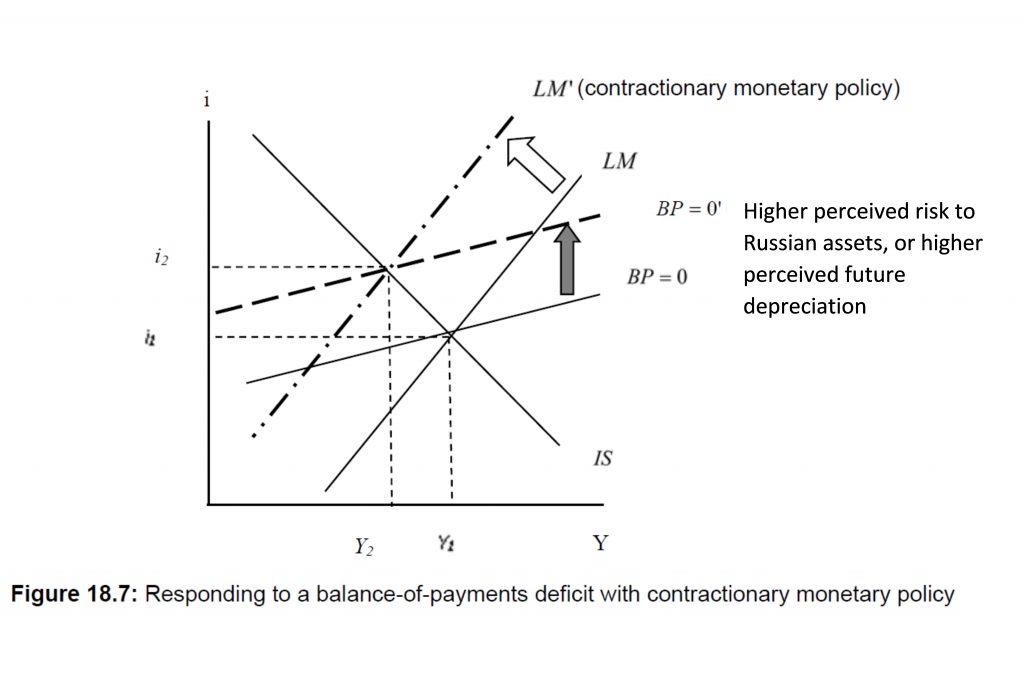

How do we interpret Russian actions in the context of the Mundell-Fleming model? Back on February 22 (before the extent of further Ukrainian aggression became apparent), I explained the imminent sanctions this way:

Rising interest rates, which were only 9.5% at the time, would push the Russian economy into recession. Subsequently, as the ruble depreciated, the policy rate was pushed to 20%. Today, the tax rate has been reduced to 17% (Reuters).

Russia’s central bank slashed its key interest rate to 17 percent on Friday and said further cuts were likely as emergency measures contained risks to financial stability, brought deposits back to banks and helped limit inflationary threats.

I explain the situation as follows:

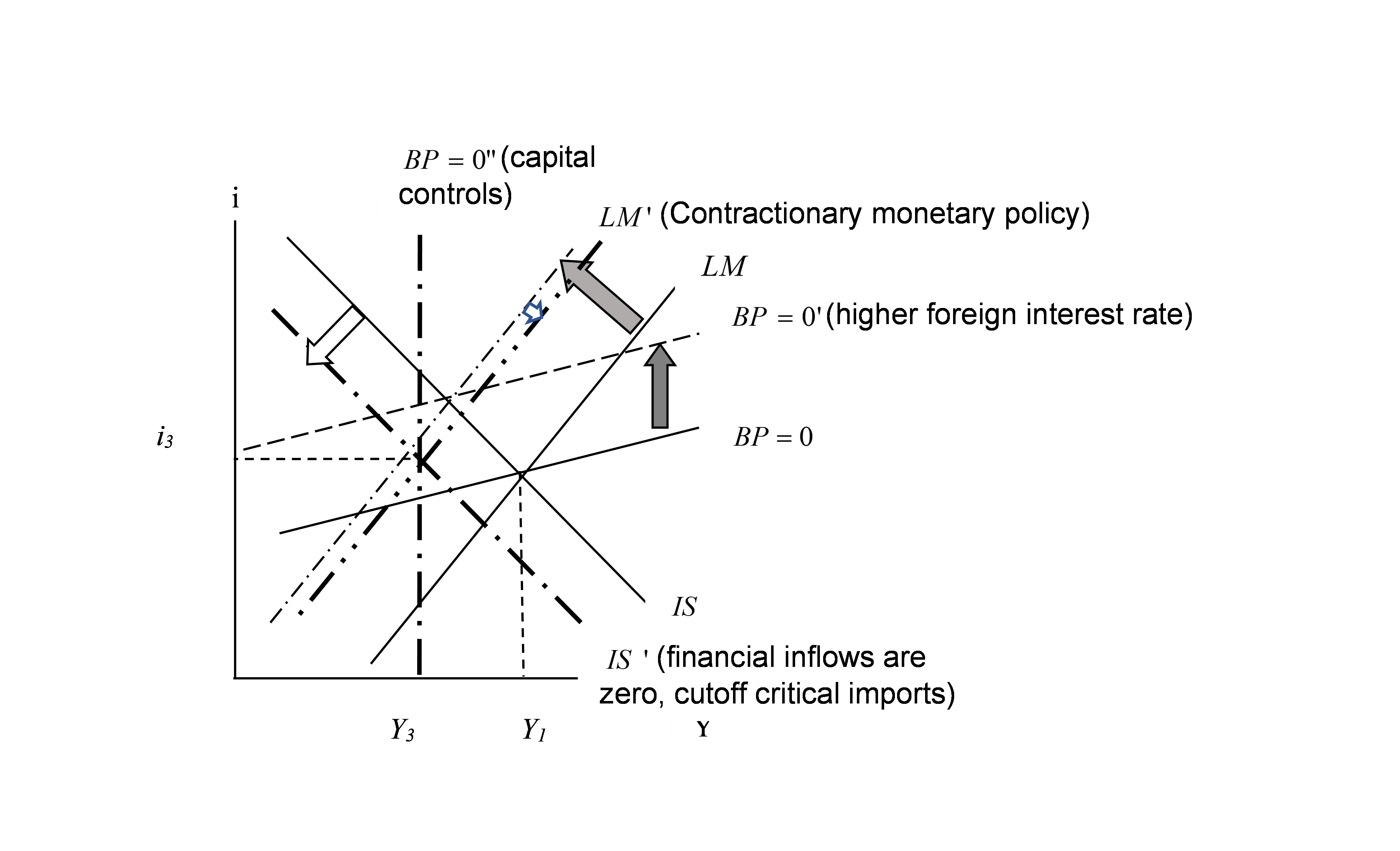

The BP=0 curve has rotated, which gives the central bank some room to cut interest rates. So, for the time being, the highly distorted foreign exchange market appears to be stabilizing, and (as far as we know) reserves. But this comes at the cost of imposing very strict capital controls. It is unclear how much monetary policy can offset the negative effects of lower exports and lower imports of key intermediate inputs needed for domestic production (i.e. I ignore supply shocks that affect prices).

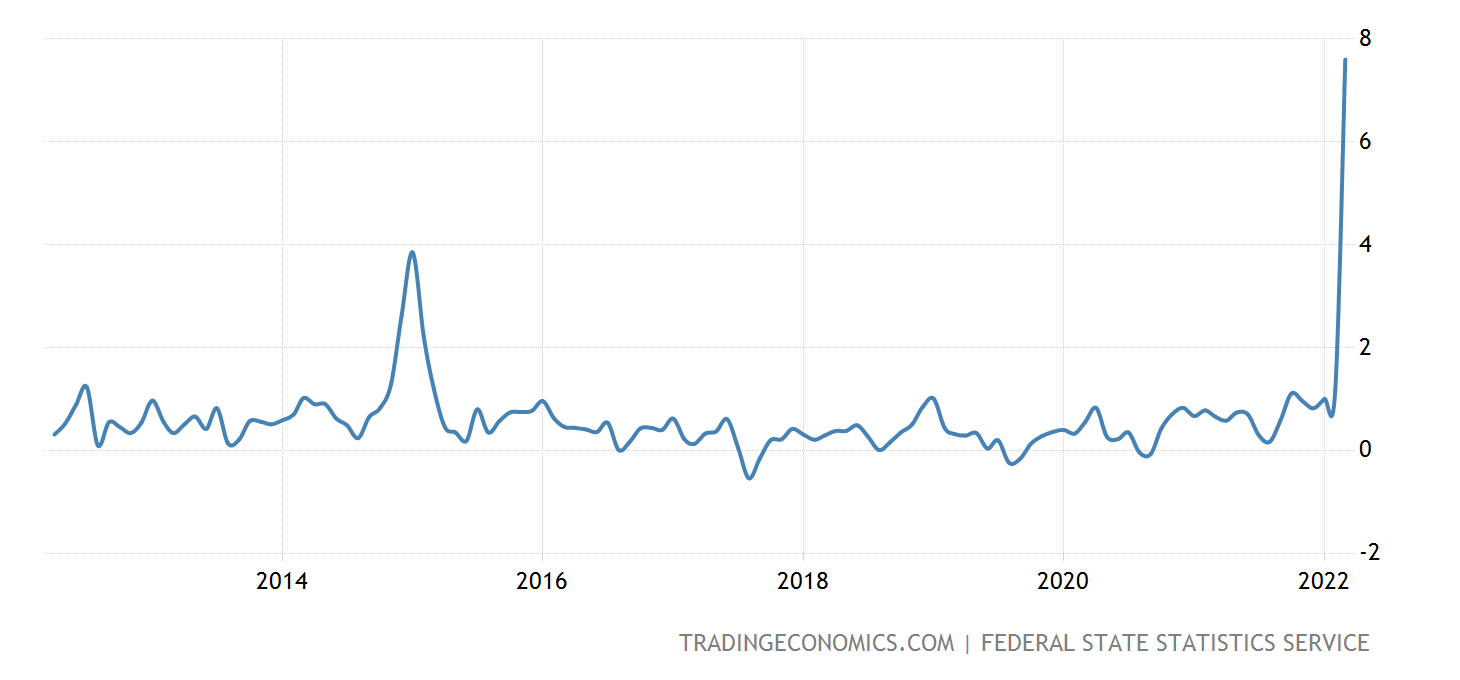

As for inflation, this is the latest data (note: month-on-month CPI, not annualized), at 7.6%:

7.6% m/m with an annualized rate of 140.8%.

{kind=link}

{kind=link}