As the forecast is downgraded (The International Monetary Fund releases new forecasts on Tuesday), here are two pictures of my answer:

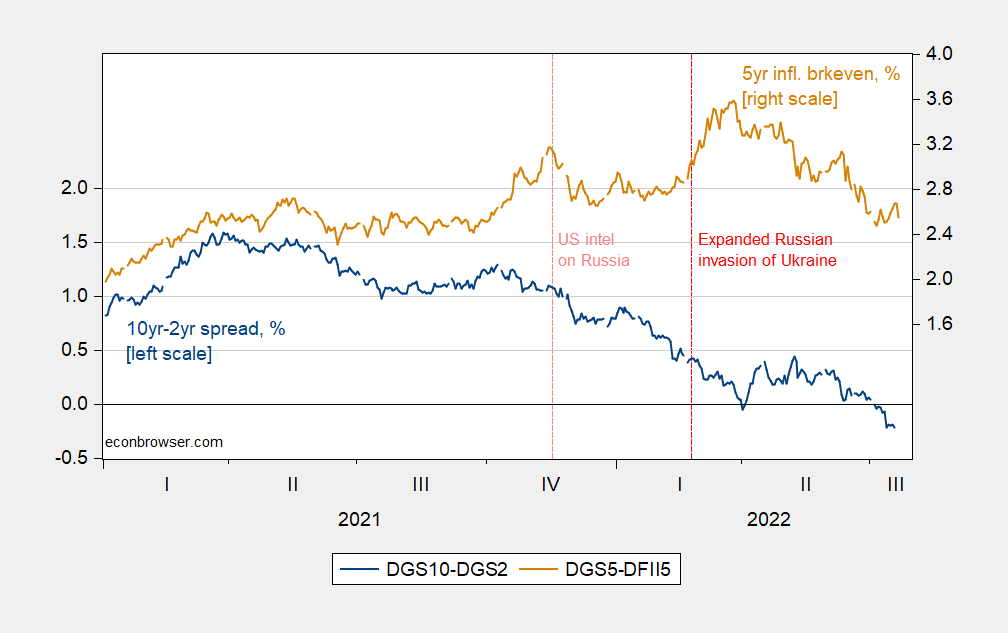

figure 1: 10-year to 2-year Treasury spread (blue, left scale) and 5-year Treasury-TIPS spread (red, right scale), both expressed as a percentage. Source: Treasury via FRED, and author’s calculations.

Inflation expectations over the next five years rose as the likelihood of an expanded Russian invasion of Ukraine in early November increased. The 10- to 2-year spread has also narrowed. With a discrete escalation of the aggression that began on February 24 (as oil prices rose), inflation expectations rose again.

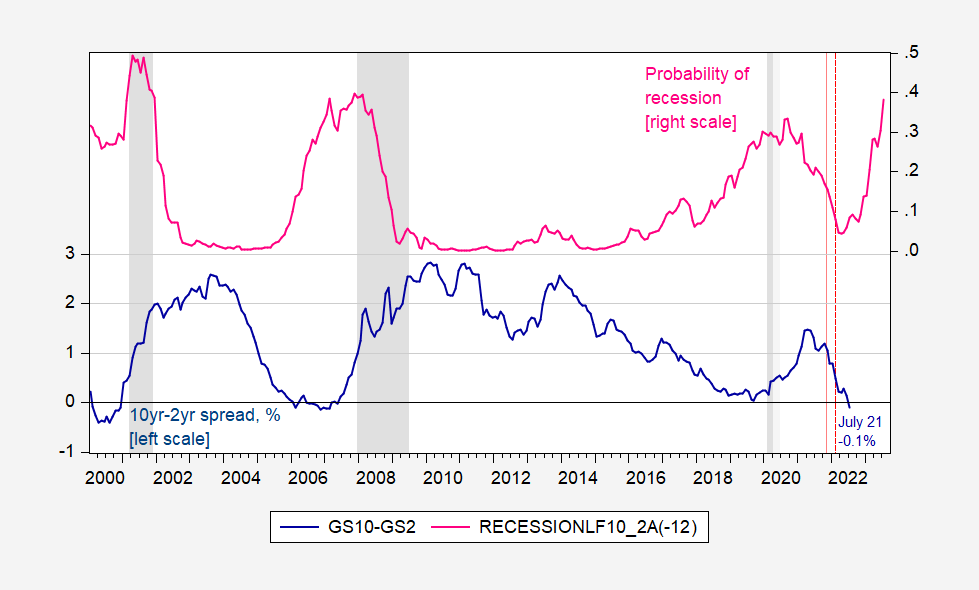

Using term spreads, we can estimate the probability of a recession based on historical correlations. These are shown in Figure 2.

figure 2: 10-year to 2-year Treasury spread, % (blue, left scale) and the probability of a next 12-month recession (pink, right scale) based on a probabilistic spread-based model. July data and probabilities based on 7/21 data. Dashed lines at 2021M11 and 2022M02. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: Treasury via FRED, NBER and author’s calculations.

If one were to use the 30% threshold for recessions (which basically covers all past recessions, but also predicted a recession in 1999/2000), we would be heading for a recession starting in June 2023.

One’s answer will vary depending on whether 10yr-3mo is used instead of 10yr-2yr. Also, if you’re wondering if anyone’s policies have made/encouraged Mr. Putin to participate in this expanded invasion of Ukraine, you’re probably putting the blame elsewhere.

{kind=link}

{kind=link}