Expected economic activity, mid-term market-based inflation expectations and risk/uncertainty measures.

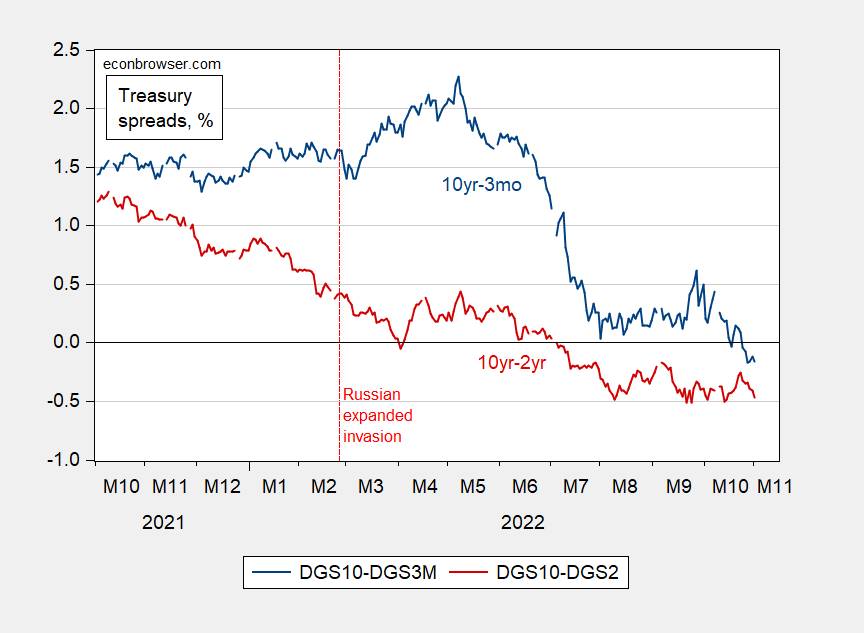

figure 1: The 10-month three-month Treasury bond spread (blue) and the 10-year two-year spread (red), both expressed as a percentage. Source: FRB Calculations from FRED, Treasury and the authors.

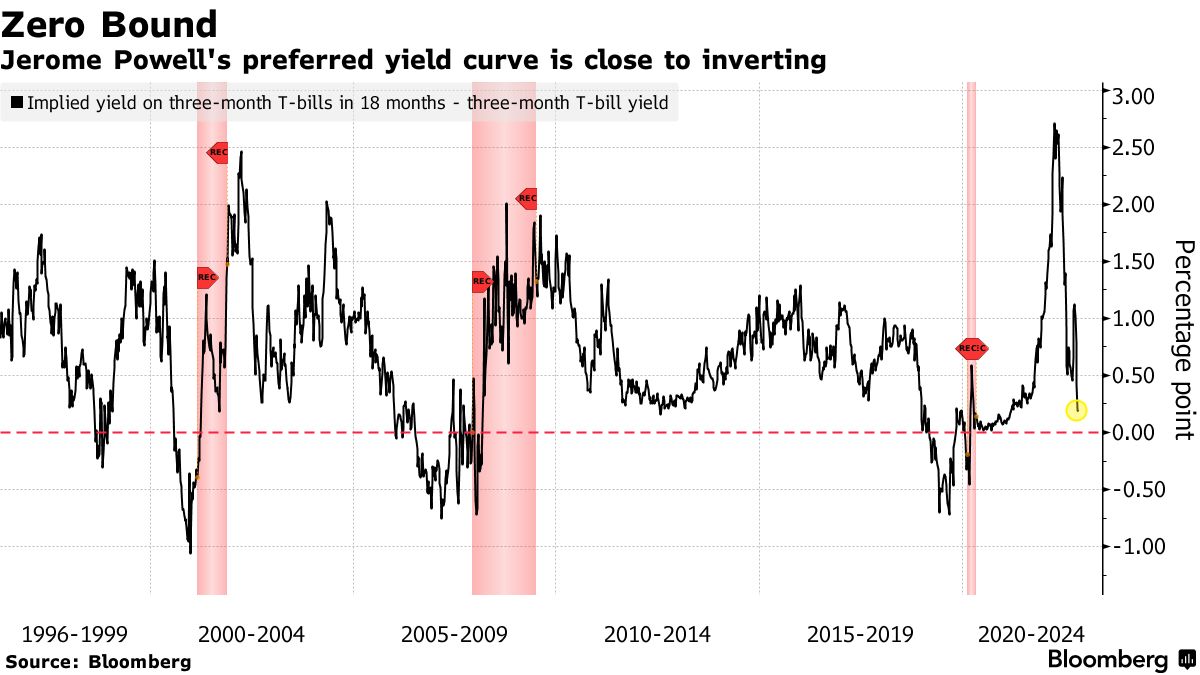

The inversion of the two-term spread is a pretty sure harbinger of a recession next year. Powell’s favored term spread — the 3-month spread relative to the 18-month 3-month forward — is also near inversion.

resource: Reynolds, Gedhill, Bloomberg, November 1, 2022.

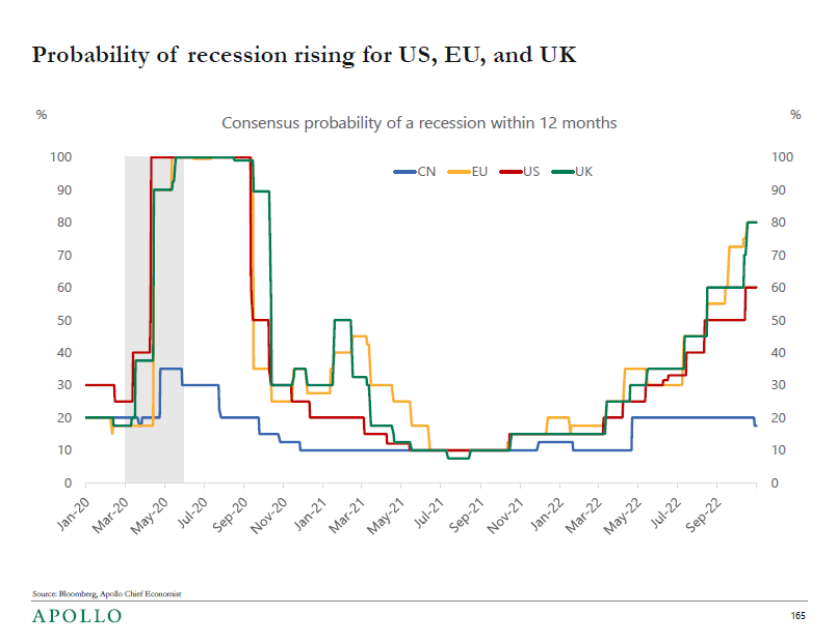

Economists also seem convinced (by countries) of an impending recession. From Torsten Slok (November 1, 2022):

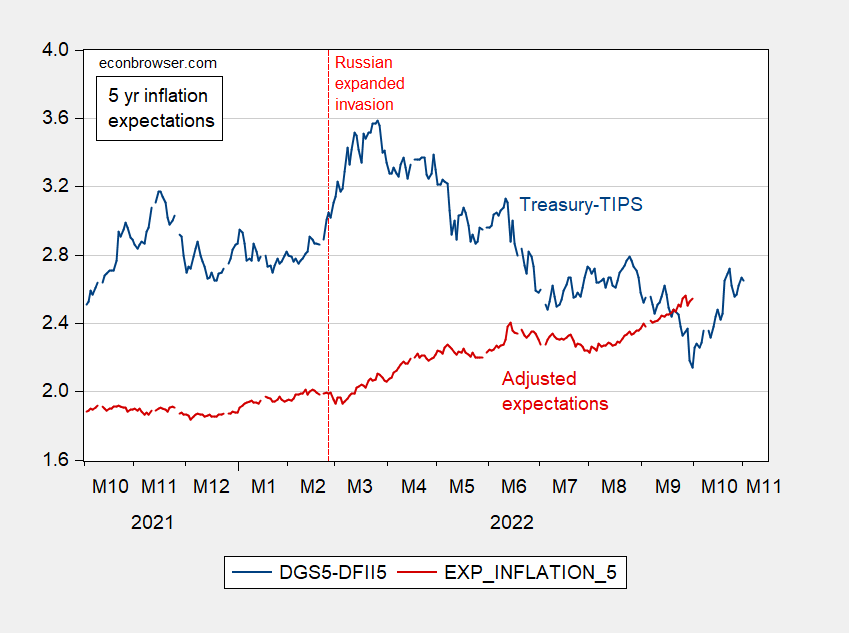

What about market-based inflation expectations? Within five years, expectations extrapolated directly from the Treasury-TIPS spread have recovered to end-August levels, but remain well below the March 2022 peak.

figure 2: The five-year inflation breakeven is calculated as the five-year Treasury yield minus the five-year TIPS yield (blue), and the five-year breakeven is adjusted by the inflation risk premium and the liquidity premium per DKW (red), both in %. Source: FRB via FRED, Treasury, KWW Following D’amico, Kim and Wei (DKW) access 11/2, and author’s calculations.

Having said that, as of the last available date at the end of September, inflation expectations estimates that take into account a premium have been trending upwards.

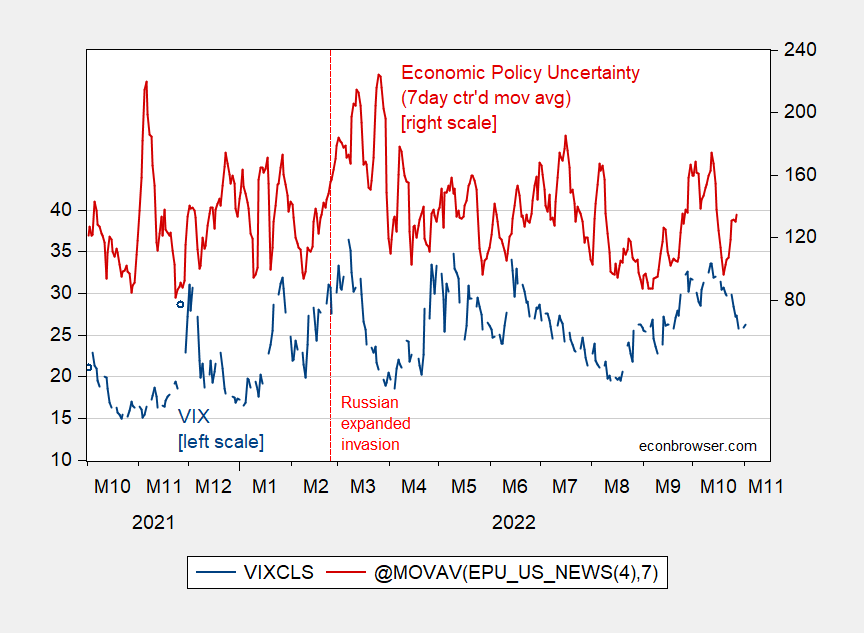

Finally, the VIX has cycled up and down, while the EPU has trended downward since a month after Russia’s expanded invasion.

image 3: 7-day central moving average of VIX (blue, left scale) and EPU (red, right scale). Source: CBOE via FRED, policyuncertainty.com.

{kind=link}

{kind=link}