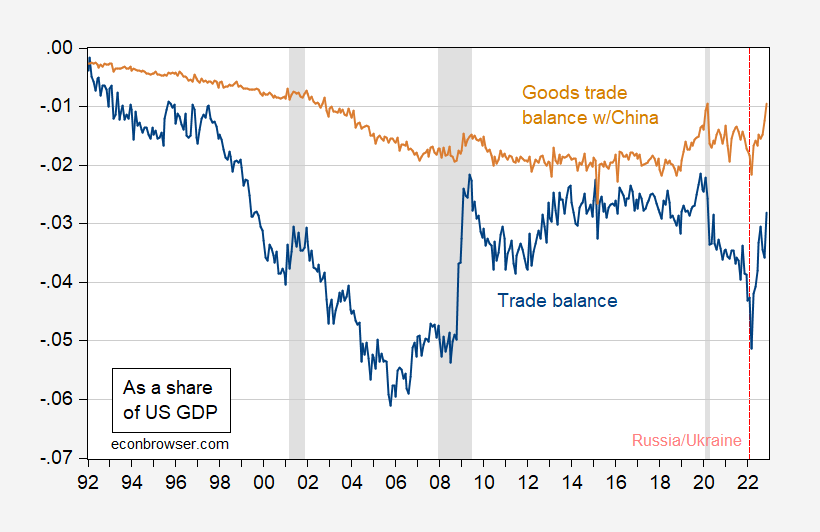

The trade balance rose to -$86.3 billion, compared with a Bloomberg consensus of -$96.3 billion. The trade deficit in goods with China has also shrunk significantly.

figure 1: Trade balance as a share of GDP (blue) and merchandise trade balance with China (tan). The authors use X-13 to seasonally adjust U.S. merchandise exports to and imports from China. GDP is IHS-Markit S&P Global. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. resource. BEA by FRED, IHS-Markit, NBER and author’s calculations.

The sharp improvement came as imports fell more than exports. Despite the sharp decline, at least some of the decline makes sense given past dollar depreciations.

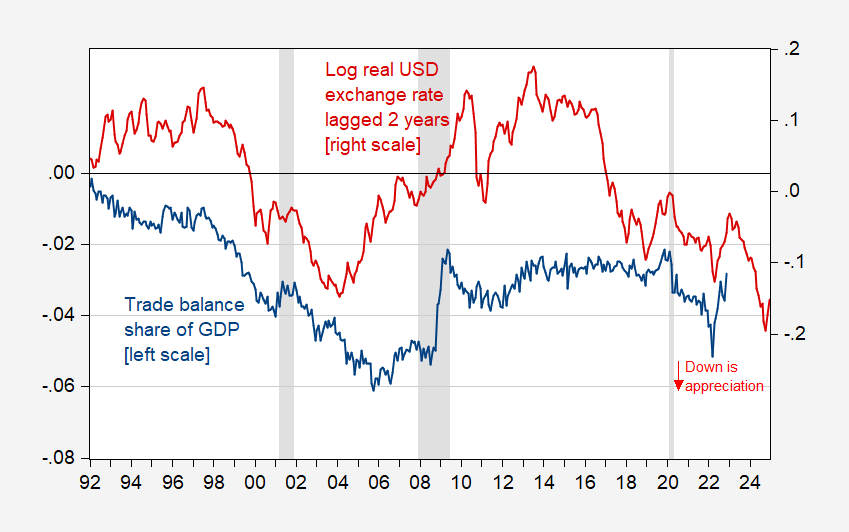

figure 2: Trade balance as a share of GDP (blue, left axis) and dollar real exchange rate against a basket of currencies, January 2006 = 0, lagged two years (red, right axis). GDP is IHS-Markit S&P Global. Real dollars are merchandise trade-weighted in 2005; weighted for merchandise and services trade thereafter. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. resource. BEA via FRED, Federal Reserve via FRED, HS-Markit, NBER and author’s calculations.

I have plotted the two series so they should show a positive correlation with a 2 year lag. Of course, during the most recent two-year period, this correlation manifested itself as expected. Having said that, with the dollar appreciating over the previous two years, we should expect the deficit to pick up somewhat, depending in part on domestic and foreign GDP developments.

Is the improvement in the trade balance good news in terms of GDP?Mechanistically, a smaller trade deficit implies estimated current GDP should be raised. On the other hand, if the decline in imports is due to lower demand for imports due to reduced spending, rather than a shift in spending, this would imply a dim outlook for future GDP growth.

I’m not sure if we can extrapolate from the composition of the decline in imports? On a percentage basis, consumer goods led the decline; however, given the surge in consumer spending on goods over the past year, I’m not sure what to make of that. The decline in imports of capital goods was much smaller, so this may not indicate a reduction in investment due to what is believed to be the early stages of a recession.

{kind=link}

{kind=link}