Today we are pleased to introduce you to Kevin Parrara, Luca Rossiand Fabrizio Venditti Bank of Italy. The views expressed in this note are those of the author and do not necessarily reflect the views of the Bank of Italy.

U.S. long-term yields rose about 1 percentage point between July and October before falling about 70 basis points between October and November. Popular models developed by the Federal Reserve attribute much of the variation in yields to the term premium, or the compensation investors require for holding long-term securities and the associated interest rate risk. A lively debate ensued over its implications for financial conditions, the real economy, and ultimately monetary policy. This column analyzes the rise in term premia within a coherent narrative across U.S. bond, equity and currency markets. Much of the growth since July can be attributed to the risk of higher long-term policy rates and lingering inflation risks. Since November, the cooling of labor market and inflation dynamics, coupled with dovish communications from the Federal Reserve, has led to a decline in term premiums.

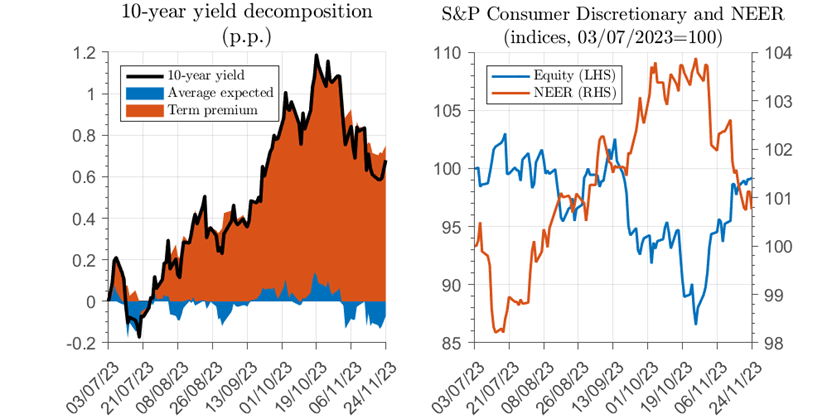

- Between July and October 2023, the U.S. 10-year Treasury bond yield rose 1 percentage point (to about 5%), while the yields on shorter-dated bonds were relatively stable. Market commentators linked the steepening yield curve to lower recession risks, the risk of higher long-term policy rates and news about a larger-than-expected primary deficit. The rise in yields has been accompanied by falling stock prices and an appreciating U.S. dollar. Long-term yields reversed course between October and November, falling about 70 basis points. A series of macroeconomic data showing a cooling labor market and slowing inflation, coupled with dovish comments from Federal Reserve officials, were the main drivers of the decline in yields.[1] Shares gained on most of the losses recorded in the previous two months, while the dollar weakened.

- According to a common decomposition of 10-year yields into expected rates and term premiums, the latter explains most of the variation in yields over this period (Figure 1, left panel). After rising about 1 percentage point, the term premium actually fell 30 basis points after November. The observed fluctuations in term premia have fueled debate about its determinants and their impact on financial conditions, the real economy, and ultimately monetary policy. For example, Dallas Fed President Lorie Logan made this argument when commenting on the rise in term premia since July: “Financial conditions have tightened significantly in recent months. But the reasons for the crunch are important.If long-term interest rates remain high due to higher term premiums, there may be less need to raise the federal funds rate”.[2] more generally, Changes in the term premium are often viewed as exogenous shocks to financial conditions, affecting the economy much like monetary policy. In fact, market commentators often highlight these market movements and state that “the market is doing its job.”

figure 1. Bond yields, stock prices and exchange rates. Note: The left chart shows cumulative daily changes since July 3RD2023 to November 24th, 2023. The stock data on the right refers to S&P Consumer Discretionary. Source: Federal Reserve Bank of San Francisco, Refinitiv.

Model-based narrative of term premium fluctuations

- A coherent narrative linking the rise in term premia to broader developments in U.S. financial markets can be gleaned from daily econometric models that decompose asset prices into structural shocks. The decomposition is obtained through Bayesian vector autoregression (BVAR), which includes term premium, S&P Consumer Discretionary, nominal effective exchange rate (NEER) and 10-year inflation compensation (ILS) as endogenous variables. The model is estimated using daily data between early December 2008 and late November 2023 and includes four lags.

- The model decomposes asset prices into four structural shocks: domestic demand Shocked, a Monetary Policy Shocked, one Inflation risk premium shocked and risk appetite Shock.

- A Domestic demand shock Upside risk through growth increases term premiums and thus real interest rates.

- in the case of Monetary PolicyThe common view is that traditional monetary policy mainly affects long-term interest rates through expected interest rates rather than term premiums. This view has been challenged by empirical evidence (Gertler and Karadi, 2015a,b; Hanson and Stein, 2015; Gilchrist, López-Salido, and Zakrajšek, 2015; Kaminska, Mumtaz, and Šustek, 2021) as well as theoretical models. Financial friction. For example, an important transmission channel is mortgage refinancing (Hanson, 2014). In the United States, most mortgages are offered at fixed rates, and when interest rates fall, households have an incentive to pay off their old mortgages early and refinance at a lower rate. The effective life of outstanding securities related to the mortgage market (such as mortgage-backed securities, MBS) declines as lenders expect to be repaid more quickly. Investors who prefer longer maturities increase demand for longer-dated government bonds, causing term premiums to fall. When interest rates rise, the opposite is true.

- one Inflation risk premium shock Captures pressure on term premia from higher inflation risk (and therefore higher nominal interest rate risk) due to supply shocks and concerns about debt sustainability. [3]

- the last one risk appetite shock Reflects changes in interest in safe assets due to financial or geopolitical uncertainty.

- Between early July and the end of October, rising inflation risks and tightening monetary policy were the main reasons for the surge in term premiums. Figure 2 (left panel) shows that the main driving force for maintaining the increase in term premium from July to October is the impact of monetary policy, especially after September 20th The FMOC meeting and the shock to inflation risks translated concerns about an overheating economy into rising yields. Together, these shocks are responsible for more than three-quarters of the surge in term premiums. In terms of stock prices (middle panel), the combined negative effects of monetary policy and inflation risk shocks are only partially mitigated by positive domestic demand shocks. This result can be explained by a simple discount model, where the stock price equals the discounted sum of future earnings. Better demand prospects boost earnings discount flows and push share prices higher. But this effect is offset by higher discount rates (yields), which are underpinned by a tighter policy stance and higher inflation risks. As for inflation compensation (below), the model breakdown shows that its stability over these months reflects the tug-of-war between lingering inflation risks and the Fed's efforts to control inflation. In fact, inflation risk shocks push up inflation compensation, but are completely offset by contractionary monetary policy shocks.

- Between October and November, financial conditions eased and term premiums fell. The latest macroeconomic data, namely a softer labor market, lower consumer inflation and softer retail sales, have contributed to a decline in term premiums over the past month. This shows that domestic demand is more fragile and the risk of rising inflation is reduced (contribution of domestic demand and inflation risk premium shocks in the right panel of Figure 2). Meanwhile, at the Federal Open Market Committee (FOMC) meeting on November 1, Powell acknowledged that forecasts for future interest rate hikes were not set in stone. Powell said the Fed may have ended its tightening cycle as it refrained from raising rates at its second consecutive policy meeting. As uncertainty surrounding the stance of monetary policy decreases, this translates into a compression of the term premium (the contribution of monetary policy shocks in the right-hand panel of Figure 2). The Fed's shift to a less hawkish stance sparked the most significant synchronized rally since November 2022, with stocks and bonds rising in tandem.

policy impact

- Many observers and some Fed officials believe that yield changes are similar to monetary policy shocks insofar as they reflect changes in term premia., No further policy changes are therefore required.

- Our results suggest that the issue is more nuanced and that the implications for monetary policy depend on the specific factors behind changes in term premia. The model shows that movements in term premiums over the past four months partly reflect the fact that the market is pricing policy rates risk converted into long-term yields. These risks affect the economy just like monetary policy, so there is no need for the Fed to take action. However, it is partly a sign of volatility among bond investors concerned about rising long-term inflation risks caused by a variety of factors. If these risks translate into sustained changes in long-term inflation expectations, policy action by the Fed will be required.

refer to

Gertler, M., & Kalady, P. (2015a). Monetary policy surprises, credit costs, and economic activity. American Economic Journal: Macroeconomics, 7(1), 44-76.

Gertler, M., & Karadi, P. (2015b). Monetary policy and the cost of credit. VoxEU column, CEPR.

Gilchrist, S., López-Salido, D., & Zakrajšek, E. (2015). Monetary policy and real borrowing costs are at the zero lower bound. American Economic Journal: Macroeconomics, 7(1), 77-109.

Hansen, S. G. (2014). Mortgage convexity. Journal of Financial Economics, 113(2), 270-299.

Hansen, S. G., and Stein, J. C. (2015). Monetary policy and long-term real interest rates. Journal of Financial Economics, 115(3), 429-448.

Kaminska, I., Mumtaz, H., & Šustek, R. (2021). Monetary policy surprises and their transmission through term premia and expected interest rates. Journal of Monetary Economics, 124, 48-65.

notes

[1]For example, see It seems like something is givingspeech by Federal Reserve Board of Governors Member Christopher J. Waller, November 28, 2023.

[2] Financial conditions and monetary policy outlookRemarks by Lorie K. Logan, President of the Federal Reserve Bank of Dallas, October 9th In 2023, San Francisco Federal Reserve Chairman Daly and Board of Governors member Waller expressed similar views.

[3] Unexpected rises in economic activity and inflation sometimes cause such shocks, as investors may interpret them as signs of an overheating economy, creating a significant risk of rising inflation. This leads them to demand higher compensation for holding long-term bonds, negatively impacting stock prices. It is this effect on stock prices that distinguishes it from demand shocks.

The author of this article is Kevin Parrara, Luca Rossiand Fabrizio Venditti.

{kind=link}

{kind=link}