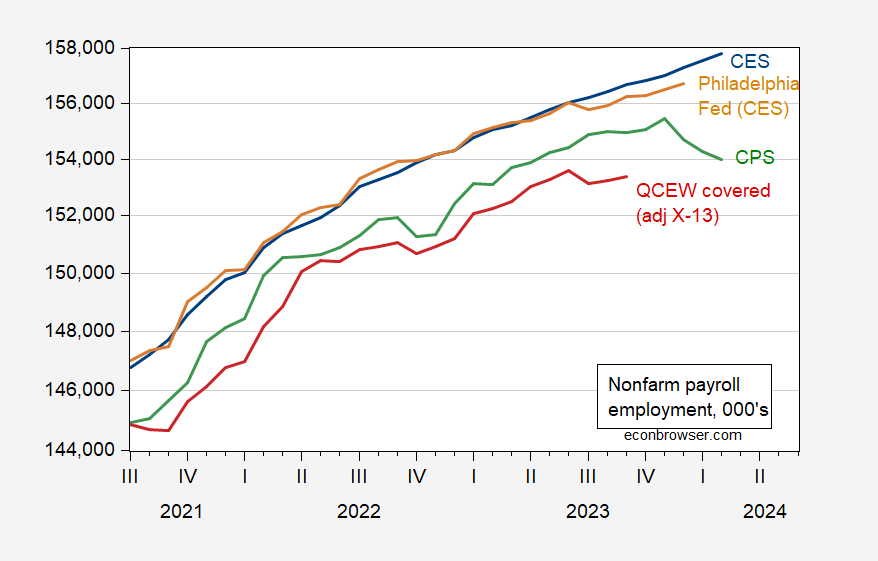

An early benchmark from the Philadelphia Fed suggests a lower trajectory for nonfarm payrolls than the CES indicator suggests, at about 600,000. How does this change the image?

figure 1: Nonfarm payrolls from the agency survey (blue), nonfarm payrolls from the Philadelphia Fed's early benchmark (tan), nonfarm payrolls from the household survey (green), adjusted for the nonfarm payrolls concept, and QCEW employment numbers (red) seasonally adjusted by the authors using X-13, all in thousands. Source: BLS via FRED, Philadelphia FedBLS, BLS (QCEW), and author's calculations.

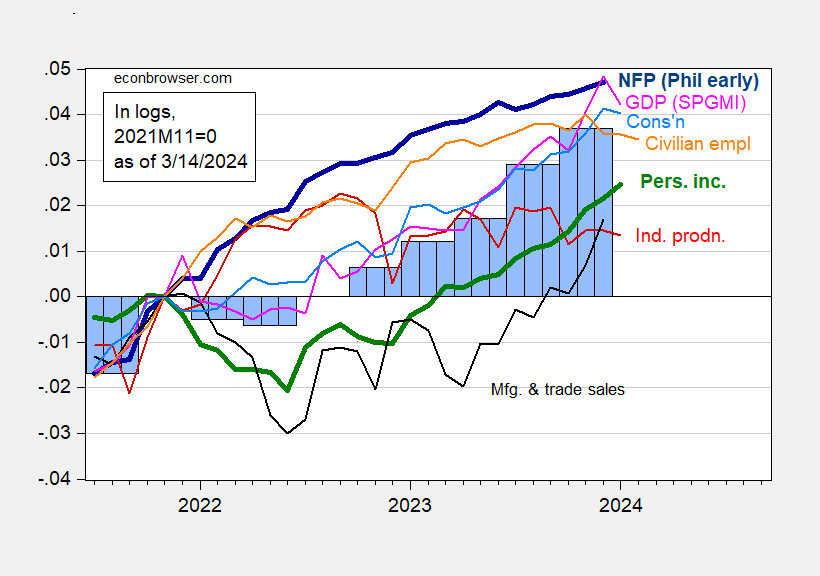

For 2022, year-over-year growth using the official BLS indicator is 2% and year-over-year growth using the Philadelphia Fed post-benchmark indicator is 1.6% (growth using state sums is 0.5%; however, the Philadelphia Fed Banks warn against using this indicator). Therefore, early benchmarks suggest that the labor market is less “hot” but still growing.

Note that, in context, this does not change the overall picture of the business cycle.

figure 1: Philadelphia Fed Early Benchmark Nonfarm Employment (bold dark blue), Civilian Employment (orange), Industrial Production (red), 2017 Personal Income $ excluding current transfers (bold green), 2017 Manufacturing and trade sales $ (black), 2017 consumption (light blue), 2017 monthly GDP (pink), third release GDP (blue bar), all logarithms normalized to 2021 M11=0 . Data source: U.S. Bureau of Labor Statistics (BLS) through FRED, Federal Reserve, BEA 2023 Q4 2nd Edition, S&P Global Market Insights (Nigerian macroeconomic consultant, IHS Markit) (3/1/Released in 2024) and the author's calculations.

You can compare it with the official NFP series pictures. here.

{kind=link}

{kind=link}