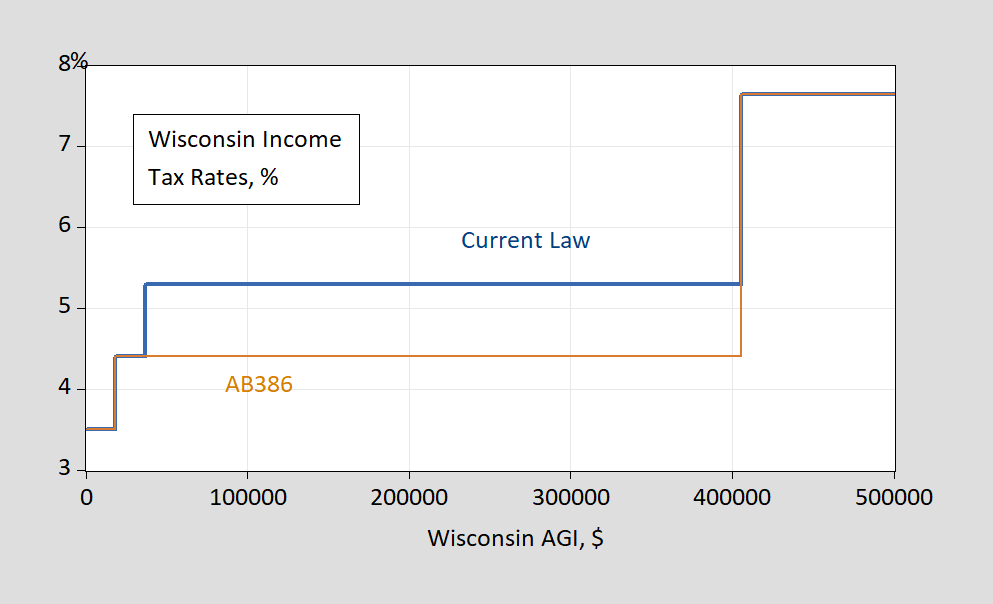

CROWE and Young America’s Foundation are bringing Arthur Laffer will speak today at UW-Madison (Grainger Hall, Plenary Room, 5:30-6:30 CT).The timing was fortuitous because State Senate is pushing to pass AB386which would exempt some retirees from tax on their income (up to $100,000 for single filers and $150,000 for married filing jointly) and lower tax rates.

figure 1: Wisconsin marginal income tax rates, current law (blue) and AB386 (tan), for married filing jointly.

I’m sure some people will say this will boost the economy and increase tax revenue. The Wisconsin Legislative Fiscal Bureau (the state counterpart to the CBO on this issue) says no to the latter (see page 4) this file).

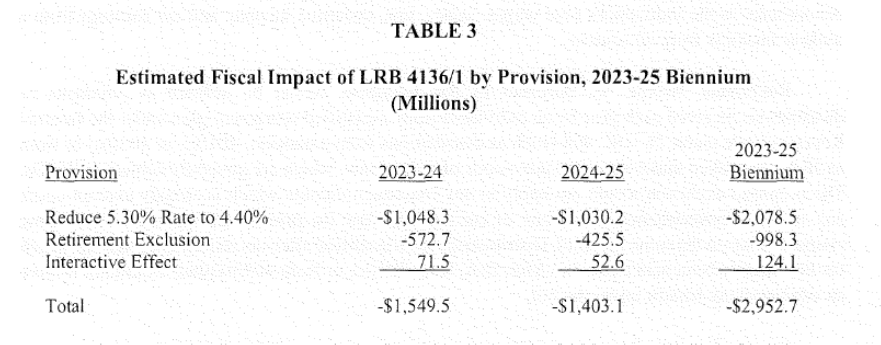

The bill is expected to reduce personal income taxes by $1,549.5 million in 2023-24 and $1,403.1 million in 2024-25.This estimate and the accompanying allocation table are based on

Simulations performed by DOR.Table 3 shows the bill’s fiscal estimates for each of the 2023-25 biennium. As shown, the estimates include interaction effects, which can occur when multiple tax law changes affect an individual’s tax liability. The estimate for 2023-24 also includes a one-time revenue impact caused by the timing difference between the state’s fiscal year and tax year.

Two-thirds of the cost will be attributable to the reduction in tax rates.

source: LFB through the Joint Finance Committee.

Guo, Ruhl and Seshadri (2023) CROWE presents estimates of the benefits of partial tax rate reductions. In their analysis, output, employment, and capital stock all increase, but overall tax revenue (business, sales, income) decreases (however, none of their scenarios are consistent with the proposals in AB386).

For comparison, under the same circumstances (2% for the lowest two tax brackets and 4.5% for the highest two tax brackets), Guo et al. (2023), using a general equilibrium model, found that overall tax revenue decreased by 13.53% in the long run. In comparison, the LFB analysis excluding long-term responses decreased by 23.5%.

{kind=link}

{kind=link}