Today’s post is a complement to my post from earlier this week – So-called “Team Transitory” declared winner (January 8, 2024). Yesterday (January 10, 2024), the Australian Bureau of Statistics released the latest data— Monthly consumer price index indicator – In November 2023, inflation fell sharply again. These figures are the closest we have to current realities, and it is clear that the decline in inflation that began in September 2022 is continuing at a considerable pace. The annual interest rate has now dropped to 4.3% from 4.9% in October 2023. The main driver of inflation over the past few years has been fuel prices, with motor fuel inflation falling from 19.7% in September 2023 to 2.3% in September 2023. In November 2023, as global factors are quite independent of domestic monetary policy. In fact, over time we get a clear reinforcement of the ephemeral narrative driven by supply factors rather than demand factors. A recent research paper from the European Central Bank also underlines this statement – What drives core inflation?The role of supply shocks (Published November 13, 2023). Overall, the data now expose the folly of a neo-Keynesian approach to macroeconomic policy, which prioritizes monetary policy as a counter-stabilizing tool and assumes that inflationary events are caused by excessive government spending.

Australian inflation continues to fall sharply

ABS Media Release (January 10, 2024) – As of November 2023, the monthly CPI indicator has increased by 4.3% annually. – Point out:

This month’s 4.3% annual growth rate was lower than October’s 4.9% gain and was the smallest annual growth rate since January 2022…

The largest contributors to annual growth in November were housing (+6.6%), food and non-alcoholic beverages (+4.6%), insurance and financial services (+8.8%), and alcohol and tobacco (+6.4%)…

Annual inflation for motor fuels has fallen to 2.3% in November from 19.7% in September 2023. This is an important reason for the low annual growth rate of monthly CPI indicators in the past two months.

Some observations:

1. The sharp drop in gasoline prices has nothing to do with the Reserve Bank of Australia raising interest rates, but an “important” reason for such a rapid decline in inflation – supply-side factors.

2. Rising rents are partly due to the Reserve Bank of Australia's own interest rate hikes, as landlords in a tight housing market simply pass on higher borrowing costs – so so-called anti-inflation rate hikes are actually driving inflation .

3. Rent increases were partially offset by increases in federal rental assistance, suggesting that more generous fiscal policy at this stage could significantly reduce inflation further.

4. Electricity prices are rising because of administrative decisions that allow poorly regulated, privatized power companies to push electricity prices higher than cost increases.

5. A series of natural disasters (floods, fires) caused by climate change will lead to an increase in insurance costs and are insensitive to interest rate increases.

6. None of the other major drivers are sensitive to rising interest rates and change for reasons unrelated to changes in monetary policy.

The overall conclusion is that the global factors driving inflationary pressures are weakening rapidly as the world adjusts to the coronavirus pandemic, Ukraine and OPEC profiteering.

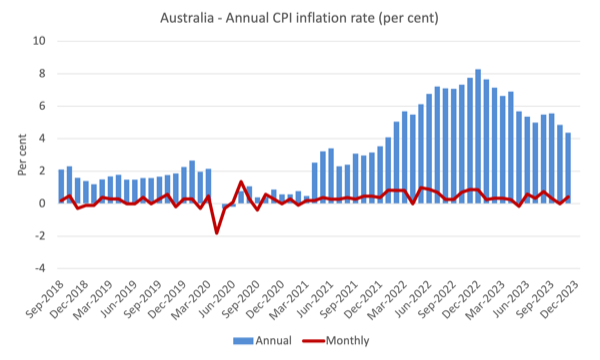

The next chart shows that the annual inflation rate is heading in one direction – falling rapidly.

The blue column shows the annual rate, and the red line shows the month-to-month change in CPI for all items.

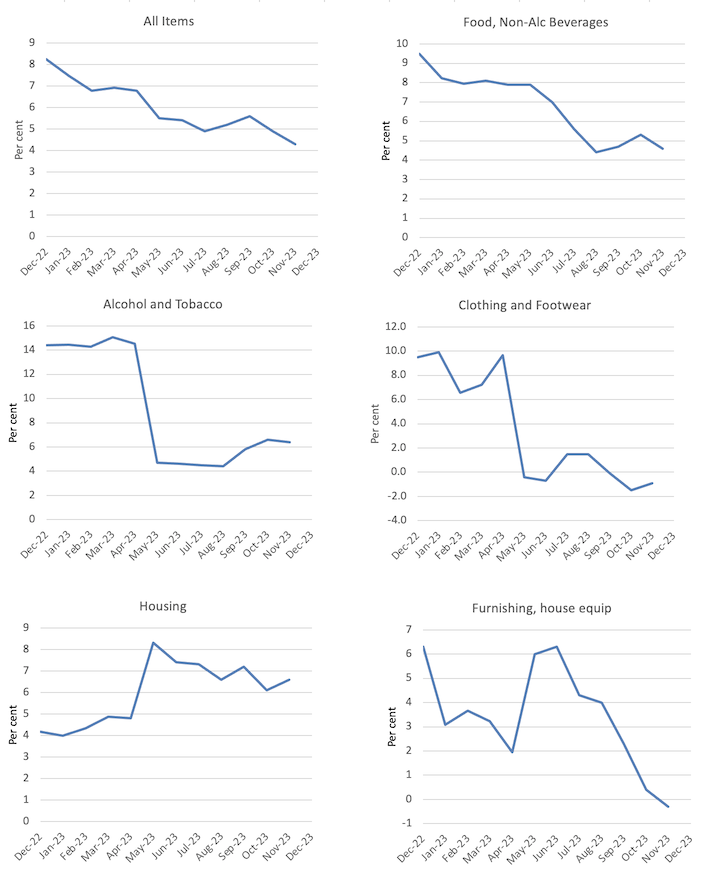

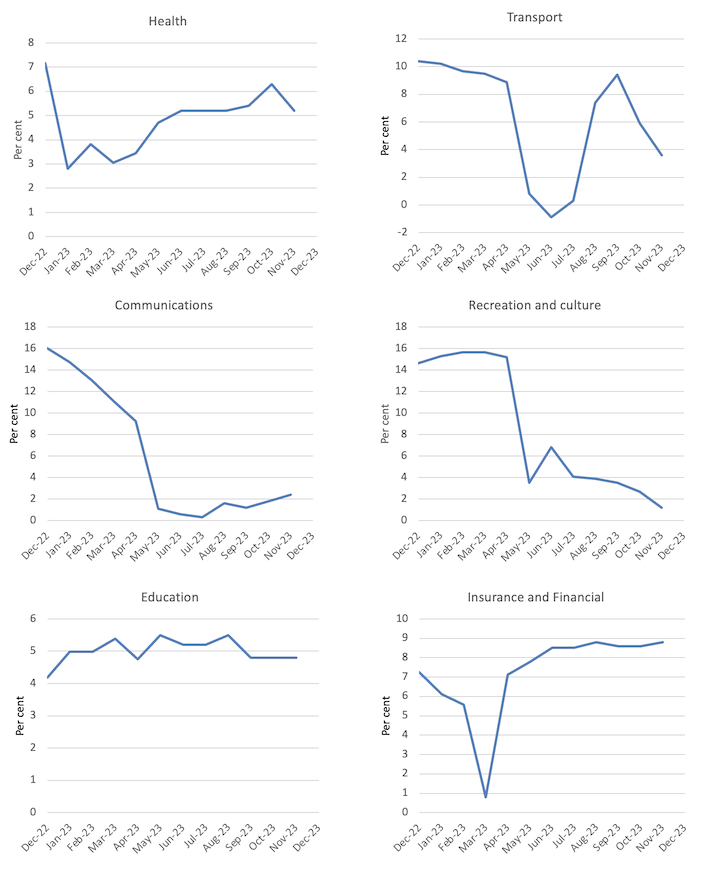

The chart below shows the changes in the main components of CPI for all projects from December 2022 to November 2023.

Overall, as noted above, price growth has fallen sharply across most components and the exceptions do not provide any justification for further rate hikes by the RBA.

Overall, inflation is falling as supply factors ease.

RBA’s fictional NAIRU

One of the problems with the New Keynesian approach is its insistence that the so-called non-accelerating inflation rate of unemployment (NAIRU) should guide monetary policy.

This is what mainstream textbook garbage says If the unemployment rate is below the NAIRU, inflation will accelerate; if the unemployment rate is above the NAIRU, inflation will fall.

Logically, NAIRU defines a state in which inflation is stable.

I reject this logic, but let's use it to test its internal consistency.

Even though inflation is falling rapidly, the RBA is currently claiming to be justified in raising interest rates as they claim the NAIRU (unobservable, but econometrically estimated) is around 4.25%.

With the unemployment rate currently at 3.9%, NAIRU logic should see inflation continuing to accelerate.

On this basis, as inflation falls, the RBA's statement is clearly wrong, even if we accept that there is a definable NAIRU that can be measured in some way.

I discuss this in more detail in this post (and others) – Mainstream logic should conclude that Australia's unemployment rate is higher than the NAIRU, not lower than the NAIRU as the Reserve Bank of Australia claims. (July 24, 2023).

The key is that, according to NAIRU logic, if the unemployment rate is below NAIRU, then inflation should accelerate; if the unemployment rate is above NAIRU, inflation should decelerate.

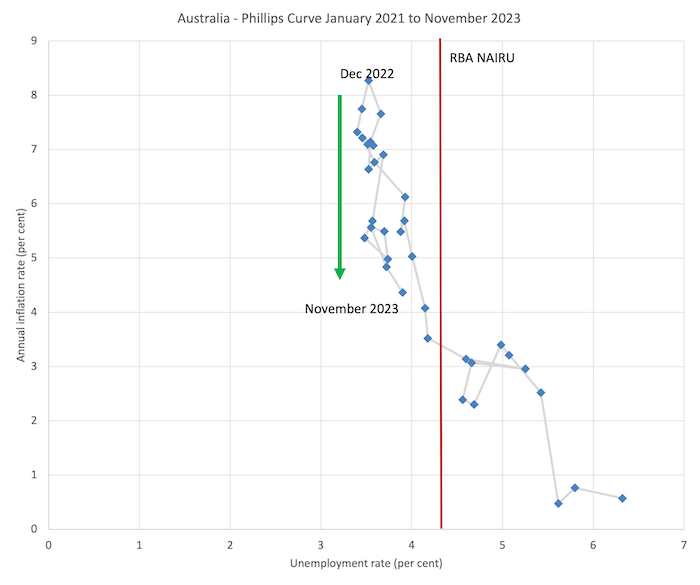

The facts are shown in the chart below, which is a graph of the Philip Curve from January 2021 (before inflation accelerated) to November 2023.

The Phillips Curve depicts the relationship between the unemployment rate (horizontal axis) and an inflation measure on the vertical axis.

Judging from the situation in Australia over the past two years, the situation is very obvious.

The unemployment rate has been very stable, fluctuating within a narrow range, over the past year or so, but the inflation rate has been falling since last September (green arrow).

This means that logically, NAIRU cannot be higher than the current unemployment rate, but must be lower than the current unemployment rate.

This means the RBA's insistence on adding 140,000 extra workers to the unemployment scrap heap is unfounded even within the theoretical framework they believe in.

The vertical red line is the RBA's NAIRU, which overlaps with an inflation rate of just over 3%.

But at this rate of inflation, with a wide range of unemployment rates – from 4.1% to 5.3% (approximately), if I were to run an econometric model to formally estimate NAIRU, I would get a wide confidence interval, at This is a range within which I cannot statistically discriminate—in other words, NAIRU's estimates are useless for policy.

NAIRU estimates are simply a tool used by ideologues who want to increase unemployment and give businesses more bargaining power.

The latest inflation peak occurred in December 2022, and has been declining steadily since then, with minor fluctuations in April 2023.

But look at how far the unemployment rate has fallen?

Very narrow.

Therefore, NAIRU cannot be 4.25%, logically it must be lower than 3.7%.

ECB study shows minimal impact on demand

One of the themes among economic commentators over the past few years has been that inflationary pressures show that Modern Monetary Theory (MMT) is a failed theory.

As a corollary, Modern Monetary Theory economists claim that the rising fiscal deficits and falling interest rates that have accompanied the policy response to the pandemic are unlikely to spark inflation.

The corollary is that MMT economists mistakenly believed that fiscal deficits were “irrelevant” and that demand expansion led to inflation, as the mainstream predicted.

Of course, the inferences and inferences are related to the “straw man” version of MMT, which has nothing to do with the body of work I was involved in developing.

All spending carries inflation risk.

The fiscal deficit must be adjusted to fill the spending gap left by non-government savings decisions.

The fiscal deficit may be too large, and the assessment depends on the circumstances – does the country have an external deficit? What is the savings-investment balance of the domestic private sector?

Furthermore, assuming that MMT is a policy regime demonstrates a fundamental ignorance of what MMT actually is…

More importantly, against this background, when the epidemic occurs and distorts the supply and demand pattern of commodities, there will obviously be some inflationary pressure.

The supply of goods and services is severely restricted.

Access to services is limited by health policies.

Revenues are maintained by government support expenditures.

People were confined to their homes, had a lot of time to work on DIY projects, and the internet was still available to place orders.

As people shift their spending away from going to cafes and theaters and towards buying home improvement tools, the supply of goods cannot adapt fast enough to the higher demand for goods!

However, overall demand (spending) is not well above trend.

Against this backdrop, it is clear that inflation is not a problem of excessive spending, but a supply problem exacerbated by Ukraine and OPEC+.

The solution then was not to cut spending – that's what central banks thought they were doing when they raised interest rates.

The Bank of Japan's solution is to wait for supply constraints to lift and keep interest rates unchanged while the government provides some financial support to low-income households to ease temporary cost-of-living pressures.

Japan's policy response has been overwhelmingly proven to be appropriate and contrary to the approach suggested by mainstream macroeconomics.

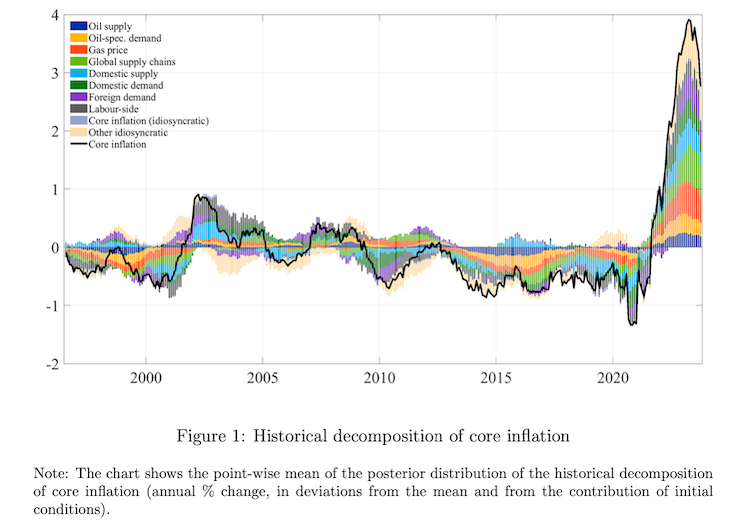

Some recent studies published by the European Central Bank reinforce this conclusion.

In the paper cited in the introduction, the researchers “propose a framework to identify a rich set of structural drivers of inflation to understand the role of multiple and concomitant sources of post-pandemic inflation spikes”.

In other words, they developed a statistical method to distinguish supply and demand factors related to the emergence of inflationary pressures.

Their conclusion is:

Overall, supply shocks can explain much of the post-pandemic inflation surge, as well as core inflation…Shocks related to global supply chains, gas prices and oil markets are all pushing in the same direction, supporting 'bad luck' ” statement to the period of high inflation.

Read it several times.

They also find that the contribution of “labour shocks” (wage pressures) is negligible, again contradicting the argument that unemployment must rise to suppress wage pressures as a solution to inflation.

This chart (ECB Chart 1) summarizes the various factors that make up the breakdown of the overall inflation effect.

in conclusion

The mainstream macroeconomics community has an incredible ability to deny evidence.

Even though it is clear that inflationary pressures are not caused by excessive demand even in 2021, the way in which the central bank has defended a sharp increase in interest rates is shocking.

But I’ve been in this business for a long time, and I’m used to the deception and blindness that comes from groupthink.

If anyone looked down from other planets to people more dedicated to the truth, they would think how stupid humans are to believe these mainstream economists, when it is obvious that they are only self-serving and reinforcing the dominance of the elite.

That's enough for today!

(c) Copyright 2024 William Mitchell. all rights reserved.

{kind=link}

{kind=link}