Today (February 28, 2024), the Australian Bureau of Statistics (ABS) released the latest data— Monthly consumer price index indicator – Figures for January 2024 show that Australia’s inflation rate is stable at 3.4%, but like the rest of the world, it is still on a downward trajectory. Today's data is the closest to current reality, showing inflation at 3.4% in January 2024, but many key drivers are now falling steadily. The trajectory is firmly downward. As shown below, the only component of the rise in CPI was either due to short-lived external factors beyond the RBA's control or was caused by the RBA rate hike itself. All that raising interest rates does is cause a huge shift in the distribution of income from the poor to the rich. Australia's economic slowdown is mainly due to fiscal drag rather than rising interest rates.

The latest ABS CPI monthly data for January 2024 shows:

- The CPI indicator for all groups remained stable at 3.4%.

- Food and non-alcoholic beverages rose 4.4% (versus 4% in December).

- Clothing and footwear rose 0.4% (-0.8% in December).

- Housing grew 4.6% (versus 5.2% in December).

- Furniture and household equipment rose 0.3% (-0.3% in December).

- The health index increased by 3.9% (4.7% in December).

- Transportation 3% (3.6% in December).

- Communications 2% (2% in December).

- Entertainment & Culture -1.7% (-2.4% in December).

- Education 4.7% (4.7% in December).

- Insurance and financial services were steady at 8.2%.

ABS Media Release (February 28, 2024) – The monthly CPI measure rose 3.4% in the year to January 2024 – Point out:

The monthly Consumer Price Index (CPI) gauge rose 3.4% in the 12 months to January 2024…

The annual inflation rate in the monthly CPI indicator was stable at 3.4%, still the lowest annual inflation rate since November 2021…

The largest contributors to annual growth in January were housing (+4.6%), food and non-alcoholic beverages (+4.4%), alcohol and tobacco (+6.7%), and insurance and financial services (+8.2%). Leisure and culture (-1.7%) partially offset annual growth, mainly due to holiday travel and accommodation (-7.1%)…

Rental prices rose 7.4% in the 12 months to January, reflecting a tight rental market and low vacancy rates nationwide…

Annual electricity prices increased by 0.8% in the 12 months to January 2024. The introduction of Energy Bill Relief Fund rebates for eligible households from July 2023 has largely offset increases in electricity prices due to higher wholesale electricity prices in the annual price review in July.

So some observations:

1. Inflation has stabilized and will continue to decline in the coming months.

2. Housing inflation has fallen to 4.6% in January from 5.2% in December, while rental inflation remains an issue.

3. Rent increases are partly due to the Reserve Bank of Australia raising interest rates themselves, as landlords in a tight housing market simply pass on higher borrowing costs – so so-called anti-inflation rate hikes are actually driving inflation.

4. It is worth noting that fiscal policy measures on electricity prices have effectively eliminated this pressure.

The federal government could have done more to ease the pressure on families caused by temporary increases in the cost of living over the past two years.

Note that the growth of FIRE services is partly due to banks' profit-seeking efforts.

The overall conclusion is that the global factors driving inflationary pressures are weakening rapidly as the world adjusts to the coronavirus pandemic, Ukraine and OPEC profiteering.

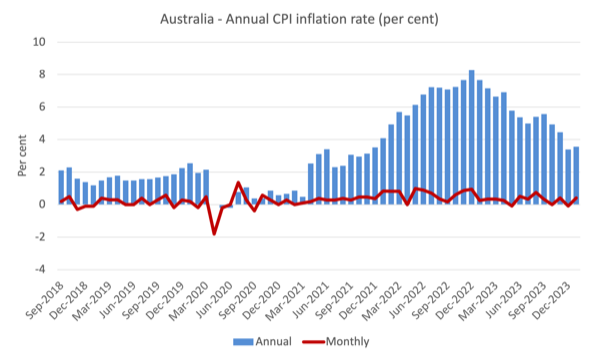

The next chart shows that the annual inflation rate is moving in one direction – month-to-month changes reflect special events or adjustments (such as annual index schedules, etc.).

The blue column shows the annual rate, and the red line shows the month-to-month change in CPI for all items.

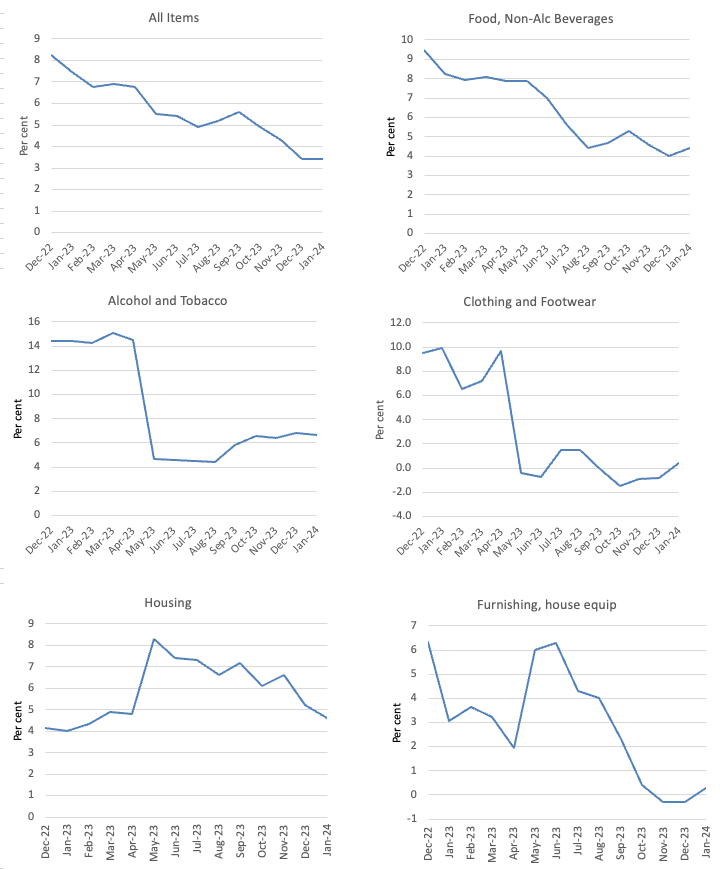

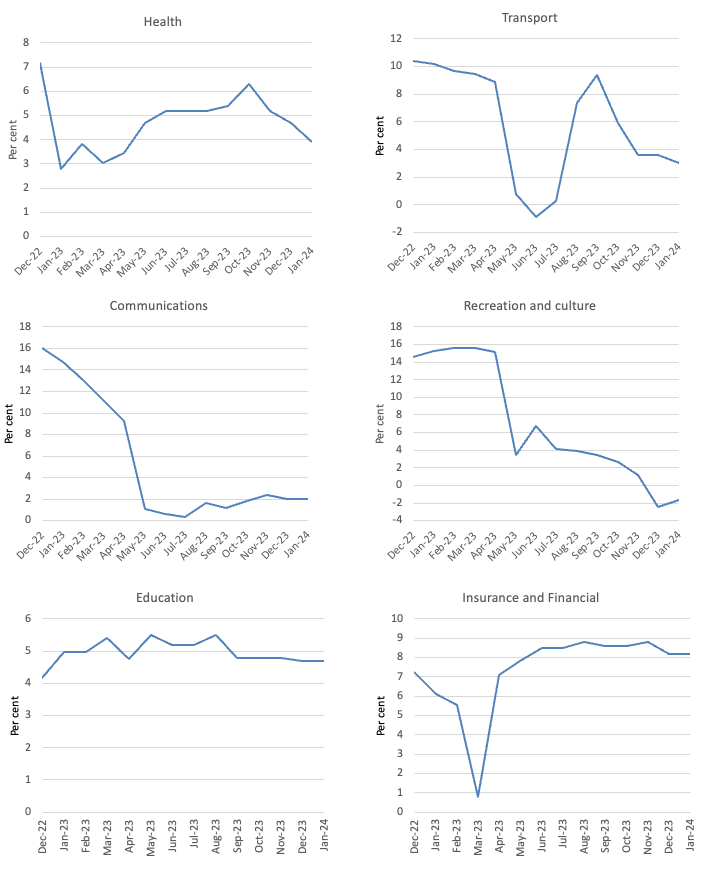

The chart below shows the changes in the main components of CPI for all projects between December 2022 and January 2024.

Overall, as noted above, price growth has fallen sharply across most components and the exceptions do not provide any justification for further rate hikes by the RBA.

For example, the entertainment and culture segment that drove inflation in 2023 is now deflating—reflecting only a temporary rebound in travel and related activities after widespread lockdowns and other restrictions early in the pandemic.

It always adjusts back to more normal behavior.

Overall, inflation is falling as supply factors ease.

Food ingredients are also sensitive to supermarket practices.

Just yesterday there were reports of huge profit margins resulting from price gouging in the retail sector supplying food and groceries.

ABC News Report (February 27, 2024) — Coles accused of cheating customers as they struggled to put food on table – According to the report, Coles Group, one of Australia’s two largest supermarket companies, controls about 64% of the market share in Australia, while Aldi accounts for about 10%. The group announced another increase in the six months to December 2023. A huge profit.

Gross margins at Coles and Woolworths are around 26% to 27%, which is ridiculously high for companies that offer food, a stable commodity.

During periods of inflation, Coles' profit margins rose, which was prima facie evidence of fraud.

The company claims:

Our profits allow us to continue to invest in our business and serve our stakeholders – whether they are our customers, suppliers, team members, community partners or shareholders – and we are working hard to deliver good across the board Results.

But the evidence shows that returns to shareholders are higher, investments are lower, and supplier squeezes are common.

Furthermore, it is extremely disingenuous to attempt to claim that the returns they generate benefit their “clients” (which indeed expands the meaning of “stakeholder”).

The point is, if the two dominant companies – effectively forming an oligopoly – do not have enough discretion to push profit margins higher under the cover of overall price pressures in the economy, then CPI inflation will be higher than Currently much lower.

This has nothing to do with wages or excessive demand pressures, but rather with excessive concentration in an industry that should be more tightly regulated.

Asymmetry in Monetary Policy

Economists who support using interest rates to change the level of spending in the economy (that is, most economists) believe that the fall in inflation is a direct result of the RBA raising interest rates.

They point to slower GDP growth and falling retail sales data as evidence to support their view.

However, they ignore the fact that over the past 12 months, fiscal policy has shifted from generating deficits to generating surpluses.

During the global financial crisis, the Australian Treasury conducted research to estimate the relative contribution of monetary and fiscal policy to a modest recovery in GDP following the large global financial shock we imported.

The Reserve Bank of Australia has cut interest rates as the federal government undertakes several discretionary spending initiatives, while the Treasury has overseen a significant increase in the fiscal deficit.

They estimate that fiscal stimulus contributed significantly to quarterly growth rates during the first four quarters of the global financial crisis (the December quarter).

On December 8, 2009, the Federal Ministry of Finance issued a report entitled – Fiscal policy returns – Attended the 2009 Australian Business Economists Annual Forecast Conference.

I wrote about this in this article – Today’s lesson: The public sector saved us (December 21, 2009).

While I disagree with most of the theories presented by Treasury in their paper, the charts they provide are interesting.

They pointed out:

Figure 10 shows the Treasury's estimate of the impact of discretionary fiscal stimulus packages on quarterly GDP growth. These estimates suggest that discretionary fiscal action provided substantial support to domestic economic growth in each quarter of the year to the September 2009 quarter – with its largest impact in the June quarter…

These estimates imply that, without a discretionary fiscal package, real GDP would have contracted not only in the December 2008 quarter (which it did) but also in the March and June 2009 quarters, so that the economy would have contracted in 2008 The December quarter contracted sharply. In the year to June 2009, growth fell short of expectations of 0.6%.

Although many economists claimed at the time that no fiscal response was necessary, it was clear that without intervention Australia would be stuck in a three-quarter recession.

Another interesting part of their work is estimating the impact on GDP growth of a rapid rate cut by the Reserve Bank.

This analysis provides a direct comparison between expansionary fiscal policy and easy monetary policy.

The conclusion is clear:

…As of the third quarter of 2009, the fall in real borrowing rates contributed less than 1% to GDP growth, while the estimated contribution of discretionary fiscal packages during the same period was about 2.4%.

Therefore, the effect of discretionary fiscal policy changes is estimated to be about 2.4 times greater than that of monetary policy changes (a record high).

Think about it now.

Since May 2022, interest rates have been raised 11 times.

But at the same time, the fiscal balance has shifted from a deficit of 6.4% of GDP in 2020-21 and a deficit of 1.4% of GDP in 2021-22. Surplus of 0.9% of GDP in 2022-23.

The federal government expects another surplus this financial year.

This is a significant fiscal shift, and fiscal drag is the main reason for the slowdown in growth and spending.

But there are also asymmetries in monetary policy, related to the spending propensities of different income groups affected by interest rate changes.

Higher-income groups have a lower marginal propensity to consume (meaning they save more for each additional dollar of disposable income) than lower-income households.

They also have more financial wealth.

When interest rates rise, low-income households' total expenses don't change much because they already spend all their income.

Only the ingredients have changed.

They also have little financial wealth and therefore cannot capture any income growth through rising returns.

For high-income households, their financial asset income increased significantly, and although they saved more than low-income households, their spending increased through the wealth effect.

These changes do not work in reverse.

Therefore, the slowdown in GDP is more likely to be the result of fiscal drag than rising interest rates.

in conclusion

The latest consumer price index data shows that, like the rest of the world, inflation in Australia is now under control and on a downward trajectory.

The reason for the decline is simple – the factors driving inflation are weakening.

And these factors – supply constraints, the impact of the Russian invasion, OPEC price gouging – are not sensitive to the RBA raising interest rates.

All that raising interest rates does is cause a huge shift in the distribution of income from the poor to the rich.

Australia's economic slowdown is mainly due to fiscal drag rather than rising interest rates.

That's enough for today!

(c) Copyright 2024 William Mitchell. all rights reserved.

{kind=link}

{kind=link}