A phalanx of mainstream economists such as the media and banks, who enjoy a vested interest in Japan’s interest rate hikes for various reasons, constantly predict that the Bank of Japan will succumb to “market pressure” and reverse the current situation. The monetary policy stance is in line with most central banks. While the concept of “market stress” is seen as some kind of economic process – inextricably linked to the fundamentals governing supply and demand of resources – in this case it is really just a gambling stance taken by speculators hoping that the central bank will Maybe they’ll soften up and return their bet with huge profits.Last week, the Bank of Japan announced

Speculators imagined in their narrative a series of “turning points” after which the BOJ would loosen its stance.

Recently, news emerged that a change of governor would end the “accommodative” policy.

That didn’t happen.

On July 28, 2023, the central bank announced that it would change the yield curve control (YCC) policy, which once again raised concerns.

Statement issued by the bank—— More flexibility for yield curve control (YCC) – is a very nicely laid out infographic, but fails to appease or satisfy the “market”.

As background, I explain the YCC approach taken by the Bank of Japan in this blog post – Bank of Japan shows again who is in charge (September 3, 2018).

we know:

1. Once the government issues bonds in the “primary market” (via auctions), they are traded in the “secondary market” among stakeholders (investors) based on supply and demand. When demand is strong relative to supply, the bond’s price will rise above its “face value,” and vice versa, when demand is weak relative to supply.

2. If demand for government bonds falls, secondary market prices fall and yields rise.

To understand this relationship, read this blog post – Bank of Japan is in charge, not the bond market (November 21, 2016) – I offer “A Primer on Bond Yields.”

3. Any central bank has the financial power to dominate the demand for bonds of any given maturity in the secondary market and thus can set the yield.

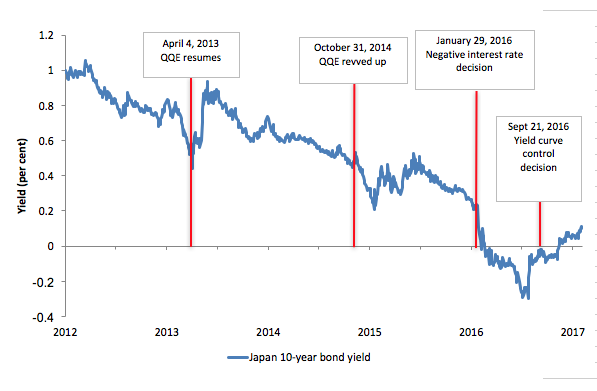

Since resuming its program on April 4, 2013, the BOJ has launched a series of so-called easing measures: Quantitative and Qualitative Monetary Easing (QQE) – This involves the central bank entering the secondary JGB market and more recently the corporate debt market, and using its endless capacity to buy what is sold in yen, including government bonds and other financial assets.

On October 31, 2014, the Bank of Japan Announce It is expanding the QQE program.

Now “money market operations will be carried out to increase the base currency at a rate of about 80 trillion yen per year (about 10-20 trillion yen more than in the past)”.

Subsequently, the bank issued a statement on January 29, 2016— Launch of “Negative Interest Rate Quantitative and Qualitative Monetary Easing” – Expanded QQE program – continued to purchase JGBs of 80 trillion yen per year and imposed a negative interest rate of -0.1% on current accounts held by financial institutions at the central bank.

I considered this decision in this blog post – Negative interest rates on bank reserves are stupid (February 1, 2016).

The explosion in yields predicted by the financial media has not materialized – the speculative commentary is as wrong as ever.

Yields are exactly following what Modern Monetary Theory (MMT) predicts — falling first and then rising as the central bank changes the size of its QQE program.

The following is the change in the 10-year Japanese government bond yield from 2010 to February 6, 2017, the announcement is divided by the red vertical line.

At the September Monetary Policy Meeting (MPM) held on September 20-21, 2016, the Bank of Japan – announcement – introduced what they called “a new framework for enhanced monetary easing: ‘Quantitative and Qualitative Monetary Easing with Yield Curve Control’ (QQE)”.

This approach became clearer when the central bank released the following information publicly— Minutes of Monetary Policy Meeting September 20-21, 2016 – November 7, 2016.

Essentially, the bank said it would use YCC to:

…control short- and long-term interest rates

It is not the market that controls interest rates – it is the central bank.

Through the YCC, it controls nominal interest rates on all parts of the yield curve as well as:

Banks will buy Japanese Government Bonds (JGB) so that the 10-year JGB yield will remain roughly at current levels (around 0%).

Speculators do not control government bond yields unless the government allows it.

Essentially, the BOJ will be involved in:

(i) Direct purchase of Japanese government bonds at the rate specified by the central bank (fixed rate purchase operation)1

(2) Fixed-rate fund supply business with a term of up to 10 years (extending the current longest business term from 1 year)

That means it will stand ready to buy unlimited amounts of Japanese government bonds at a fixed rate.

The statement outlines how the program works — Summary of direct purchase of Japanese government securities – Published November 1, 2016.

This is history.

As mentioned above, last week the Bank of Japan made changes to the YCC program.

They say there is no plan to stabilize inflation at around 2% – not referring to higher current rates, but to their view that current rates are temporary and fundamentals – wage pressures – cause inflation to Sexual factors have weakened, and interest rates will be well below 2%.

As I explained before, this is a central bank that wants higher wage growth, while most central banks are trying to push unemployment higher to further dampen (quite low) wage pressures.

However, for the BOJ, the pressure of constant wages would send the economy towards deflation and low growth, so they would maintain their monetary policy stance until stronger wage growth begins.

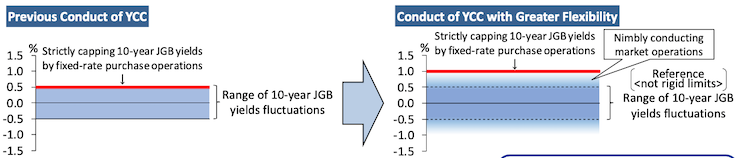

Their infographic (partially shown below) shows their now proposed shift in YCC policy.

Essentially, they have raised the cap from 0.5% to 1%, and will use their monetary power to buy bonds to ensure that yields move within a somewhat flexible range.

“Somehow” is what got speculators into trouble.

Reuters headlines (July 29, 2023) – BOJ’s opaque policy shift means yen is stronger and wilder – Sentiment captured – Opaque – What does the central bank really mean?

Washington Post article (July 28, 2023) – Bank of Japan relinquishes some control, but also throws a curveball – Claims that policy shifts represent:

…a small step toward abandoning the longstanding attachment to ultra-easy money.

But then conceded that a world of rising interest rates in Japan is “very far away, if it happens at all”.

They then call the change a “half-hearted” or “uninstructive fabrication”, as if the central bank is faltering and getting a little lost.

Incorrect.

The central bank made it clear that it will continue to “purchase unlimited daily 10-year government bonds at an interest rate of 1 percent”.

Only the ceiling has changed.

Yesterday (August 2, 2023), Bank of Japan Deputy Governor Shinichi Uchida addressed local leaders in Chiba (near Tokyo) about – Japanese Economy and Monetary Policy.

It was an interesting talk and covered a lot.

But hopes in financial markets could still be disappointed.

Clearly, the minor changes to the YCC’s plans are not seen as a shift from the central bank’s fundamental stance that has been held for years.

The Deputy Governor said (among other things):

1. “There are extremely high uncertainties in the price outlook, including the development of overseas economic activities and prices, the development of commodity prices, and the wage and price setting behavior of domestic enterprises. The assessment of the central bank is that the sustainable and stable realization of 2% The price stability target has not been achieved.”

2. “Signs of change are already being seen in firms’ wage and price-setting behavior…We are working to identify a critical inflection point where firms’ behaviors entrenched in deflationary times may change” – Chang In other words, they are looking for evidence that the deflationary mindset that is holding back wage growth is changing.

When such a change is detected, they will begin to adjust the stance of monetary policy.

3. “Strive to achieve the 2% price stability target in a sustainable and stable manner, while wages are rising.”

4. “The central bank assesses that the downside risk of missing the 2% target due to hasty adjustments in monetary easing now outweighs the upside risk of inflation continuing to exceed 2% if monetary tightening lags behind the curve” – in other words, they don’t want to pass A policy shift to deal with the current high inflation could lead to a recession and further intensify their efforts to boost wage growth.

5. “The central bank needs to patiently continue the current phase of monetary easing to support the Japanese economy so that wages continue to rise steadily next year” – they will be oriented towards wage growth as they believe it is essential to ensure stable inflation around 2% Important The risk now is that once the disruptions from COVID-19 and the Ukraine outbreak subside, inflation will remain well below inflation.

Referring to the YCC specifically, the vice-governor said “there is a long way to go before such a decision is made,” referring to those who believe it’s time to raise rates.

He also reiterated that the trigger for a major policy shift would be wage conditions, not a temporary rise in inflation.

However, the BOJ also wants to “smooth” the yield curve, which means they want a stable relationship (within a certain range) between corporate bond and JGB returns.

They argue that sticking to a tight plus-minus 0.25% band for JGBs (as YCC policy maintained until its last revision in December 2022) means that “yield spreads between corporate bonds and JGBs are unnaturally Expansion”, thus undermining the desired effect of monetary easing on business”.

In other words, corporate borrowing rates are rising due to “extremely high uncertainty about economic and price developments at home and abroad,” while low yields on JGBs are becoming an anomaly.

But the changes are small.

The December shift “raised the bond market’s expectation that if something goes wrong, the central bank will eventually respond”.

However, the deputy governor made it clear that despite the uncertainty, “more flexibility in yield curve control” is needed:

Needless to say, we are not considering an exit from monetary easing.

in conclusion

So there is nothing to suggest a return to the stance taken by other central banks.

The BOJ is firmly committed to providing “expansionary” conditions to encourage wage growth, which they see as crucial to supporting its target of stable inflation of 2%.

All the noise around that goal, caused by pandemics and the like, is just noise.

It is a pity that other central bankers have not followed suit.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}