In May 2023, the British Office for National Statistics (ONS) released national accounts data (preliminary estimates) for the March quarter. The data showed that real GDP grew by only 0.1% in the first quarter, the same as in December – in the fourth quarter of 2022, critics have Move out. Brexit this. Brexit. Charts created show Britain’s economic growth is the worst among the G7. Brexit this. Brexit. Labor frantically continues its purge of progressive elements within the party. Then, a second estimate was released on June 30, 2023, using additional data that the ONS said “provided a more accurate picture of economic growth than the first estimate” and we learned that GDP “first Quarterly growth was an unrevised 0.1%.” Brexit this. Brexit. William Keegan, like a legalistic broken record, has written more articles in the Guardian lamenting the democratic option of leaving the EU. The problem is that all this data-centric reasoning is based on illusions, which is why one must always be cautious when dealing with such data. The latest national accounts data released by the Office for National Statistics on Friday (29 September 2023) revised the first quarter result to 0.3% (a threefold increase), which is still slow but far from what experts claim disaster.

ONS latest data— UK Quarterly National Accounts GDP: April to June 2023 – tell us:

1. “UK gross domestic product (GDP) is expected to grow by an unrevised 0.2% in the second quarter of 2023.”

2. “UK GDP is currently estimated to grow by 0.3% in the first quarter of 2023 (January to March), which is higher than the previous forecast of 0.1%.”

3. “Growth in the latest quarter was driven by a 1.2% increase in the production sector, with 9 of 13 subsectors recording growth.”

4. “The household savings rate increased by 9.1% in the latest quarter, up from 7.9% in the first quarter of 2023, with income (driven by increased social benefits and higher wages and salaries) growing faster than spending.”

5. “Real household disposable income (RHDI) increased by 1.2% in the second quarter of 2023 (April-June), compared with no change in the previous quarter.”

6. “UK GDP is now estimated to grow by 4.3% in 2022, a revision from the original estimate of 4.1%.”

7. “GDP in the second quarter of 2023 (April-June) is currently estimated to be 1.8% above pre-coronavirus (COVID-19) pandemic levels.”

The ONS said the significant revision to first-quarter results was partly due to “improvements in source data and additional updates”.

They also noted that “the revisions were larger than normal, reflecting… the practical challenges of estimating GDP throughout… the pandemic.”

So if we put all of this together, I wouldn’t issue a disaster declaration just yet.

But we can look further.

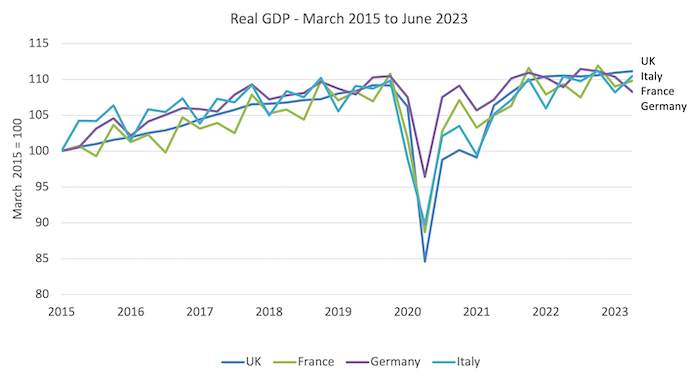

The chart below shows the situation in the UK, France, Germany and Italy since the third quarter of 2015 (thus covering the entire period after the 2016 referendum and some).

Obviously, the UK has been hit harder by the epidemic, but in terms of growth, the current recovery is better than the three largest economies in the EU.

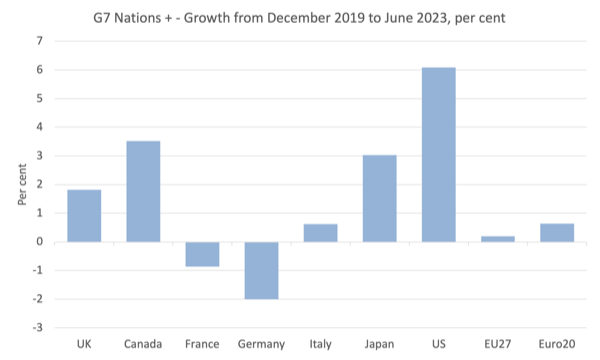

We can see this from another perspective – the chart below shows the G7 countries (UK, Canada, France, Germany, Italy, Japan, US, with the EU as enumerated members). I also include euro area aggregates.

Whatever you want to say – claims earlier this year that the UK was at the bottom of the G7 in terms of economic growth and recovery since the pandemic began – based on preliminary national accounts data, were wrong.

Compared to the major European economies, the UK looks fine.

I know that economic growth is not necessarily the best way to achieve economic performance.

But the purpose here is not to debate the best measures of social and environmental well-being.

Rather, I am interested in satisfying the claims made by those who still believe that the EU is an ideal organization.

Furthermore, as usual we are talking about aggregates here, and I know that on a micro level where humans live and work, the decision to leave the EU will be disturbing and inconvenient for some Britons.

Structural shifts of this magnitude always create winners and losers.

But again, my goal is to address a broad range of claims, not to try to pretend that large-scale structural changes won’t cause harm to some people.

On the macro level of Brexit, if being part of the EU is a benefit due to reasons such as being close to trade routes, and recognizing that much of the trade of European countries is within the EU rather than outside it, then it is expected that at this stage Europe’s larger economies will perform better than the UK.

But that is not the case, with Europe’s trading powerhouse Germany performing the worst of the three major economies.

Even so, despite the poor performance of major European economies, the Guardian’s Keegan and others still believe that the EU is a trading paradise for the UK.

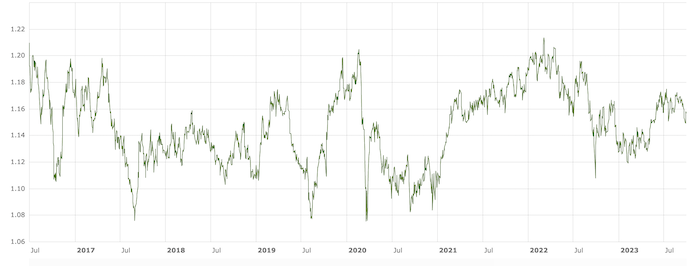

He also frequently claims that the pound has depreciated significantly against the euro.

He wrote on June 25, 2023: “The sharp fall in the pound following the referendum has led to higher prices for all imports, especially food from the EU” (source).

This is his typical claim.

How we view exchange rate movements depends on what we mean by dramatic and when we choose to measure it.

This is the GBP/EUR exchange rate since 1 July 2016 (shortly after the referendum).

No dramatic and irreversible devaluation occurred there.

Some changes but keep coming back to the original level.

Take a closer look at the modified data

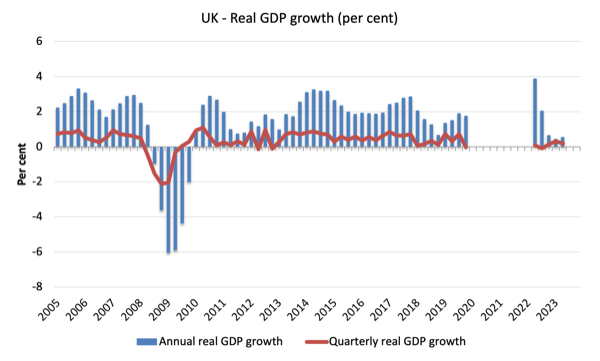

The chart below shows annual and quarterly growth from the March 2005 quarter to the June 2023 quarter.

I exclude the period of the pandemic (March 2020 quarter to March 2022 quarter) because it skews the rest of the data.

Obviously, despite what I wrote above, growth in the last three quarters has been very low.

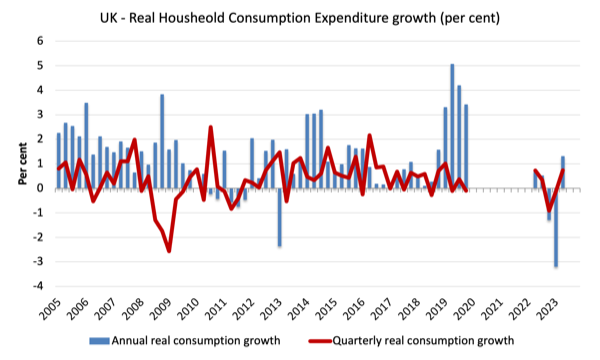

The chart below shows annual and quarterly growth in household consumption expenditure (in real terms) since the third quarter of 2005.

The rebound in the June quarter also coincided with an increase in government spending.

Tourism spending drives household consumer spending.

I think this is another interesting statistic as the anti-Brexit crowd complains about border changes creating a huge barrier to travel.

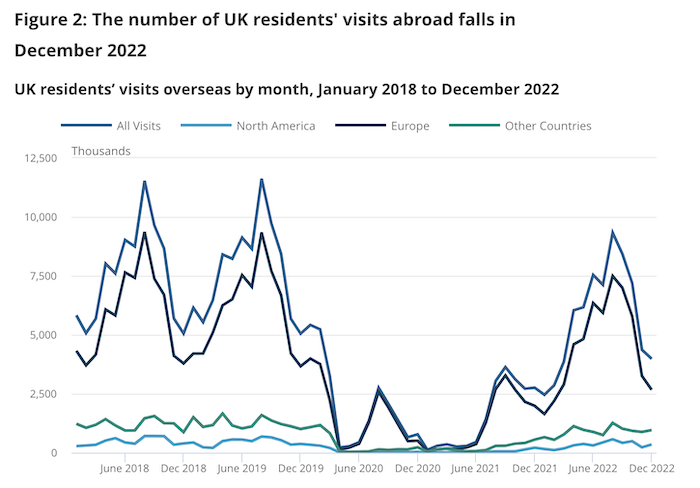

The latest outbound travel data was released on July 20, 2023— Overseas travel and tourism: provisional results for December 2022.

This is the Office for National Statistics (ONS) chart of UK residents traveling abroad.

It’s hard to see any impact other than the pandemic happening here and rising interest rates squeezing purchasing power.

One might interpret the pre-pandemic decline as Brexit disruption, and it may well have occurred while adjustments were being made.

But you also have to explain the post-pandemic boom in a strange way.

in conclusion

Overall, I still don’t see a significant macroeconomic impact from Brexit.

Remainers now insist on the difference in inflation between Britain and Europe as evidence.

I’ll write more about that another day.

That’s enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}