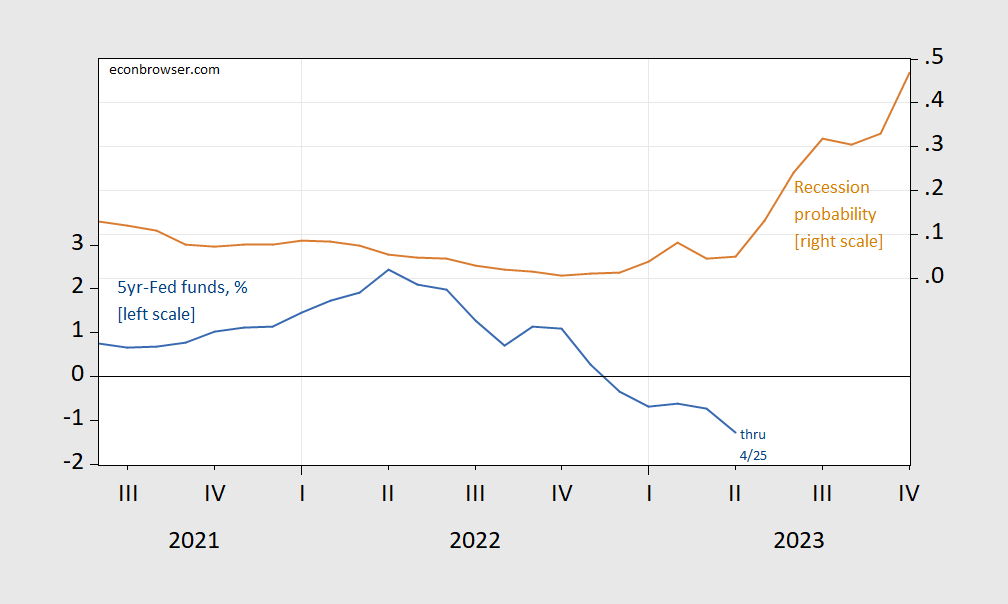

I was asked about my guess on the start of the recession. I said the consensus is the second or third quarter of this year, about 6 months away. Then I kind of wondered. According to Miller (2019), the highest AUROC over 6 months is the 5-year fed funds spread. What does this spread say?

figure 1: Five-year Treasury-Federal Funds spread, % (blue, left scale), and estimated probability of a recession in the next 6 months (tan, right scale). Source: Federal Reserve via FRED, and authors’ calculations.

Therefore, for October 2023, using a probabilistic model (pseudo-R2 = 0.16).

What about the next few months, including Q1 and Q2? Q1 advances will be released tomorrow; as of today, Q1 GDPNow is 1.1% q/q SAAR. S&P Global Market Insights (formerly Macroeconomic Advisors) is tracking 1% and 0% in Q1 and Q2 as of today. Of course, as already discussed in depth, NBER does not date business cycles based solely on GDP (China Eastern Airlines (2022); Frankel (2022); CBO Discussion (2022); postal).

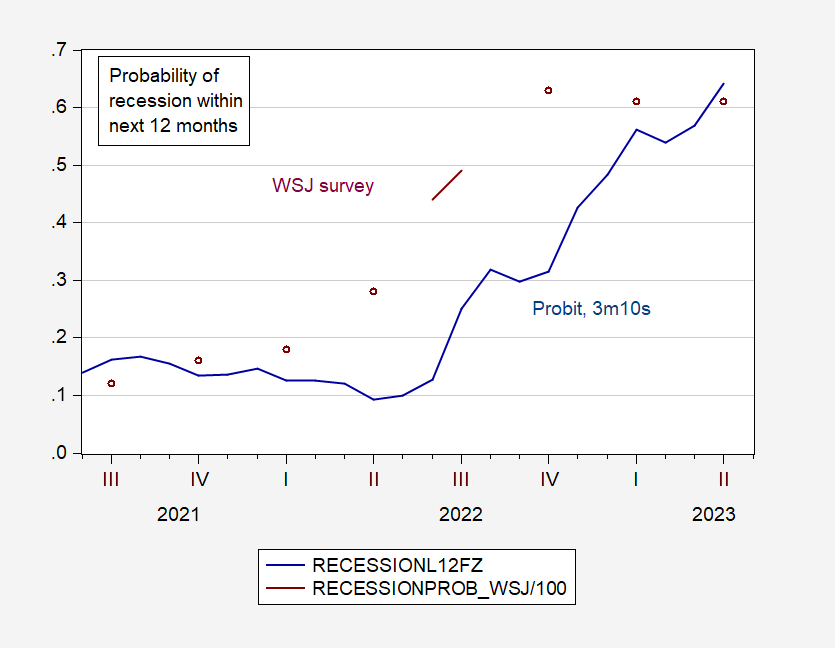

The most recent (April) survey by the Wall Street Journal shows the likelihood of a recession within 61% over the next 12 months, not too far from what the ordinary probability of the 3-month 10-year term spread would suggest.

figure 2: Estimates of the probability of a recession within the next 12 months based on the 10-year to 3-month spread (blue) and the median of the Wall Street Journal survey. Source: WSJ survey, author’s calculations.

{kind=link}

{kind=link}