Following the release of employment and monthly GDP (IHS Markit):

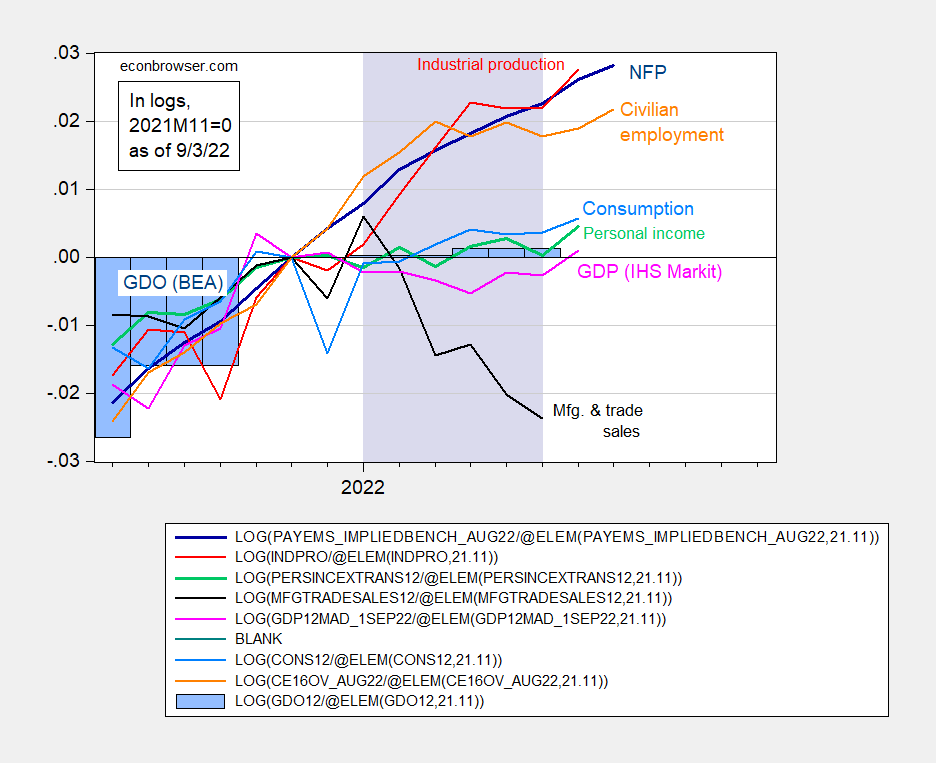

The traditional case in terms of GDP (BEA), normalized to 2021M11:

figure 1: Nonfarm employment (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in mid-2012 (green), manufacturing and trade sales in mid-2012 (black), consumption $2012 ( Light blue), January 2012 monthly GDP (pink), official GDP (blue bars), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

Another case, using the implicit benchmark NFP and GDO:

figure 2: Nonfarm employment (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in mid-2012 (green), manufacturing and trade sales in mid-2012 (black), consumption $2012 ( Light blue) and 2012 monthly GDP (pink), official GDP (blue bars), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

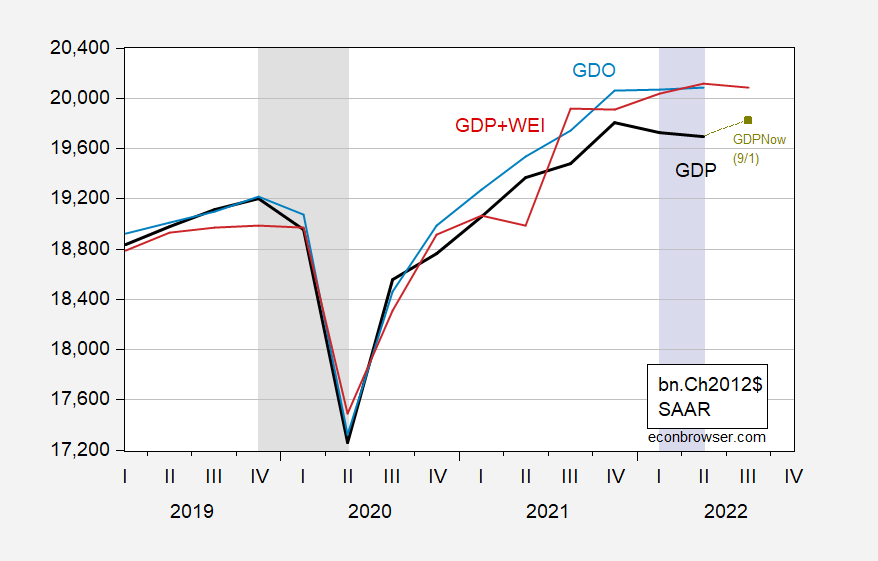

Since we have additional data on Q3, I thought it would be interesting to see what the quarterly numbers mean:

image 3: GDP (bold black), GDPNow implied levels as of September 1 (yellow-green squares), GDO (light blue), and Weekly Economic Index (WEI) implied GDP (red) for GDP one year ago ). The third quarter of implied GDP uses WEI to 8/27. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA (Second Edition), New York Fed through FRED (as of September 3), Atlanta Fed (as of September 1), NBER and author’s calculations.

Note that the implied GDP level of the Lewis-Mertens-Stock weekly economic index applied to real GDP a year ago is very close to the GDO for this and previous quarters.

{kind=link}

{kind=link}