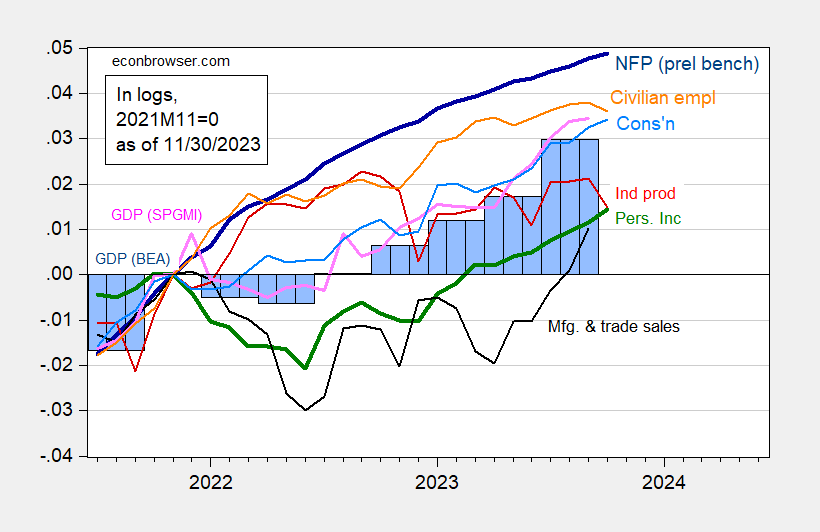

On the last day of the month, we see consensus on monthly personal income and consumption data. Below is a picture of the key indicators followed by the NBER BCDC (of which personal income transfers and employment are key) as well as the SPGMI’s monthly GDP.

figure 1: Nonfarm employment includes preliminary baseline (bold dark blue), civilian employment (orange), industrial production (red), 2017 personal income excluding transfers (bold green), 2017 manufacturing and trade sales $ ( black), consumption $ in Ch.2017 (light blue), monthly GDP $ in Ch.2017 (pink), second release of GDP (blue bar), all logarithms normalized to 2021M11 = 0. Source: BLS via FRED, U.S. Bureau of Labor Statistics preliminary benchmarksFederal Reserve, BEA 2023Q3 2nd Edition, contains comprehensive revisions, S&P Global/IHS Markit (Nigerian macroeconomic consultant, IHS Markit) (11/1/2023 release) and the author’s calculations.

The latest signs are that inflation-adjusted personal income (excluding current transfers) and consumer spending continue to grow. When earnings and nonfarm employment trends are considered together (even taking into account preliminary revisions to employment benchmarks), it’s difficult to see the severity of the recession as of October.

The GDPNow quarter-to-quarter seasonally adjusted rate (SAAR) as of today is 1.8%. Tomorrow we should take a look at monthly GDP.

Note that the picture will look slightly different when using GDO.

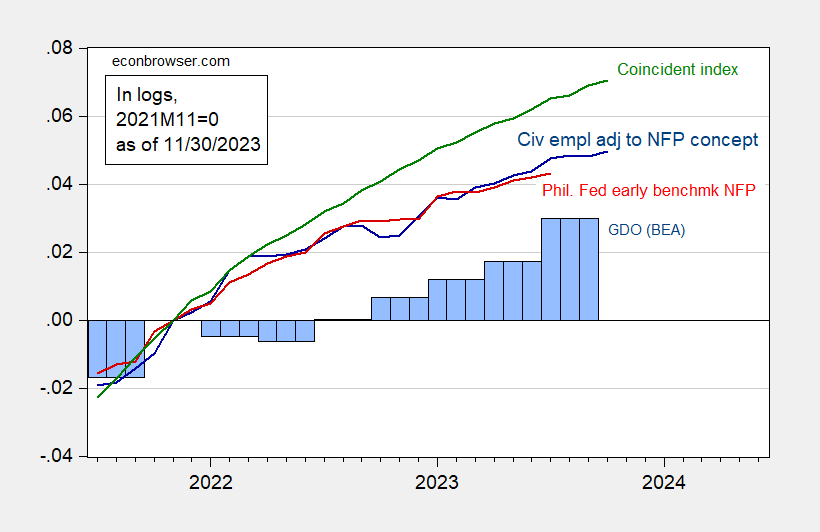

figure 2: CPS civilian employment adjusted for NFP concepts (dark blue), the Philadelphia Fed NFP early benchmark measure (red), the U.S. Philadelphia Fed Concurrent Index (green), and 2017 $1 billion GDO (blue bar), All logarithms are normalized to 2021M11=0.Source: Bureau of Labor Statistics, Federal Reserve Bank of Philadelphia [1], [2]BEA 2023 Season 3 Edition 2, and the author’s calculations.

although GDO growth rate is lower than GDP growth rate (3.3% vs. 5.2%, quarter-on-quarter seasonally adjusted rate), according to the latest observations, all indicators (preservation of industrial production) continue to rise.

{kind=link}

{kind=link}