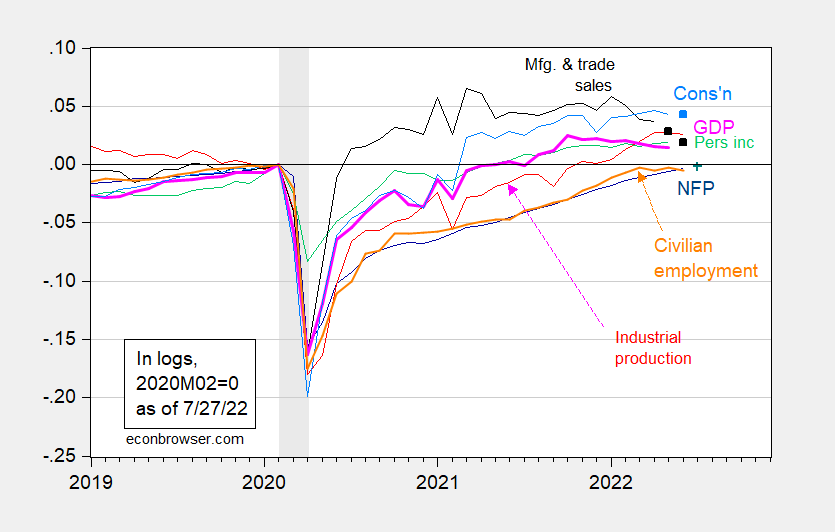

Below are some of the key metrics followed by the NBER Business Cycle Dating Committee. I have added civilian employment to a set of indicators. Here are the recession and recovery trends so far, with some speculation on June consumption, May and June sales (as data is released 7/29), and July employment (8/5).

figure 1: Nonfarm payrolls (dark blue), Bloomberg consensus (blue+) as of July 27 Industrial production (red), mid-2012 personal income excluding transfers (green), manufacturing and trade sales mid-2012 (black), projected sales based on retail sales (black squares), consumption in 2012 dollars (light blue), projected consumption based on retail and food sales (light blue squares), and monthly GDP in 2012 dollars (pink), all logs normalized to 2020M02=0. NBER defines the decay date, peak to trough, shades of gray. Sources: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published July 1, 2022), NBER, and author’s calculations.

Since we only have manufacturing and trade sales through April, and consumption through May, I’ve projected these based on a log-first difference regression after 2021M04. Adjusted R2 was 72% for consumption and 43% for sales.

Manufacturing and trade sales continued to decline, as expected, as consumption shifted from goods to services. Consumption was basically stable, with an annual growth rate of 0.6%. The Bloomberg Consensus for NFP points to +255 K, so the labor market continues to recover.

{kind=link}

{kind=link}