Industrial production was lower than expected (-0.1% vs. Bloomberg +0.3% m/m). Below are some of the key metrics the NBER BCDC follows.

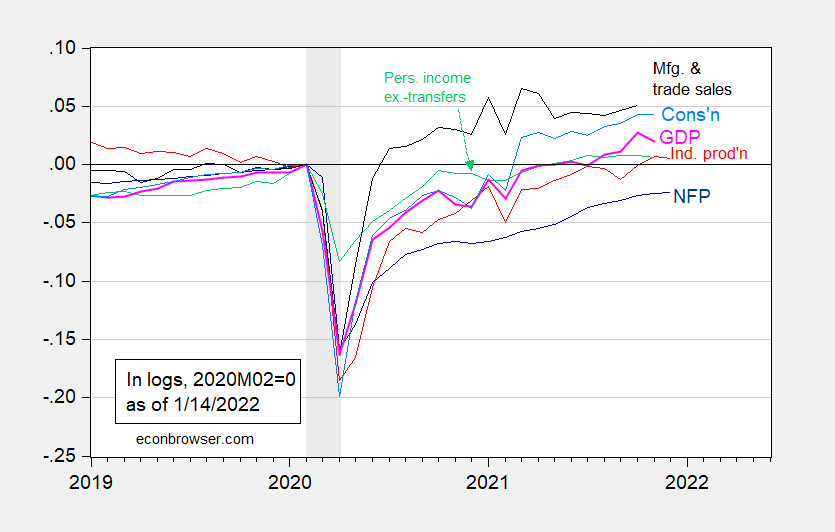

figure 1: Nonfarm employment (dark blue), industrial production (red), 2012 personal income excluding transfers (green), 2012 manufacturing and trade sales (black), 2012 consumption (light blue), and 2012 Monthly GDP (pink) for January of the year, all log normalized to 2020M02=0. NBER defines recession dates, peaks and valleys, shades of gray. Sources: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published January 3, 2022), NBER, and author’s calculations.

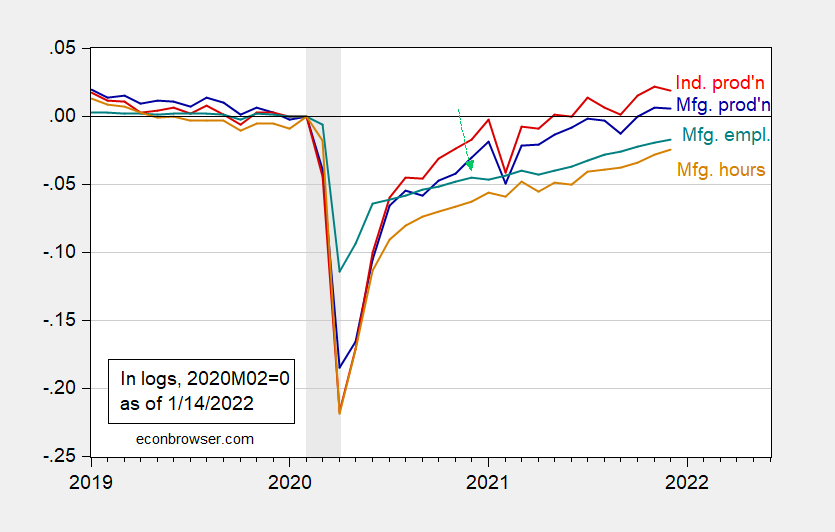

Manufacturing production also missed out (-0.3% vs. +0.5% consensus).

figure 2: Industrial production (red), manufacturing production (blue), manufacturing employment (green), total manufacturing hours for production and unsupervised workers (brown), all seasonally adjusted, all log 2020M02=0. NBER defines recession dates, peaks and valleys, shades of gray. Source: Federal Reserve Board calculations from FRED, BLS, NBER and authors.

The volatile utilities segment of IP declined 1.5% sequentially, partially offsetting a 2% increase in mining.

On the manufacturing side, the business equipment category fell 0.5%, which is sensitive to capital investment spending and could signal a slowdown (probably, since we don’t know if it’s caused by supply and demand). Auto parts production fell 1.3% month-on-month.

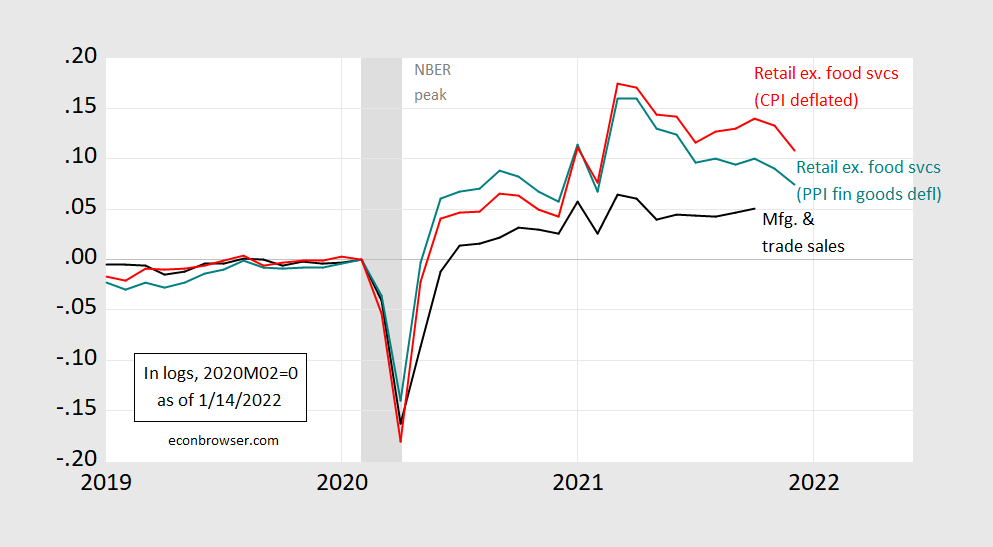

Finally, nominal retail sales (excluding food services) were also below expectations, at -2.3% and +0.2%, respectively. The actual situation:

Figure 3: Manufacturing and trade industry sales, 2012 Ch.$ (black), retail sales excluding food services due to decline in CPI (red), retail sales excluding food services due to decline in PPI for manufactured goods (turquoise), Both are represented by logarithm 2020M02=0. NBER defines recession dates, peaks and valleys, shades of gray. Source: Federal Reserve Board through FRED, Census, BLS, NBER, and author’s calculations.

Jason Furman The observed decline in actual sales toward trend could be seen as a signal of normalization as spending on merchandise returns to pre-pandemic levels. Looking at business cycle indicators, if manufacturing and trade sales correlate with retail sales, this implies a downward movement of the black line in Figure 1. (For every 1 percentage point change in PPI since July 2020, a contraction in retail sales is associated with a 0.5 percentage point change in real manufacturing and trade industry sales, adj.R squared at 0.75).

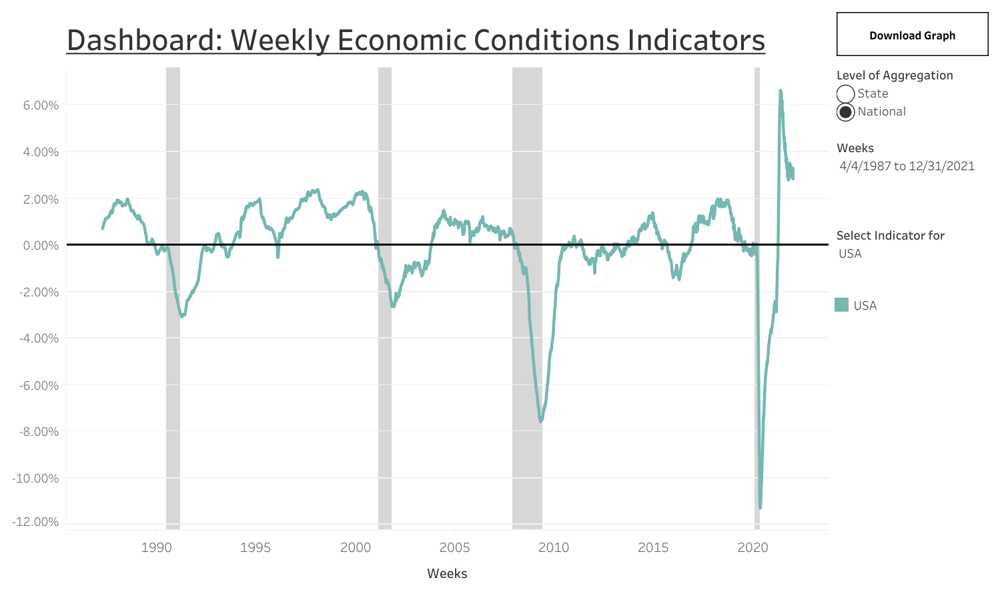

These are backward looking indicators. High-frequency indicators based on weekly data (Baumeister et al. index, see this postal,and this postal) showed continued growth through December.

source: Weekly Economic Conditions Index, accessed 14 January 2022.

Similar patterns are shown in Lewis-Mertens-Stock indicator.

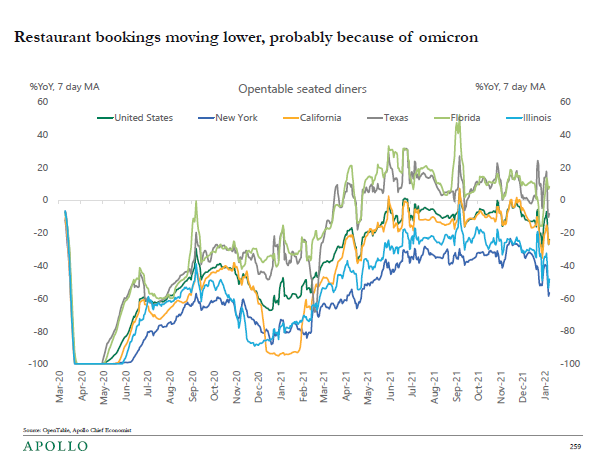

On the other hand, indicators for the high-touch services sector suggest a downturn there.

source: Torsten Slok/Apollo, Newsletter January 14, 2022.

{kind=link}

{kind=link}