The monthly GDP for November is out. Q4 tracked as q/q growth of 2.1%-3.9% (SAAR).

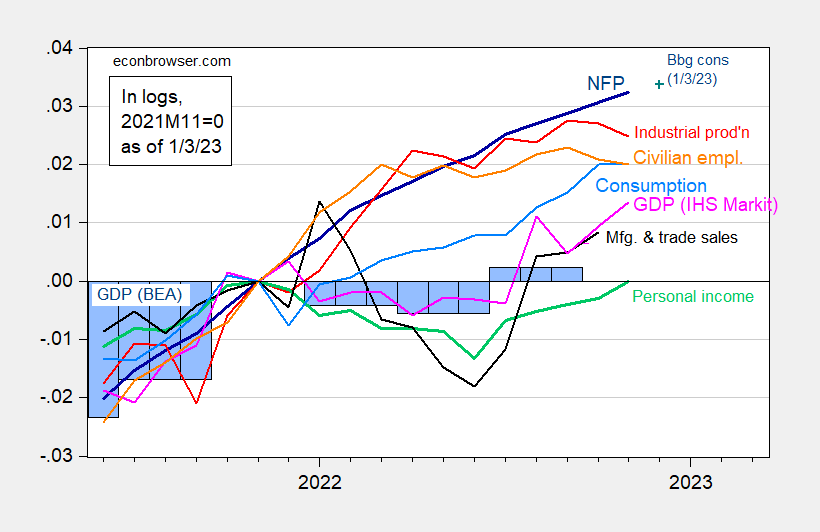

figure 1: 2012 Nonfarm Payrolls, NFP (Dark Blue), Bloomberg Consensus (Blue+), Private Employment (Orange), Industrial Production (Red), Personal Income Excluding Transfers (Green), 2012 Manufacturing and Trade Sales $ (black), Consumption $ for Ch.2012 (light blue) and Monthly GDP $ for Ch.2012 (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 3 January 2023), and authors’ calculations.

IHS-Markit monthly GDP continues to rebound sharply. Today from IHS Markit:

SAAR monthly GDP rose 0.4% in November after rising 0.5% in October (up 0.2 percentage points). The sharp rise in net exports outpaced November’s growth. Final domestic sales fell in November, largely reflecting a decline in residential and nonresidential fixed investment. Taking the average of October and November, monthly GDP was 3.0% above the annual average in the third quarter. Our latest estimate for Q4 GDP growth of 2.6% annualized implies a decline of 0.5% (non-annualized) in December.

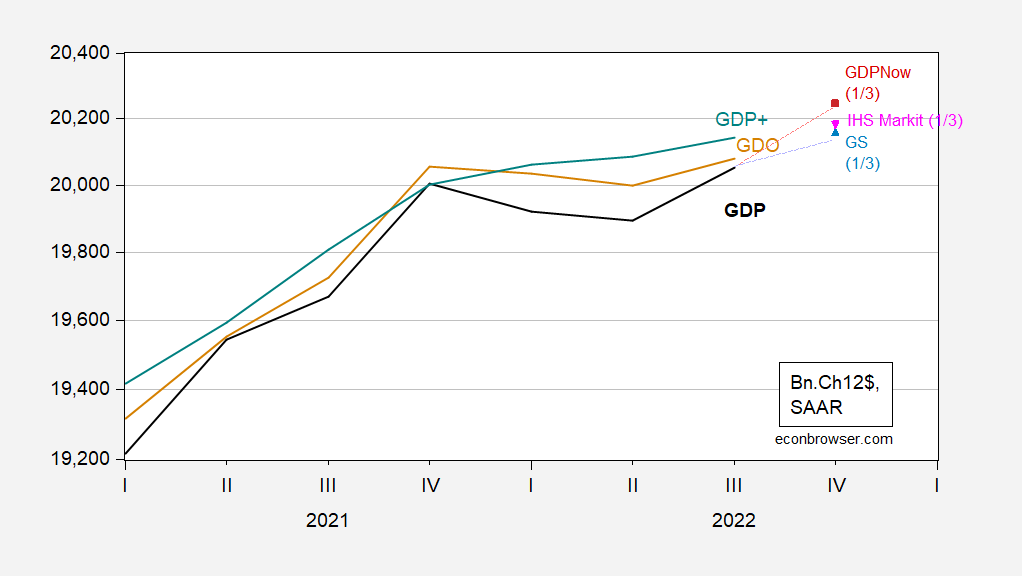

Revised nowcast and track estimates today. GDPNow for Q4 is 3.9% q/q SAAR.

figure 2: GDP (black bold), GDO (tan), GDP+ (green), Q4 GDPNow (red squares), Goldman Sachs (sky blue triangles), IHS Markit (inverted pink triangles), all in billions of Ch. 2012$, SAAR. GDP+ level calculated by iterating 2019Q4 GDP (when GDP and GDO are matched). Lavender shading represents the peak and trough of a hypothetical recession in the first half of 2022. Source: BEA (3rd Edition Q4), Federal Reserve Bank of Philadelphia (12/22), Federal Reserve Bank of Atlanta (1/3), Goldman Sachs (1/3), IHS Markit (1/3), and author’s calculations.

Note that while GDP is down in 1H22, GDO is essentially flat, while GDP+ is rising.

Outlook summary for financial firms, via Bloomberg here.

{kind=link}

{kind=link}