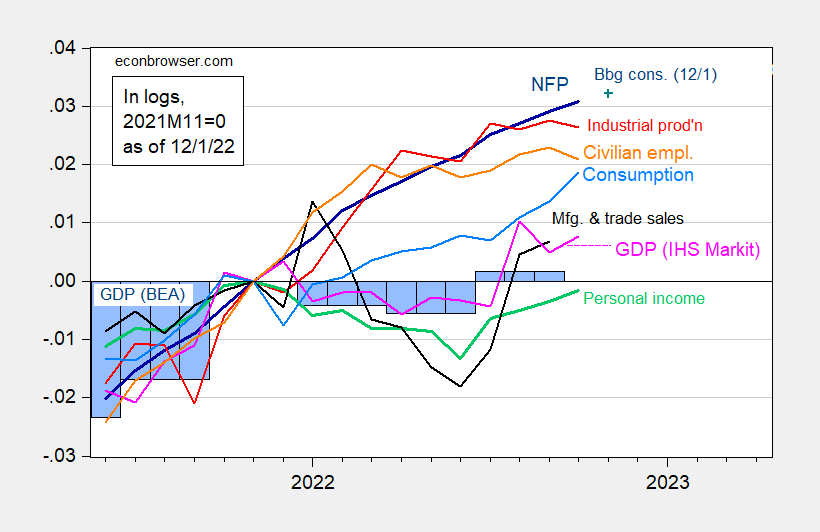

With the release of personal consumption and income for October, we have the following key series of pictures following NBER BCDC (and IHS Markit’s monthly GDP, previously from Macroeconomic Advisers).

figure 1: Nonfarm payrolls, NFP (dark blue), Bloomberg consensus as of Dec. 1 (blue+), civilian employment (orange), industrial production (red), personal income excluding 2012 Chinese transfers (green) , Sales for Manufacturing and Trade Ch.2012 (black), Consumption for Ch.2012 (light blue) and Monthly GDP for Ch.2012 (pink), GDP (blue bars), all log normalized to 2021M11= 0. Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 12/1/2022), and authors’ calculations.

Personal income excluding current transfers and consumption continued to grow. Although the third quarter GDP SAAR was revised up by 0.3 percentage points, IHS Markit monthly GDP October also rose:

Monthly GDP rose 0.3% in October after falling 0.5% in September. The latter was revised down by 0.4 percentage points. The increase in monthly GDP in October outpaced a strong increase in real personal consumption expenditures. Elsewhere, non-residential fixed investment, non-farm inventory investment and others all recorded gains in October, while residential investment and net exports recorded declines.

As of today, GDPNow is Q4 2.8% q/q SAAR. A recession in the first half of 2022 seems (still) unlikely to me given the likely revision of GDP and the evolution of GDO.However, a recession in 2023 seems likely yield curve inversion and other predictors.

{kind=link}

{kind=link}