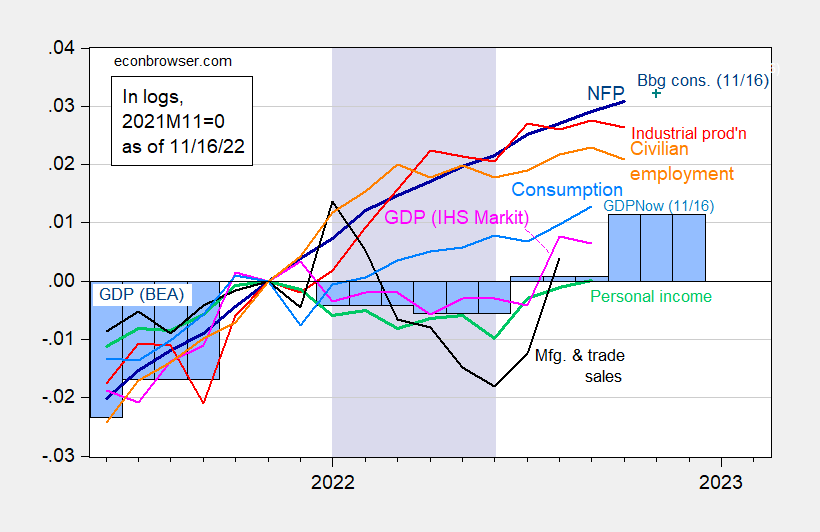

Industrial production fell 0.1% on the month, compared to +0.2 expected by Bloomberg. Non-farm payrolls rose strongly in October. Other key metrics followed by the NBER Business Cycle Dating Committee.

figure 1: Non-farm payrolls, NFP (dark blue), Bloomberg consensus as of Nov 16, 2016 (blue+), private employment (orange), industrial production (red), personal income excluding 2012 Chinese transfers ( Green), Manufacturing and Trade Ch.2012 Sales (black), Ch.2012 Consumption (light blue) and Ch.2012 Monthly GDP (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 GDP from GDPNow on 11/16. Lavender shading indicates a hypothetical recession in the first half of 2022. Sources: BLS, Fed, BEA, calculations from FRED, IHS Markit (formerly Macroeconomic Advisor) (published 1 Nov 2022), GDPNow (11/16) and authors.

While industrial production fell, with manufacturing production rising just 0.1% versus the consensus estimate of 0.2%, retail sales far outpaced forecasts.

As of today, GDPNow is at 4.382% q/q SAAR in Q4. A recession in the first half of 2022 seems (still) unlikely to me given the likely revision of GDP and the evolution of GDO. However, given the inverted yield curve and other forecast factors, a recession is likely in 2023.

{kind=link}

{kind=link}