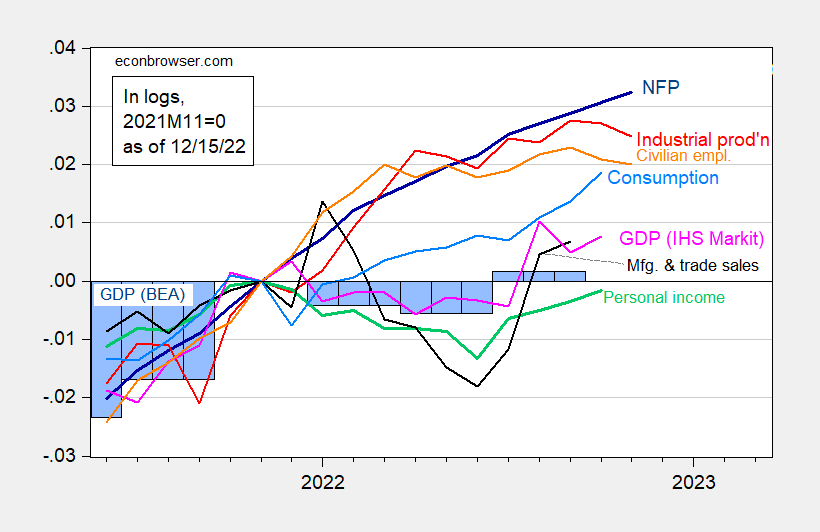

Both industrial and manufacturing production unexpectedly fell in November – -0.2% and -0.1% vs +0.1% and -0.1% m/m (Bloomberg). Here is a graph of the results of some of the key variables followed by the NBER Business Cycle Dating Committee.

figure 1: Non-farm payrolls, NFP (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in China 2012 (green), manufacturing and trade sales in China 2012 (black), Monthly GDP in Consumption Ch.2012$ (light blue) and Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 12/1/2022), and authors’ calculations.

Retail sales (not in the above table) also fell -0.6% m/m, below the Bloomberg consensus of -0.1% m/m.

Q4 GDPNow cuts to 3.2% from 3.4% q/q SAAR (12/9), IHS-Markit/S&P Global to 3.3% from 3.6% (12/9), while GS was unchanged at 1.7%.

{kind=link}

{kind=link}