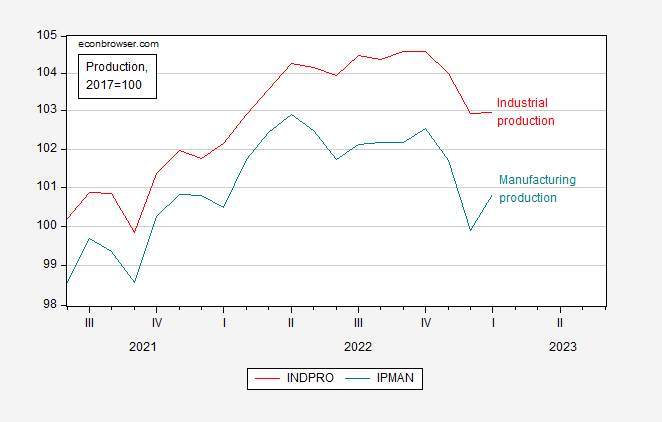

Industrial output was in line, while manufacturing output and retail sales topped expectations. As far as the analysis of the economic situation is concerned, industrial production is more concerned by the NBER Business Cycle Timing Committee.

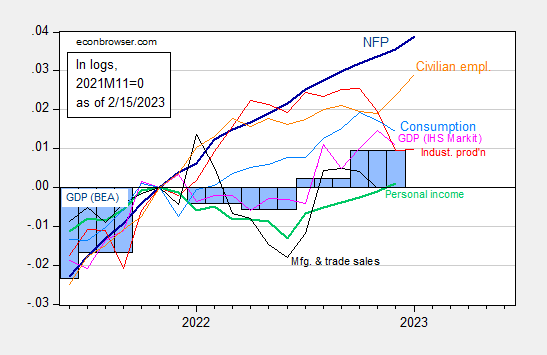

figure 1: Non-farm payrolls, NFP (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in China 2012 (green), manufacturing and trade sales in China 2012 (black), Monthly GDP in Consumption Ch.2012$ (light blue) and Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 1 February 2023) and authors’ calculations.

Manufacturing production, which is not directly affected by weather conditions (ie warmer than expected), rebounded 1% m/m, above the consensus estimate of 0.8%.

figure 2: Industrial production (red) and manufacturing production (teal), both 100 in 2017. Source: Federal Reserve Board via FRED.

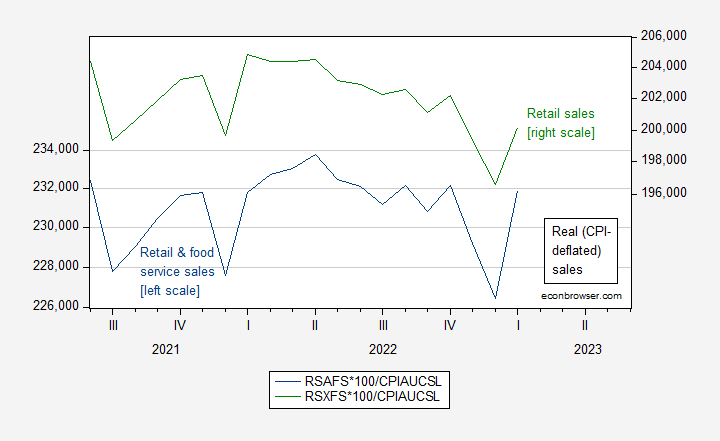

Finally, retail and food service sales – giving us some insight into consumption, were also above consensus (3.0% vs. 1.8% consensus).

image 3: Retail and food service sales (blue, left axis) and retail sales (green, right axis), 1982-84 $m/month (CPI deflator). Source: Population census via FRED, BLS, and author’s calculations.

The increase in retail sales suggests that consumption remains strong.

{kind=link}

{kind=link}