New Deal Democrats Proposed normalization on 2023M01. That’s the NBER BCDC indicator, plus monthly GDP, and a bunch of other indicators since then.

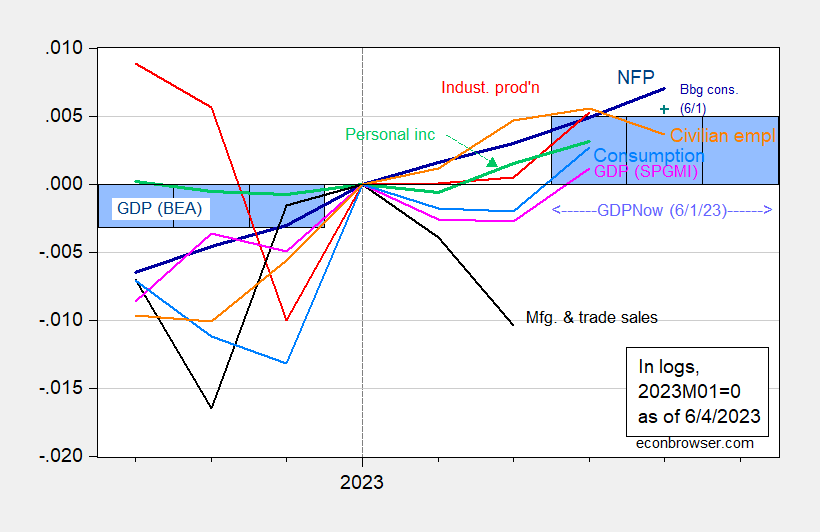

figure 1: Nonfarm payrolls, NFP (dark blue), Bloomberg 6/1 consensus (blue+), civilian employment (orange), industrial production (red), personal income excluding 2012 China transfers (green), manufacturing and Trade Sales Ch.2012 USD (black), Ch.2012 USD Consumption (light blue), Ch.2012 USD Monthly GDP (pink), GDP (blue bars), 2023Q1 is 6/1 of GDPNow, all Log normalized to 2023M01=0. The Bloomberg consensus level is calculated by adding the forecast change to the previously unrevised level of available employment at the time of the forecast. Source: US Bureau of Labor Statistics, Federal Reserve, BEA 2023Q1 Second Edition via FRED, Federal Reserve Bank of Atlanta, S&P Global/IHS Markit (nee Macroeconomic Consultant, IHS Markit) (6/1/2023 release) and the authors’ calculations.

As noted by the Democratic New Deal, NFP and personal income have not grown as sharply as they normalized to 2022M01. However, they are still rising (civilian employment in the CPS series fell in May, but as noted elsewhere, this series should not be taken too seriously given its volatility). Note that GDPNow as of June 1 (thus using 2/3 of Q2 data) is positive at 2% q/q SAAR.

and alternative series.

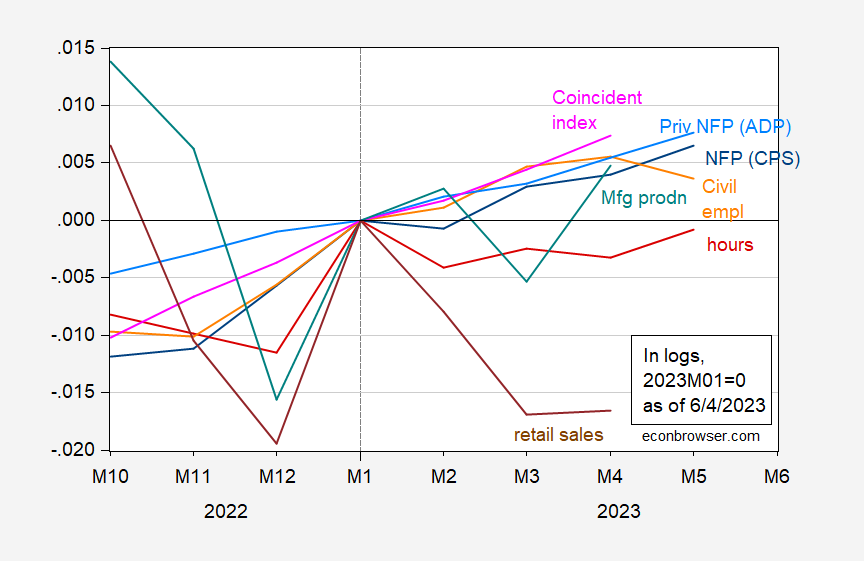

figure 2: Civilian employment adjusted for the concept of nonfarm employment (dark blue), ADP’s private nonfarm employment (sky blue), civilian employment (orange), total weekly hours worked by production and non-supervisory workers (red), manufacturing production ( teal), Concordance Index (teal), retail sales ex food services deflated by CPI (brown), all log normalized to 2023M01=0. The Bloomberg consensus level is calculated by adding the forecast change to the previously unrevised level of available employment at the time of the forecast.Source: U.S. Bureau of Labor Statistics, Federal Reserve and Philadelphia Fed via FRED and author’s calculations.

Total hours did drop slightly. The same goes for retail sales, though the series is pretty volatile. The series has been trending down since 2022M04.

So one might be able to extrapolate the deceleration more clearly over shorter periods of time.

{kind=link}

{kind=link}