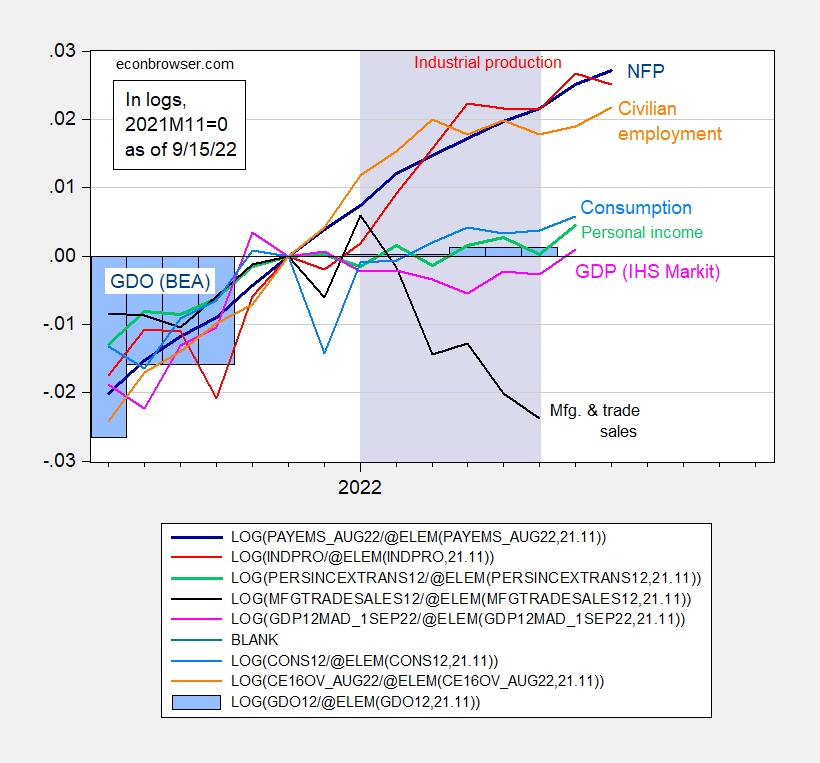

With industrial production below consensus in August (-0.2% vs. 0.1% m/m Bloomberg), we have below a picture of some of the key metrics followed by the NBER Business Cycle Dating Committee.

figure 1: Nonfarm employment (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in mid-2012 (green), manufacturing and trade sales in mid-2012 (black), consumption 2012 USD ( Light blue), January 2012 monthly GDP (pink), official GDP (blue bars), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

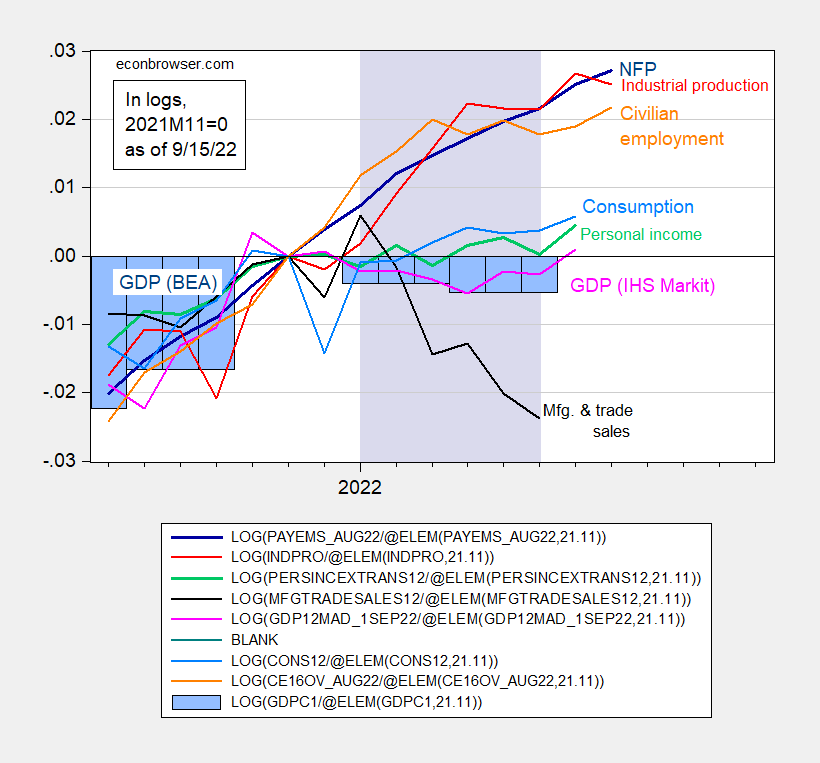

There appear to be differences in GDP and other metrics; however, if we look at GDO, they appear to be more consistent.

figure 2: Nonfarm employment (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in mid-2012 (green), manufacturing and trade sales in mid-2012 (black), consumption 2012 USD ( Light blue) and January 2012 monthly GDP (pink), GDP, GDO (blue bars), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

For more discussion on GDP vs GDO and other related indicators, see here postal from the beginning of the month.

{kind=link}

{kind=link}