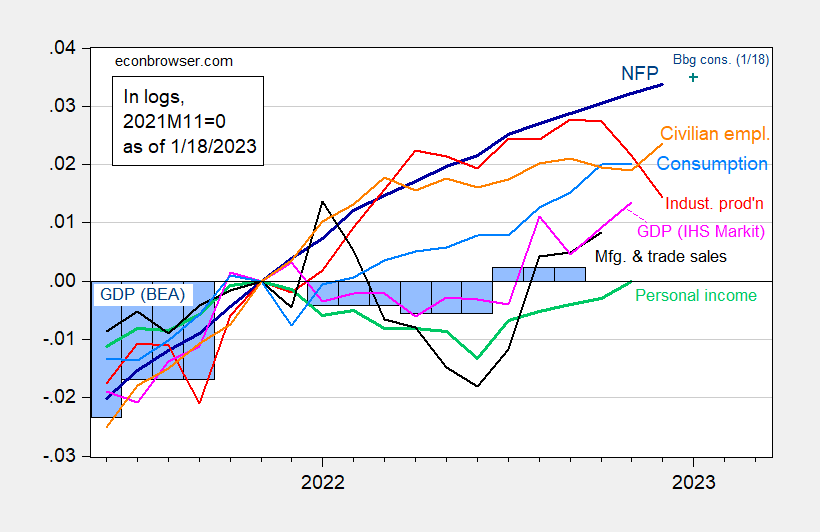

With the release of December 2022 Industrial Production (-0.7% vs. Bloomberg Consensus -0.1, m/m), we have the following picture of business cycle indicators, which include the NBER Business Cycle Date Committee as well as the IHS Markit monthly GDP:

figure 1: Non-farm payrolls, NFP (dark blue), Bloomberg consensus as of 1/18 (blue+), private employment (orange), industrial production (red), personal income excluding transfers in China in 2012 (green), Sales for Manufacturing and Trade Ch.2012 (black), Consumption for Ch.2012 (light blue) and Monthly GDP for Ch.2012 (pink), GDP (blue bars), all log normalized to 2021M11=0 . Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 3 Jan 2023), Bloomberg (as of 1/18) and author’s calculations.

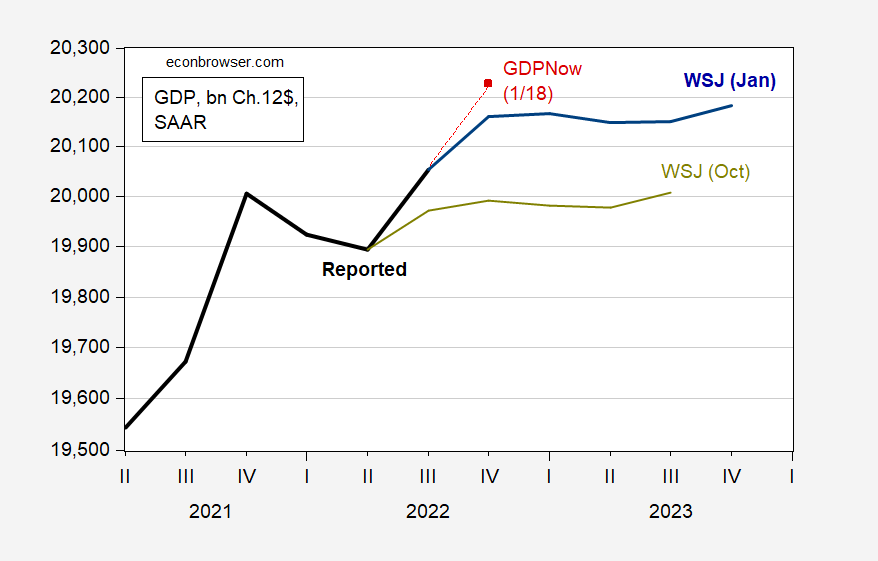

The decline in industrial production was a big negative surprise. Taking this report and other factors into account, the Atlanta Fed lowered its near-term forecast for the fourth quarter to 3.5% from 4.1% q/q SAAR.

figure 2: GDP (black), WSJ average Jan 2023 survey (blue), Oct 2022 (yellow green), GDPNow 1/18/23 (red squares). Source: BEA 2022Q3 3rd rel, Wall Street Journal (various), Federal Reserve Bank of Atlanta.

So despite the sharp drop in industrial production (remember NBER BCDC puts the main weight ahead of non-farm payrolls and personal income transfers), Atlanta Fed data still showed positive GDP growth in Q4.

{kind=link}

{kind=link}