This is an almost happy conclusion Washington Examiner article Last December.Now, their conclusion is indeed based on Report from the Legislative Analyst's Office. However, this conclusion is based on the (inappropriate) use of (national-level) Sam's rule to calculate state-level unemployment rates.and as Dr. Sahm saidthis is not the correct approach – instead one needs to check the appropriate threshold for a given state before using it to infer a recession.

Well, let's look at some metrics.

figure 1: California nonfarm payrolls (dark blue), Philadelphia Fed early benchmark measure of nonfarm payrolls (pink), civilian employment (tan), linear interpolation of real wages and salaries, deflated by national chain CPI (sky blue) Color), GDP (red), consistency index (green), all in the log 2021M11=0.Source: Bureau of Labor Statistics, Bank of East Asia, Federal Reserve Bank of Philadelphia [1], [2]and the author's calculations.

Our picture is a bit divergent – similar to the situation at the national level – with employment indicators (NFP, early benchmark NFP and concurrent index) pointing to growth through 2023, while tight wages and salaries have not recovered by the end of the year compared to November 2021 s level. However, by 2023, GDP is still growing.

Note that the Coincidence Index – which is based on nonfarm payrolls, average hours worked by manufacturing workers, the unemployment rate, and wage and salary expenditures deflated by the Consumer Price Index – significantly outperforms other indicators. For what it's worth, Federal Reserve Bank of Philadelphia state-level business cycle chronology It does not mean there will be a recession in 2023.

As for the coming recession, UCLA Anderson School Predictions (March 13) Notes:

California's economy is expected to continue to grow faster than the United States, but not by much. The risks to forecasts are the same as those to countries: political and geopolitical. On the downside, interest rates could disrupt the current economic expansion; on the upside, increased international migration and accelerated localization of technology manufacturing could be affected.

The unemployment rate in the first quarter of this year is expected to average 4.7%, and the average unemployment rate in 2024, 2025 and 2026 is expected to be 4.6%, 3.8% and 3.9% respectively. The forecast total employment growth rates in 2024, 2025 and 2026 are -0.6%, 2.1% and 1.5% respectively. Non-farm employment is expected to grow by 1.4%, 1.7% and 1.2% respectively in the past two years.

Real personal income is expected to grow by 2.0% in 2024, 2.9% in 2025, and 2.7% in 2026. recovery, followed by steady growth in new home production. We expect 123,000 net new housing units to be added in 2024, rising to 159,500 units by the end of 2026.

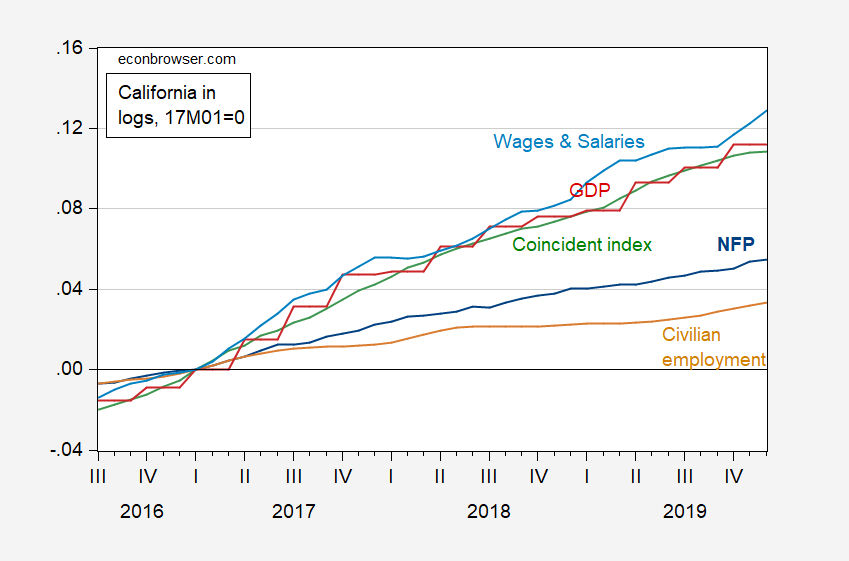

* Some readers may remember the great California recession debate of 2017 political calculation, here. The Philadelphia Fed failed to determine that California was in recession in 2017-18.

Based on the 12-month moving average of the household survey series, Ironman speculates that a recession has begun. Here are the actual results.

figure 2: California nonfarm payroll employment (dark blue), civilian employment (tan), linearly interpolated real wages and salaries, deflated by national chain CPI (sky blue), GDP (red), coincidence index (green), all Shows 2021M11=0 in logarithmic form.Sources: Bureau of Labor Statistics, U.S. Bureau of Economic Analysis, Federal Reserve Bank of Philadelphia [1]and the author's calculations.

in conclusion: Be wary of state-level household survey employment series.

{kind=link}

{kind=link}