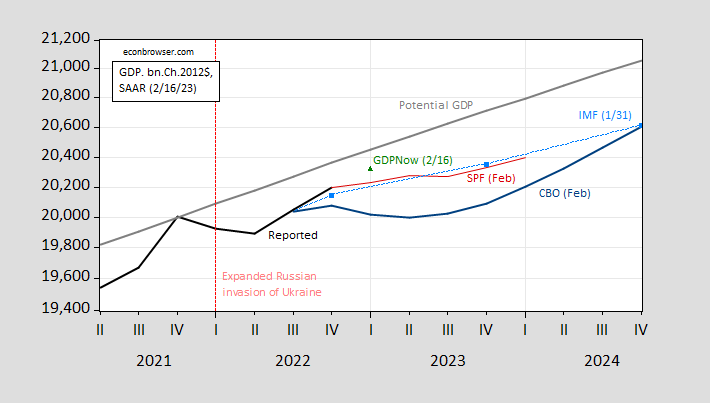

CBO released its Budget and Economic Outlook, 2023-33 yesterday. The forecast, based on data available as of January 6, shows a slight decline in GDP in the first quarter of 2023 and the second quarter of 2023.

figure 1: Reported GDP (bold black), CBO forecast (blue), SPF median forecast (red), IMF WEO forecast (sky blue), GDPNow 2/16 (green triangle), potential GDP (gray), all ten Billion Ch.2012 $ Sal. Source: BEA 2022Q4 advance release, congressional budget office, Federal Reserve Bank of Philadelphia, Federal Reserve Bank of AtlantaIMF WEO (January), and authors’ calculations.

CBO forecasts are based on data available on January 6 and therefore do not include information released in advance of the fourth quarter, nor follow-up information.

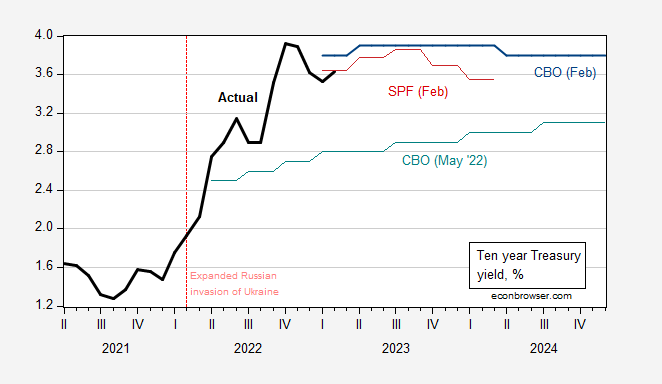

Note that interest rates are also expected to be much higher as financial markets actually develop.

figure 2: Ten-year Treasury yield (bold black), CBO February 2023 forecast (blue), CBO May 2022 forecast (teal) and SPF February median forecast (red), all in %. 2023Q1 is the first half of the quarter. Source: Treasury via FRED, congressional budget office (various), and Federal Reserve Bank of Philadelphia.

Higher interest rates – among other developments – mean slower GDP growth, so slow that it has two quarters of negative growth (albeit at -0.1% q/q in Q2, essentially zero). The implied peak of CBO’s forecast for GDP is the fourth quarter of 2022. Still, the document made no mention of a recession in 2023.

image 3: Nonfarm Payrolls – Actual (bold blue), Estimated (blue), GDP – Actual (bold pink), Estimated (pink), Actual Personal Income Less Current Transfers – Actual (bold light Green), Actual Personal Income – Projected (light green), Actual Consumption – Actual (bold sky blue), projected (sky blue), all in log, 2022Q4=0. The 2023Q1 NFP observation is for January. Source: BLS, BEA 2022Q4 Forecast, Congressional Budget Office (February)the author’s calculation.

While GDP did fall slightly, NFP was flat and consumption and personal income continued to rise.Since the NBER’s Business Cycle Dating Committee does not rely primarily on GDP (given multiple revisions to GDP), it Employment and Personal Incomeit makes sense that the recession was not predicted.

GDPNow as of today suggests that Q1 2023 GDP will be substantially higher than the CBO forecast (green triangle in Figure 1; 2.5% SAAR for Q1), and even higher than the median of the February survey of professional forecasters. However, that doesn’t mean the slowdown is canceled, just that it may be delayed.

{kind=link}

{kind=link}