Dean Baker has an interesting article Driven by gasoline, automobiles and food, it is speculated that CPI will fall in the future. This argument seems reasonable, depending on the supply chain and the oil market. I want to consider what might happen, depending on other components.

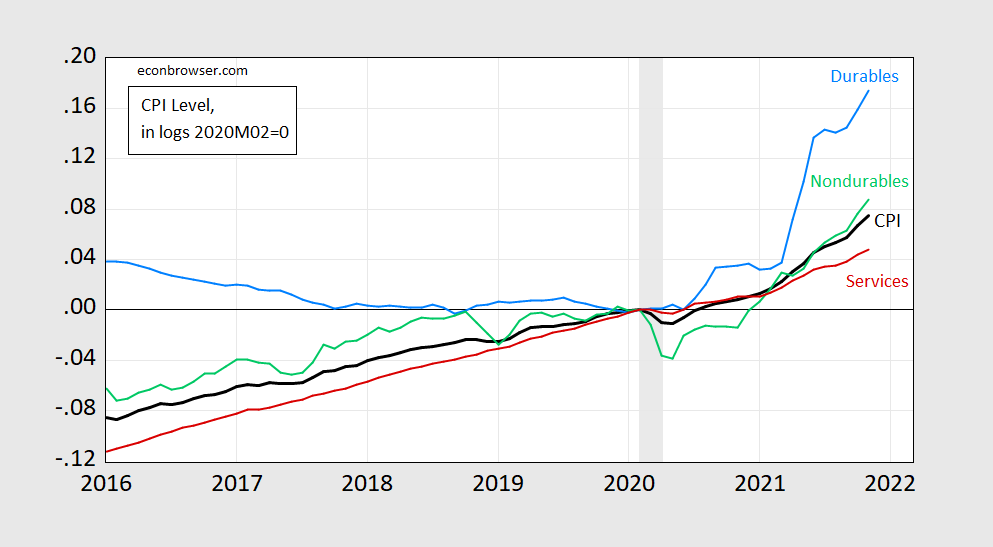

First, consider that the factor driving overall inflation is largely the soaring price of durable goods.

figure 1: CPI-all cities (black bold), CPI-durable goods (light blue), CPI-non-durable goods (light green) and CPI-services (red), all in the log, 2020M02=0. NBER-defined recession dates are shaded gray from peak to trough. Source: BLS (published in November 2021) calculated by FRED, NBER and the author.

If public health problems decrease, then as consumption shifts to services, durable goods prices may stabilize or even decline. Remember that the supply chain issues that involve transporting goods from the place of production to the place where they are needed are largely driven by the surge in demand for the goods—not the decline in the port’s supply capacity, etc. This is Baker’s variant argument, among others.

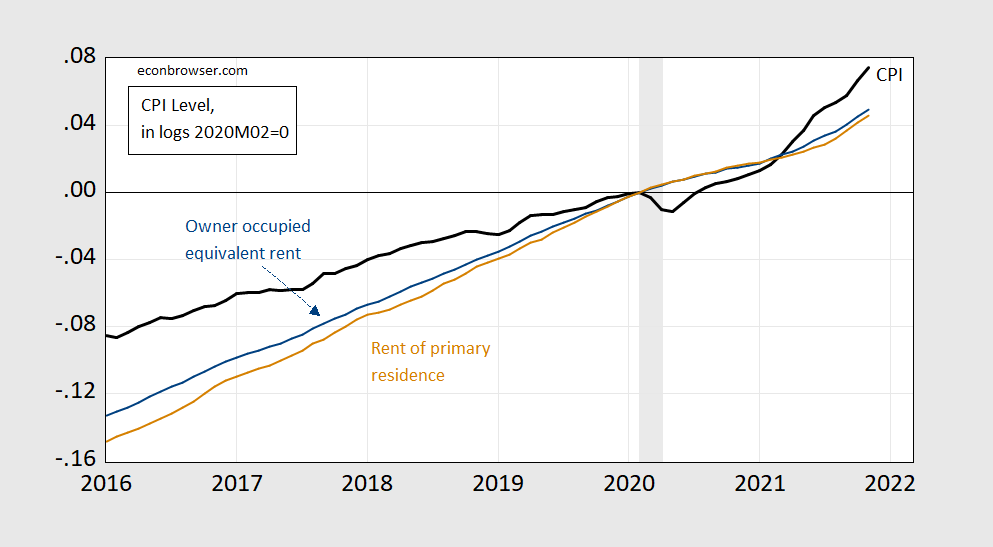

Another area of concern is housing costs, which are clearly rising:

figure 2: CPI-all cities (black bold), CPI-owner’s own equivalent rent (blue), CPI-main residential rent (tan), are all in the log, 2020M02=0. NBER-defined recession dates are shaded gray from peak to trough. Source: BLS (published in November 2021) calculated by FRED, NBER and the author.

In October 2021, the rent of main residential buildings accounted for 7.6% of the total weight, and the rent of owners’ equivalent residential buildings accounted for 23.5% (see Table 6) release). The former growth accounted for 1.3 percentage points of the 9.8% CPI inflation rate in November, while rent growth accounted for 0.4 percentage points.

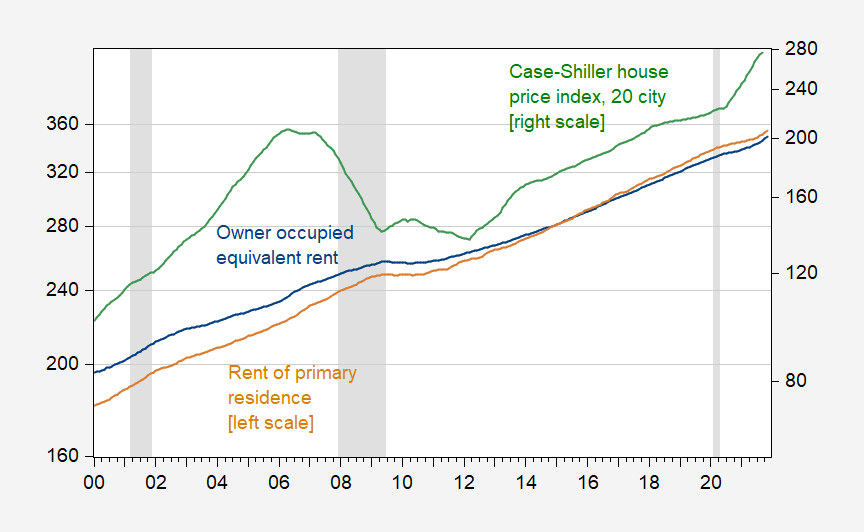

One reader Pointed out that the accelerated rise in rents for owner-occupiers may continue.

The average lag time from the housing price index to the CPI owner’s equivalent rent is 18 months.

It is expected that year-on-year inflation in 2022 will remain unchanged or may even increase

The CPI measurement of rent is also measured in a way that lags behind the commonly observed rent measurement.

This is a comparison chart of the landlord’s own rent (and rent) and the house price.

image 3: CPI-owner-occupied equivalent rent (blue, left logarithmic scale) and CPI-primary residential rent (tan, left logarithmic scale), Case-Shiller 20 City Housing Price Index (green, right logarithmic scale). NBER-defined recession dates are shaded gray from peak to trough. Source: BLS (published in November 2021) through FRED, Standard & Poor’s through FRED, NBER and author’s calculations.

Visual inspection seems to reveal a relationship, especially in y/y changes (but not in long-term cointegration). At 18 months (using non-overlapping changes), the relationship is 0.08-that is, a 1 percentage point increase in y/y growth rate results in a 0.08 percentage point increase in OER component growth rate. Literally, the 17.5% year-on-year change in September (in logarithmic terms) means that by March 2023, the OER inflation rate will therefore be 1.4 percentage points higher. Since I have no confidence in the return (considering some diagnostic results), I am not going to bet on this number.

{kind=link}

{kind=link}