Talk about the dollar as a reserve currency next week [2]and noticed these interesting trends.

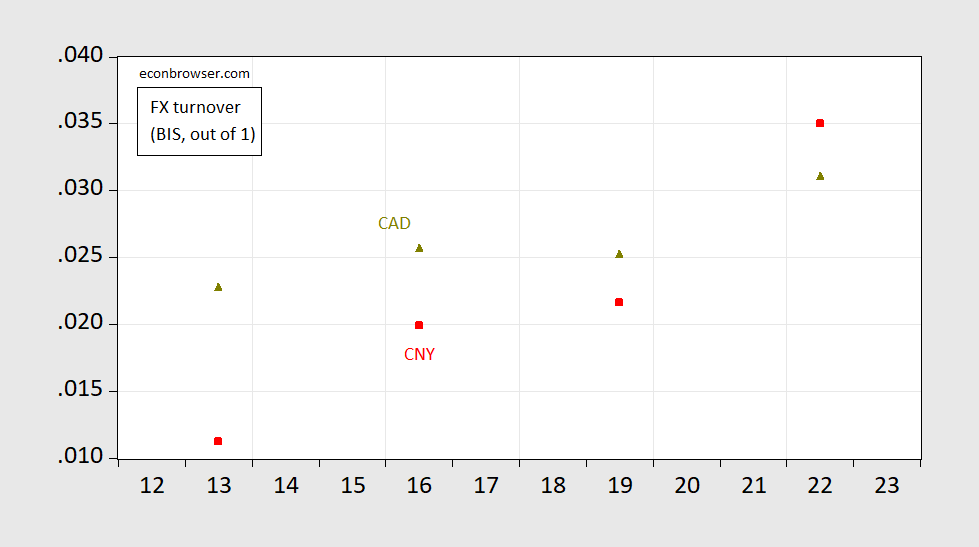

figure 1: Share of FX trading volume in April in Chinese yuan (red squares) and Canadian dollars (yellow-green triangles). Stocks are normalized to 1.00. Source: Bank for International Settlements three-year survey.

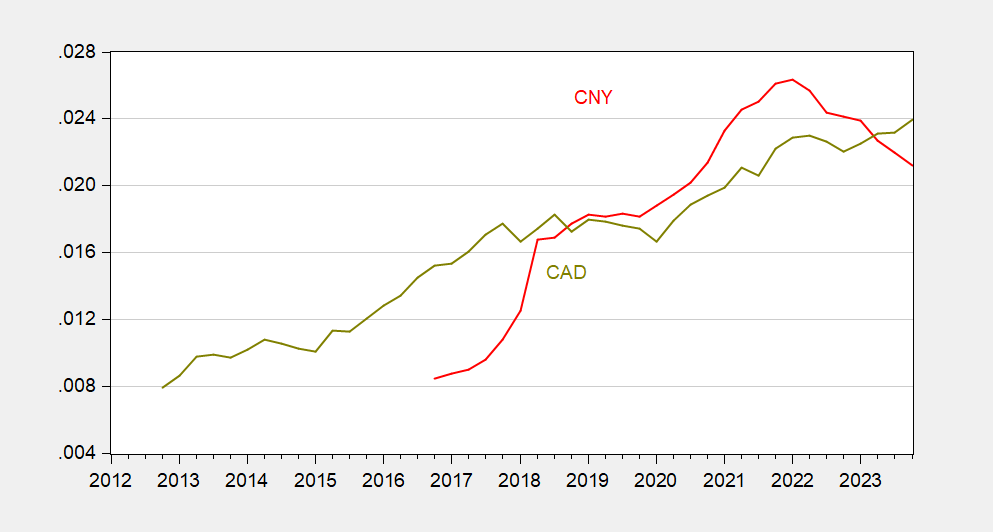

A similar pattern exists for reserves held by central banks, as reported by the International Monetary Fund's COFER.

figure 2: Central bank reserve shares are expressed in Chinese yuan (red) and Canadian dollars (yellow-green). Source: International Monetary Fund.

Although the share of RMB holdings has shrunk since 2022, explaining this trend is complicated. Most, if not all, of the decline is likely caused by the depreciation of the yuan against the US dollar (9% in logarithmic terms, compared with a decline of about 5 percentage points).

Nonetheless, as discussed, I don’t think the RMB will become a major international currency anytime soon here (Keep in mind that at the end of 2023, the euro accounted for 18.5 percentage points of the central bank’s total foreign exchange reserves).

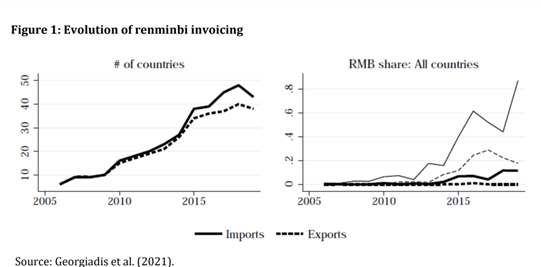

Not surprisingly, given China's dominance of trade, one area where the yuan has become important is in pricing. Ito and Chinn (2014) discuss this issue, but the most recent estimate is by Georgiadis(2021).

notes: The left chart shows the number of countries with RMB denominated data. The right chart shows the share of exports and imports invoiced in RMB, along with the median (thick line) and the 75th percentile (thin line).

{kind=link}

{kind=link}