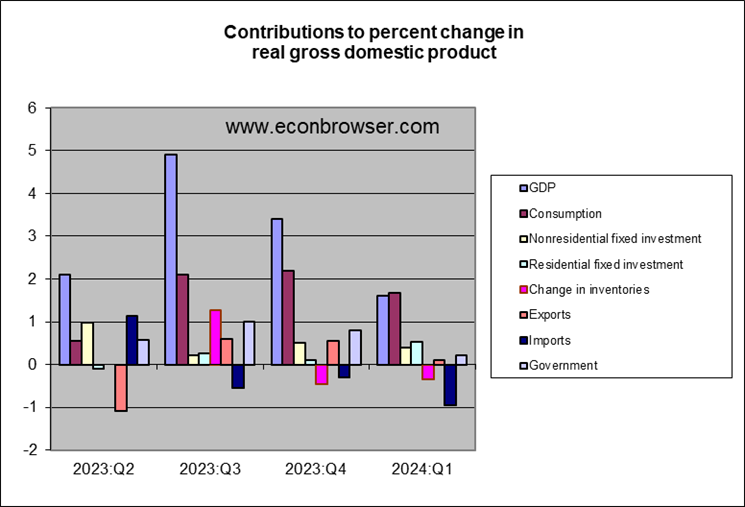

this Bureau of Economic Analysis It was announced today that the seasonally adjusted annual real GDP growth rate of the United States in the first quarter was 1.6%. That was slightly lower than many analysts expected. But year-on-year growth is still on track.

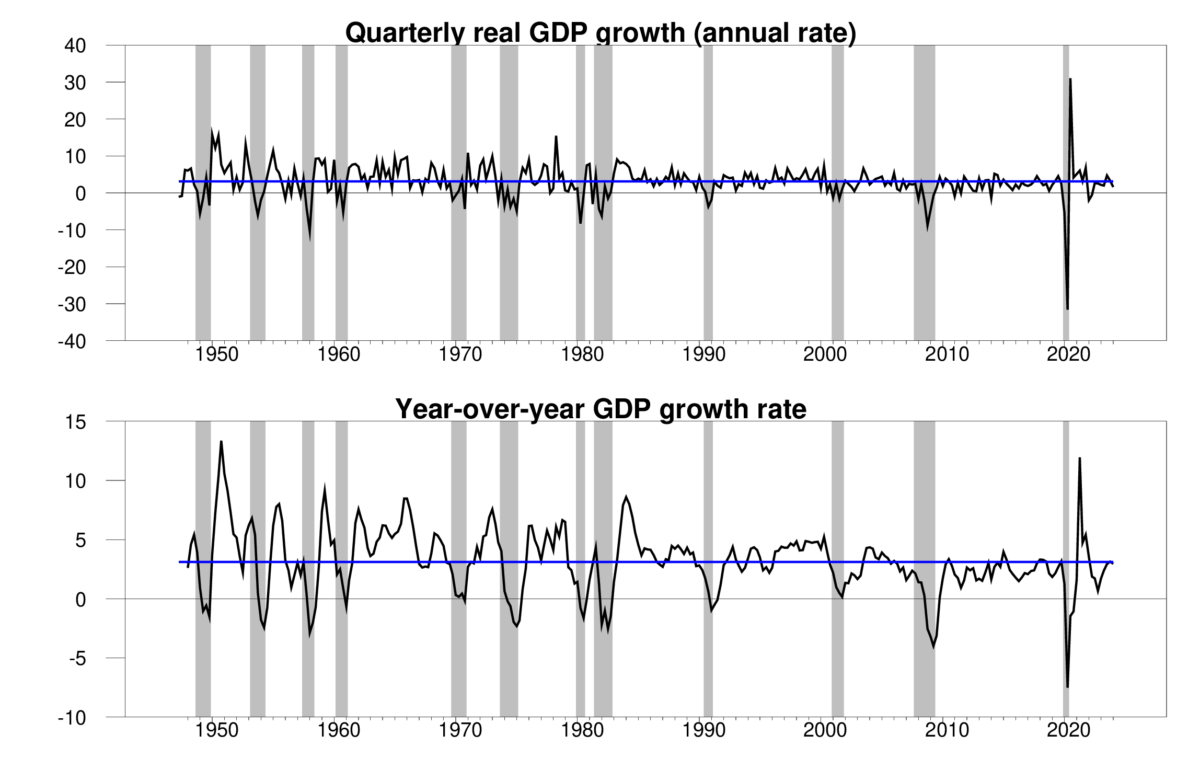

Above: Quarterly real GDP growth at an annualized rate, Q2 1947 to Q1 2024, with the historical average (3.1%) in blue. Calculated as 400 times the natural logarithm difference between real GDP and the previous quarter. Below: Annual growth rate. Calculated as 100 times the difference between the natural logarithm of real GDP and the same quarter of the previous year.

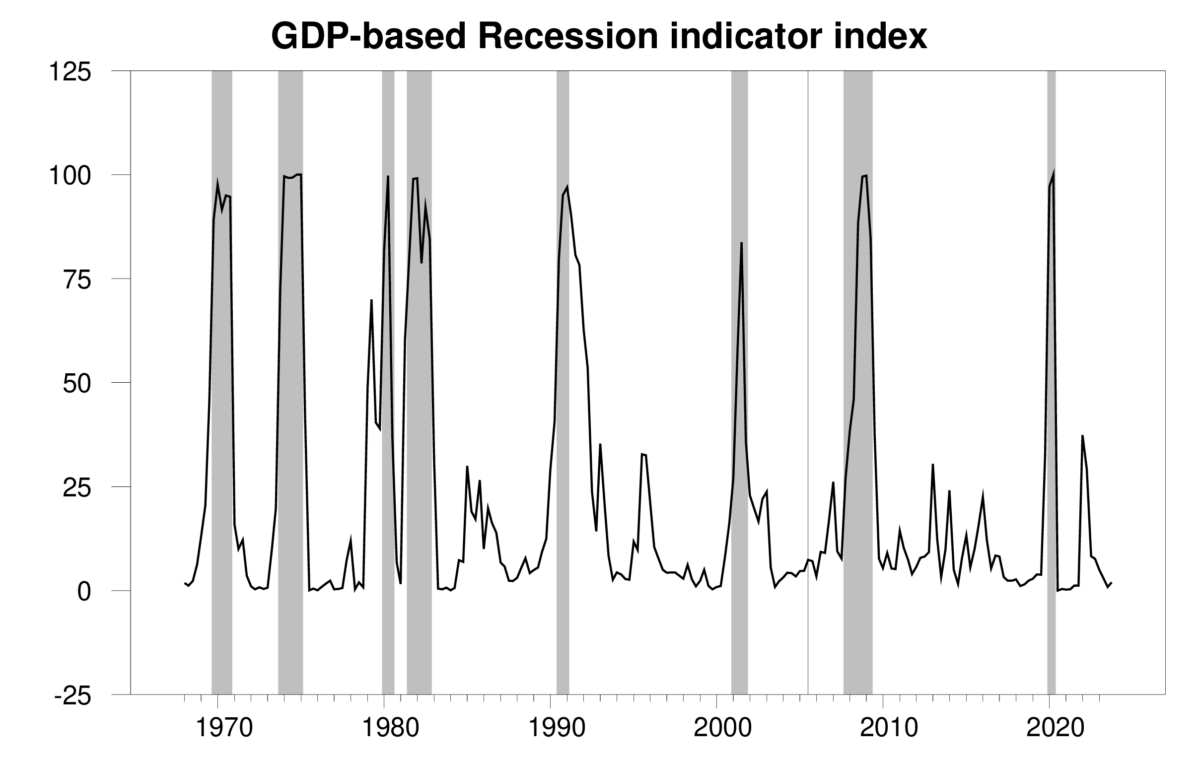

new numbers will Ecobrowser Recession Indicator Index 2.0%, a very low level, indicating a definite continuation of the economic expansion that began in the third quarter of 2020.

GDP-based recession indicator index. The values plotted for each date are based only on publicly available GDP data for the quarter after the specified date, with Q4 2023 being the last date shown on the chart. The shaded area represents the NBER's recession date, which was not used in any way in constructing the index.

The key factor behind weak GDP growth is a surge in imports, which are excluded from GDP calculations. Import estimates are volatile and subject to revision.

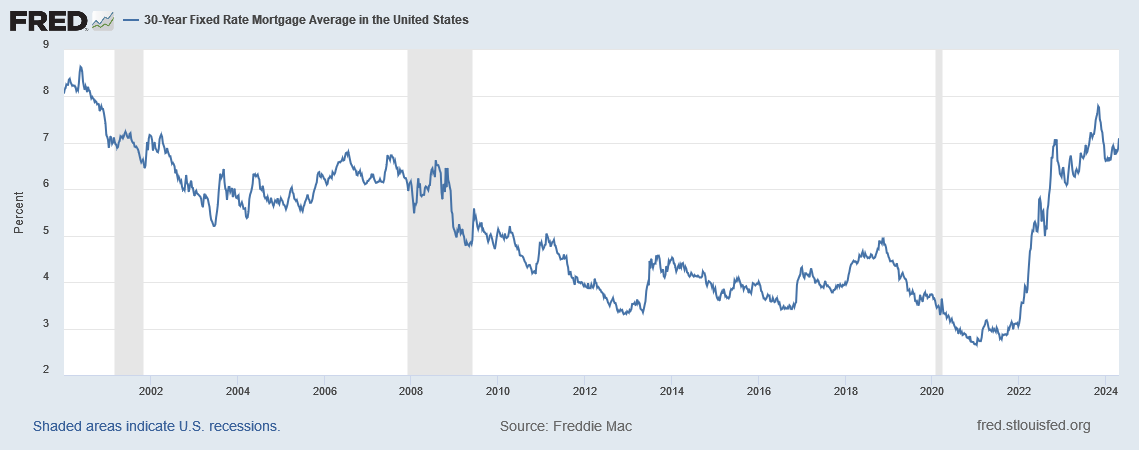

Despite higher interest rates, residential fixed investment made a decent contribution to first-quarter GDP growth. Mortgage rates fell between November and February but have since recovered.

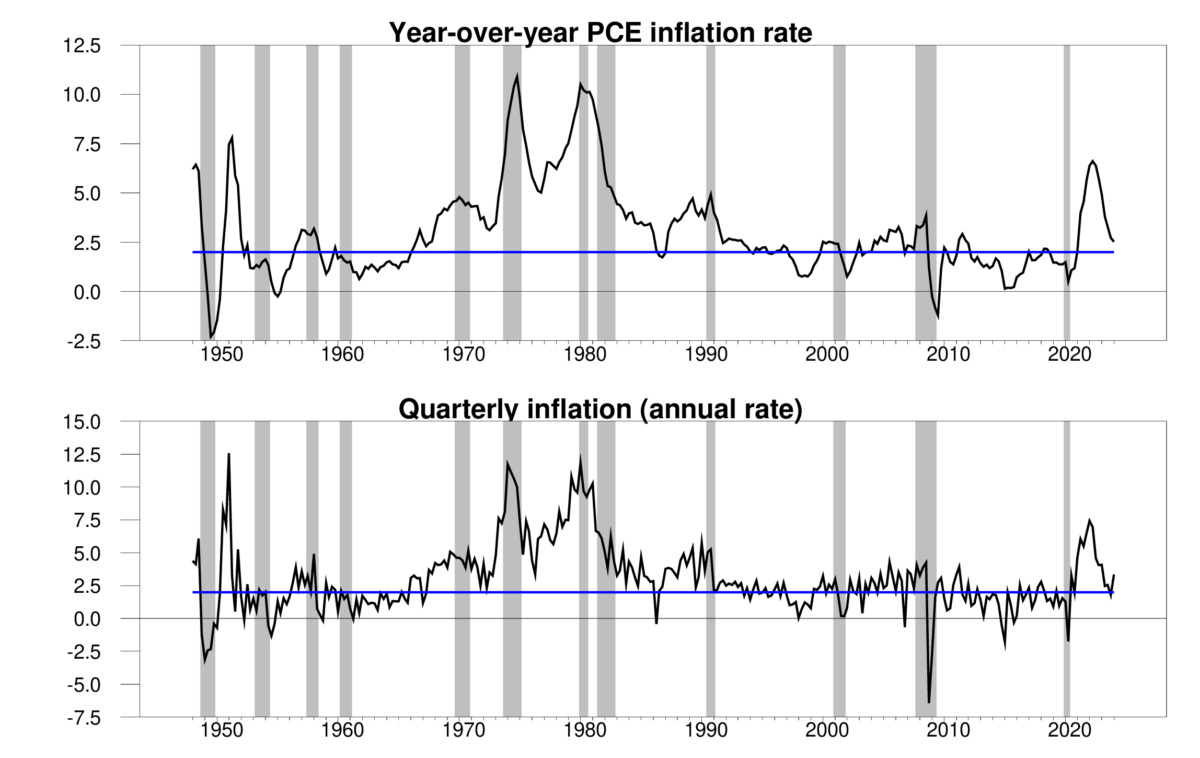

The reason for the recent rise in mortgage rates is that the Federal Reserve has not made the progress in lowering inflation that many had hoped. The new GDP report was also a bit disappointing. The implicit personal consumption expenditure deflator grew at an annual rate of 3.3% in the first quarter. The year-over-year rate was 2.5%, slightly better than the quarterly increase but still above the Fed's 2% target.

Top panel: 100 times the natural log difference Personal consumption expenditures implied price deflator Compared to the same period last year. Below: 400 times the difference between the natural logarithm of the PCE deflator and the previous quarter's value.

The lack of further progress on inflation has led to a significant shift in market expectations for the Fed's next steps. At the beginning of December 2023, futures contract The federal funds rate in December 2024 is 4.3%, consistent with four 25 basis point cuts to the federal funds rate this year. The contract currently implies an interest rate of 5% in December. Traders now expect just one rate cut, and not until later this year.

Some supply-side factors are also likely to push inflation higher. The two presidential candidates appear to be competing over who can raise the price of imported goods the most. Geopolitical risks could lead to higher energy prices.and similar measures California’s minimum wage for fast food workers to be $20 Can't help.

The Fed still appears to have achieved the coveted “soft landing,” lowering inflation without triggering a recession. But I have to admit, the plane hasn't quite landed yet.

{kind=link}

{kind=link}