That’s the title of today’s show WPR Central Time, I am a guest there. In my view, the economy’s durability so far is largely due to the resilience of consumers boosted by COVID-era transfers. Consumption has also increased as disposable income is higher than expected a month ago and – with savings rates lower against a tight labor market backdrop – there is a greater buffer of “excess savings”.

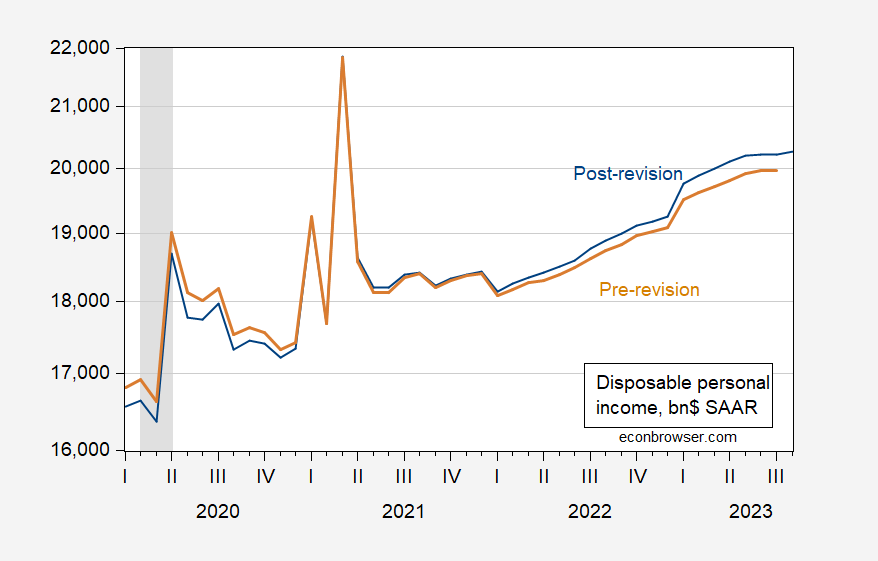

figure 1: Disposable income before full revisions (tan), after full revisions (blue), in billions of dollars, SAAR. NBER-defined recession peak-to-trough dates appear gray. Source: BEA, via ALFRED, NBER.

FuGuo bank Using the revised data, it is estimated that “excess savings” in August were approximately $1.1 trillion, while using pre-revised data, “excess savings” in July were approximately $340 billion. How can this happen when the cumulative difference in disposable income is about $153 billion and the cumulative difference in consumption is $453 billion (i.e., after revision, consumption is much higher)? The difference stems from the lower assumed savings rate (7.2% vs. 9.1%), which defines “normal” saving levels downward and “excess saving” levels upward.

Therefore, it is not surprising that consumption continues to be strong.

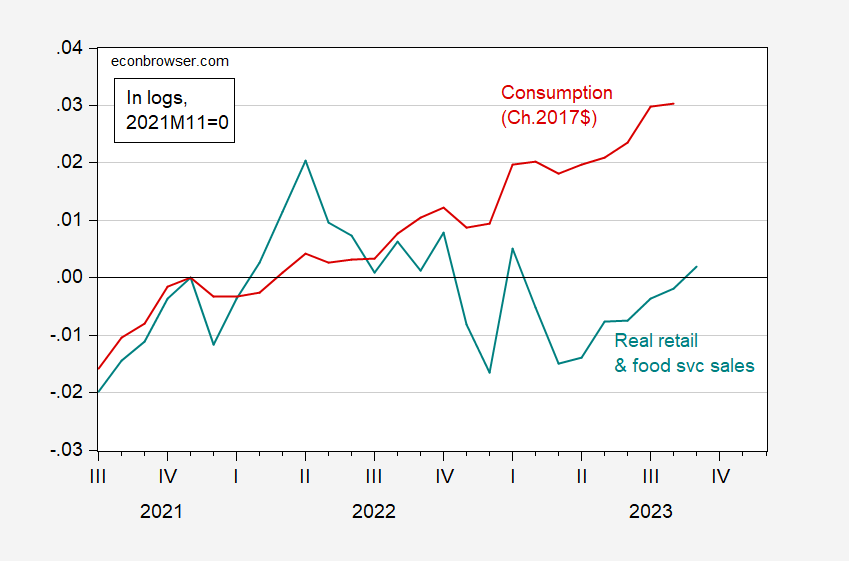

figure 2: Actual retail and food service sales (cyan) and actual consumption (red), both logarithmic, November 2021 = 0. Retail and food service sales (FRED series RSAFS) declined due to the Chain Consumer Price Index (seasonally adjusted to X13). Sources: Census, Bureau of Labor Statistics, Bureau of Economic Analysis, and author’s calculations.

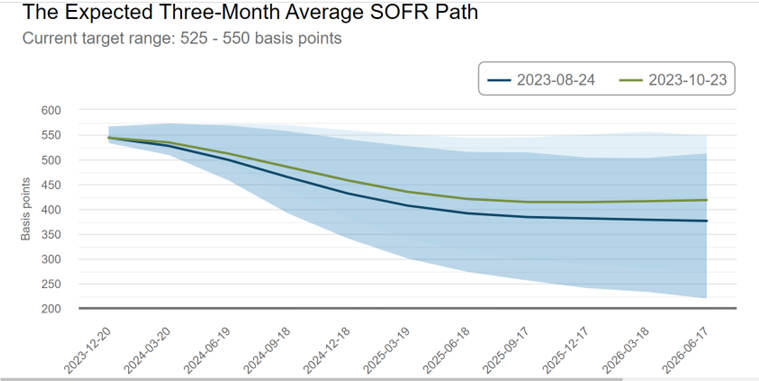

As the economy’s resilience emerges time and time again, the expected recession date is being pushed back further – or canceled (see this postal) – The federal funds path is pushed further higher. Please see the combined pre- and post-revised path of GDP, shown in Figure 3 below.

image 3: Implied path for federal funds, from the Atlanta Fed, August 24 (blue) and October 23 (green). source: Atlanta Fed Probability Trackeraccessed on October 24.

{kind=link}

{kind=link}