Or why I still think a recession is likely in the first half of 2024.

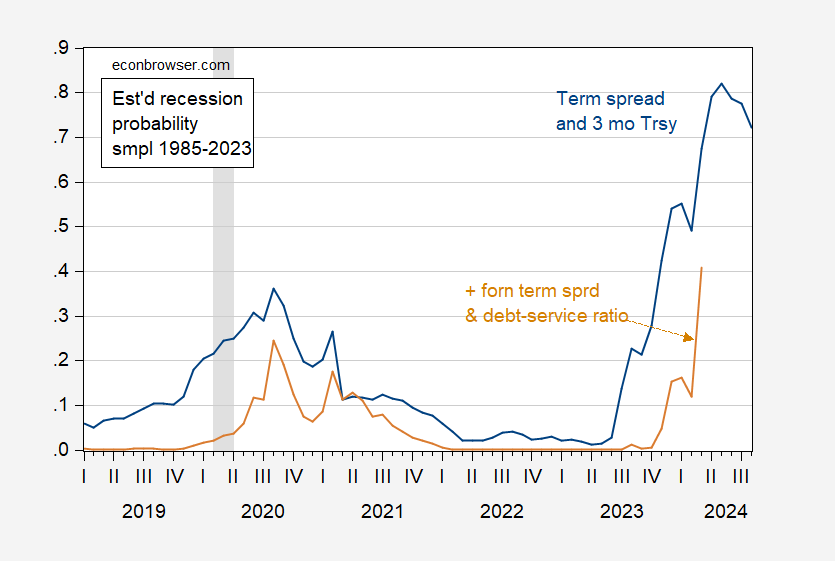

BIS just released debt ratio Season 1, 2023. Using this variable along with term spreads and foreign term spreads, the estimated odds of a recession in Q1 2024 have risen significantly, although they remain well below the corresponding figures using only term spreads/short rates.

figure 1: NBER-defined recession probabilities are estimated using the 10-year to 3-month term spread plus the 3-month Treasury rate (blue) and a specification augmented by the foreign term spread and the debt service ratio (tan). Debt service ratios apply to the private non-financial sector. NBER-defined recession peak-to-trough dates appear gray. Source: Author’s calculations and NBER.

The chance of a recession in the forecast month rose from 12% in February 2024 to 41% in March 2024. This highlights the fact that probabilistic regression involves estimating a non-linear relationship between the dependent and independent variables. Growth in debt ratios looks quite modest.

Having said that, the enhanced specification implies far lower odds than the term spread and short rate only specifications (68% in March 2024 compared to 41% for the enhanced specification).Motivation for using debt service ratio as a proxy for the financial cycle Borio Dreman-Xiathis foreign word spread like this Ahmed Chin,look at this postal.Additional analysis in collaboration with other countries Laurent Ferrara exist Slides here.

Figure 2 plots the evolution of term spreads and debt service ratios for the private non-financial sector.

figure 2: 10-year to 3-month Treasury spread, % (blue, left axis) and debt service ratio, % (tan, right axis). NBER-defined recession peak-to-trough dates appear gray. Source: Treasury via FRED, Bank for International SettlementsNBER, and author’s calculations.

Note that term spreads became more negative in the first quarter of 2023 as debt service ratios rose. The estimated odds increased by 18 percentage points for the unenhanced specification and by 29 percentage points for the enhanced specification.

One might ask why one should prefer enhanced norms to unreinforced norms. The pseudo R2 for the term spread plus the short rate specification (1985-2023M08) is 0.28, while the pseudo R2 for the debt service and foreign term spread is 0.60. (The pseudo-R2 for debt service alone is 0.32, but that means the probability of a recession in March 2024 is essentially zero).

Additionally, the enhanced specification captures 3 of the 4 recessions during the sample period, using a 50% threshold (the 2020 recession is omitted). Term spreads plus short rates only capture the 2001 recession, while debt service ratios alone fail to capture all four scenarios (closer to the 2007-09 recession). Using a 40% threshold reduces the differences between models, with both the term spread plus short rates and the augmented model capturing 3 of the 4 recessions (the debt service ratio captures only the 1990-91 and 2007-09 recessions) . All specifications do not take into account the 2020 recession.

Fun fact: Even if you think that the word spread is no longer a reliable predictor (e.g. Putnam), that doesn’t mean you can relax.

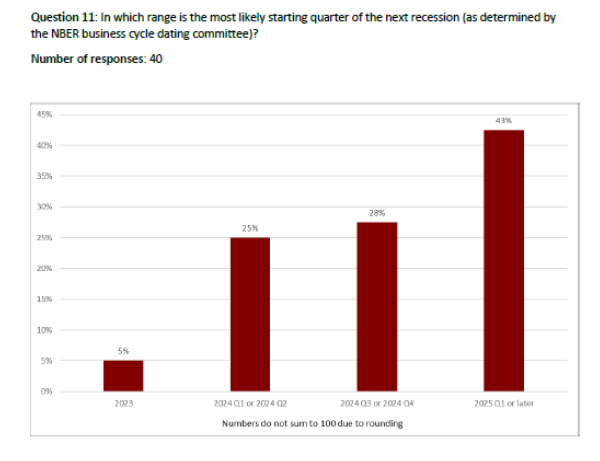

Therefore, despite the dominance of the “soft landing” view, the above results are consistent with the view of a recession in the first half of 2024, which accounts for about 53% of the FT-Booth School macroeconomists survey:

source: Booth School (September 2023).

Note that some analysts are predicting a recession while acknowledging that such a recession may not meet the NBER’s criteria – e.g. Oxford Economics.

{kind=link}

{kind=link}