On Friday (July 29, 2023), the Australian Bureau of Statistics released the latest data—— Australian retail industry – Data showed that total retail sales fell 0.8% in June 2023 and rose 2.3% in June 2022. Growth of 4.1% in May 2023. So things slow down. Almost all components (household goods, clothing, etc., department stores, cafes, etc.) were down for the month. The ABS noted that while EOFY sales were huge, “retail turnover fell sharply as cost-of-living pressures continued to weigh on consumer spending”. In the United States, by contrast, June data from the U.S. Census Bureau – Monthly sales advances for retail and food services (Published July 18, 2023) – Up 0.2% in June. In addition, the latest consumer sentiment survey results from the University of Michigan — Improving personal finances, business conditions boost consumer confidence (Published July 28, 2023) – Reveals sharp rise in US consumer confidence. But there’s a twist, and that’s the point of this post. “Consumers’ experience of the economy has improved materially compared with last year’s high-inflation peak … with the exception of low-income consumers, who expect inflation to continue to be challenging and labor market prospects that are likely to weaken,” the survey reported. What we are going to discuss today is that central bankers actually work to increase poverty in society. And, no matter how you look at it, relying on this pernicious policy tool—a policy that deliberately increases poverty—is not a solid foundation for social stability. And, despite rising inflation, which has been falling anyway, the negative distributional impact should discourage the use of such a nasty and inefficient tool.

In radio interviews and in private discussions with reporters, the question I’m often asked is why the U.S. economy isn’t in trouble when the Fed keeps raising rates, and why the Australian economy isn’t doing so when the RBA isn’t raising rates. But quickly slowing down to hike less and be late to the party?

In this blog post I provide some guidance on why interest rate changes may affect the US and Australia differently – RBA chief’s ‘let them eat brioche’ moment of defiance (June 8, 2023).

I note several factors that affect the response to rate hikes.

First, no one really knows whether winners of rate hikes will spend more than losers cut spending.

Evidence suggests that the effect of wealth on consumer spending is relatively low compared to the effect of income.

But there are many complexities – like saving buffers etc – that make it hard to be sure.

Second, in the short term following a rise in interest rates, debtors’ spending responses may be limited as they are able to adjust their wealth mix (save less, etc.) to absorb the contraction.

Thus, rising interest rates can trigger inflation as businesses pass on increased borrowing costs in the form of higher prices, and as noted above, landlords pass on higher mortgage servicing costs into higher rents, which in turn This again led to inflation. Included in CPI data.

Third, in the medium to long term, if interest rates rise above a certain threshold, the effect will be a slowdown in spending and higher unemployment.

Eventually, those who benefited from the rate hike, usually with a lower marginal propensity to spend (how much they spend from each extra dollar they receive), will run out of things to buy and pocket the bonus.

Eventually, spending cuts by debtors, especially low-income mortgage holders, began to dominate.

In order to make an assessment, we must consider:

1. Household debt levels – the higher the debt, the greater the negative impact of rate hikes on spending.

2. Proportion of the population with mortgage debt – the higher the proportion, the more likely the medium- to long-term effects will dominate.

3. Crucially, the ratio of fixed-rate mortgage debt to variable-rate mortgage debt.

In the U.S., while debt levels are relatively high by historical standards, outstanding mortgages are mostly long-term, fixed-rate and held by people higher in the income distribution, meaning rising interest rates are unlikely to lead to sharp cuts in spending from mortgages loan holder.

Then, wealth holders’ higher incomes from Fed rate hikes dominate.

In Australia (and the rest of Europe, the UK, Canada, etc.), the vast majority of mortgages are variable rate and are more likely to be held by low-income households, so increases in mortgage payments will squeeze disposable income and eventually bankruptcy.

These insights focus our assessment of monetary policy implementation on distributional issues, which is why I looked at data from the latest University of Michigan survey last week.

I write about the distributional impact of monetary policy in these blog posts:

1. Monetary policy in the hands of central bankers sociopaths is advancing elite class interests (July 5, 2023).

2. The RBA is implementing one of the largest per capita disposable income cuts in history (March 8, 2023).

The latest survey of consumer sentiment in the US shows that the results are back to levels seen around October 2021 and have risen sharply in recent months.

In June 2022, the index was 50 points, and it is currently 71.6 points.

Between June and July 2023, the index rose from 64.4 to 71.6, an increase of 11.2% (one of the largest monthly gains in the index’s history).

The chart below shows the evolution of the index from January 2013 to July 2023.

But new survey data reveals stark differences in the fortunes of the top 10 per cent versus the bottom earners, helping to explain why retail behavior differs between Australia and the US.

It also allows us to understand why monetary policy is an unwise macroeconomic policy tool.

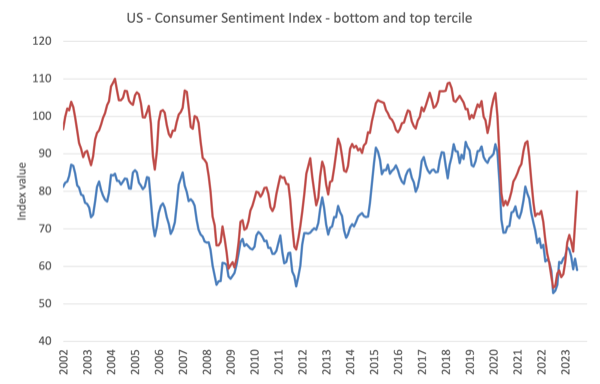

A tertile is generated when a data set is divided into three equal parts (bottom third, middle third, and top third).

The chart below shows the evolution of the top and bottom tertile surveys between 2002 and July 2023

After a period of rising sentiment in both groups, the index for low-income consumers is now falling, but the index for the top 10% has risen sharply.

Like most central banks, the Fed (with the notable exception of the Bank of Japan) has attempted to quell inflationary pressures by raising interest rates.

Their stated goal is to increase unemployment because they believe this will hold down inflation, despite the fact that inflation is falling rapidly as supply-side factors weaken.

These factors are not weakened by rising interest rates, but because the world is adjusting to some extent to the shock of the new crown epidemic, Putin and most recently OPEC.

We also know that when unemployment rises, it affects low-income workers disproportionately — they are often the first to leave and the last to be rehired.

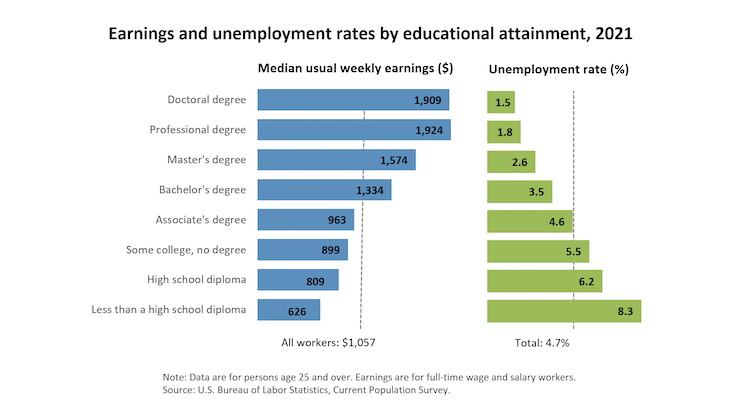

The chart below, produced by the U.S. Bureau of Labor Statistics, shows the link between education, income, and unemployment (in 2021).

Even though the overall unemployment rate is quite low (4.7% in 2021), there are large differences in unemployment rates by income group

In the US, this spreads disproportionately to minority groups (African-Americans are worse off).

Moreover, there is a direct positive relationship between unemployment and the incidence of poverty.

So, in effect, the goal of the Fed and other central bankers who raise rates is to cause poverty rates to rise among the most vulnerable workers in their communities.

They don’t express it that way – but that’s what they’re doing.

Currently, the unemployment rate has not risen significantly, but if the unemployment rate continues to rise, the unemployment rate will rise.

Currently, what we observe is:

1. Consumers with higher incomes are also less likely to be affected by job losses and have higher discretionary spending power, which gives them more room to adjust to inflationary pressures without significantly lowering their living standards, they feel Very confident.

2. The income of this group has also increased significantly because they are more likely to hold financial assets and their mortgages are mostly fixed rate.

3. Also, lower-income consumers have much less, or even zero, discretionary spending power and are therefore hit harder by inflationary pressures, especially when a significant portion of their income is spent on food and energy.

4. While they are less likely to have large mortgages in the US, they are more likely to be unemployed and have a lower savings buffer (if any).

5. So it should come as no surprise that their consumer confidence will now decline as the Fed continues to raise interest rates.

Worries about job losses among this group are growing even as inflation is falling.

in conclusion

Trying to figure out the impact of rising interest rates will involve a deeper analysis of the distributional impact of rate hikes.

Central bankers are as unclear as anyone about the net impact of their actions.

Borrowers lose and creditors benefit.

Those who hold financial assets benefit, and those with less wealth suffer.

The net impact depends on many of the factors mentioned above.

Clearly, the rate hikes have not yet led to recessionary conditions, probably because the winners of rate hikes are still spending freely on top of growing wealth, while lower income groups are cutting back, but not as much as expected. to the same extent.

Ultimately, if rates continue to rise, unemployment will rise as the wealthy reach a saturation point in their spending.

Lower inflation also helped, as pressure on the cost of living eased for the poorest households.

In America, the poorest are less likely to get a mortgage, so for them the threat of higher rates is rising unemployment.

In Australia, lower-income households take out a higher proportion of mortgages than in the US, and are more likely to be variable-rate loans.

That’s why the impact of rate hikes looks more severe overall.

But no matter how you look at it, relying on such a harmful policy tool that deliberately increases poverty is not a solid foundation for achieving social stability.

And, despite rising inflation, which has been falling anyway, the negative distributional impact should discourage the use of such a nasty and inefficient tool.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}