Not only did the surveys differ across groups, but also across groups within households.

figure 1: Median CPI inflation expectations for the year ahead are from the Survey of Professional Forecasters (blue+), median expectations from the Michigan Final Survey of Consumers (red), medians from the New York Fed Survey of Consumer Expectations (light green), from Average of the Coibion-Gorodnichenko Company Expectations Survey [light blue squares], all expressed in %. Michigan’s preliminary inflation expectations for January. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. The dashed red line indicates Russia’s expanded invasion of Ukraine.Source: University of Michigan, via FRED and Philadelphia Fed Survey of Professional Forecasters, the fedand Coibion and Gorodnichenkoand the National Bureau of Economic Research.

As mentioned earlier, expectations from surveys of consumers and households are generally higher than those from surveys of economists. More recently, firm expectations have been higher than households.

The differences between households and firms are discussed at length in an excellent survey Weber, D’acunto, Gorodnichenko and Coibion (Give2022). Here are some pictures of the differences by family, income and education level. Since it is difficult to see differences across the sample, I present available data from 2013M06-2022M12, split into pre-pandemic and pandemic periods.

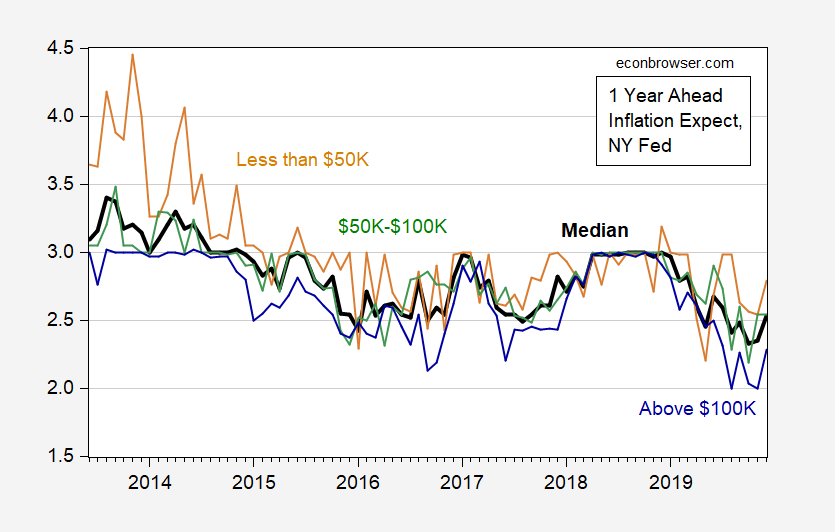

figure 1: 2013M06-19M12, HH Income below $50k (tan), $50k to $100k (green), over $100k (blue) expected median CPI inflation (bold black) one year ahead . source: the fed.

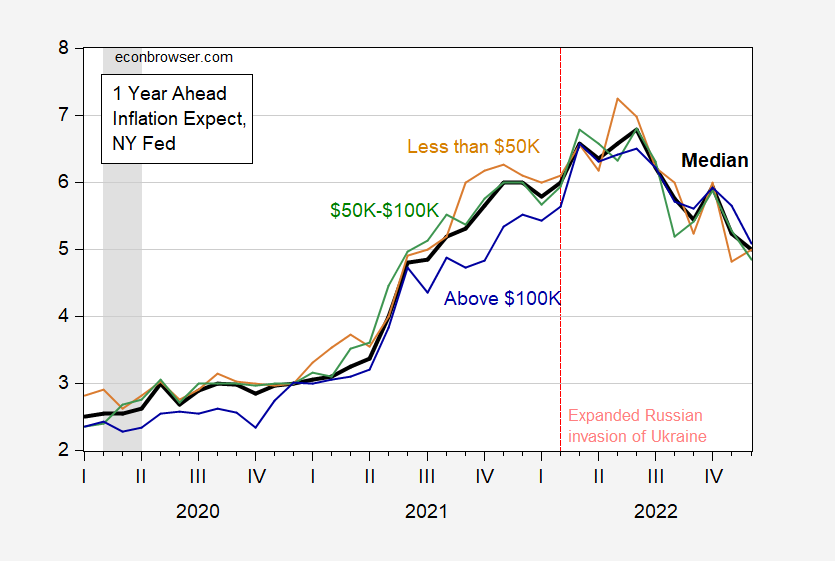

figure 2: Median expected CPI inflation for households with incomes below $50,000 (tan), $50,000 to $100,000 (green), and above $100,000 (blue) from January 2019 to December 2022 (rough body black) one year in advance. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. source: the fedU.S. Bureau of Economic Research.

image 3: Median expected CPI inflation (bold black) for high school or less (tan), high school and some college (green), BA or higher (blue) from January 2013 to December 2022 year. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. source: the fedU.S. Bureau of Economic Research.

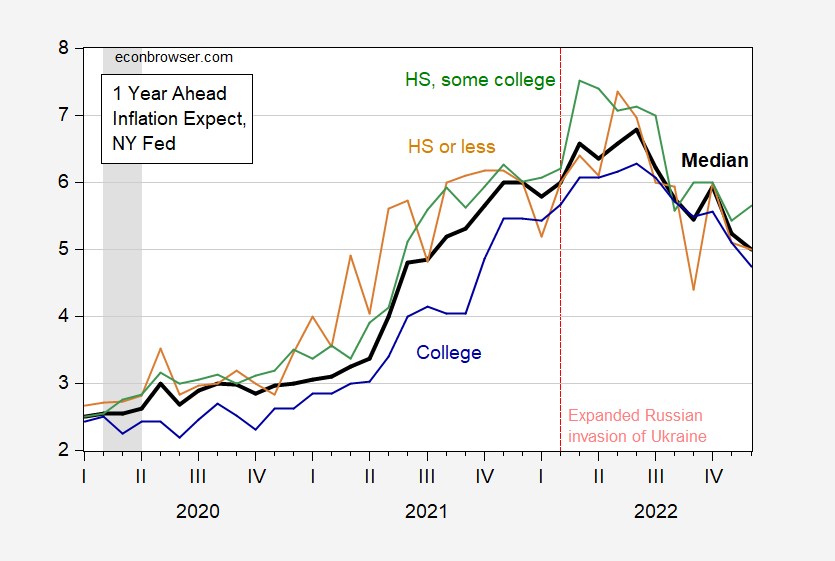

Figure 4: Median expected CPI inflation (bold black) for high school or less (tan), high school and some college (green), BA or higher (blue) from January 2019 to December 2022 year. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. source: the fedU.S. Bureau of Economic Research.

The Bottom Line on Income Group Forecasts – People with lower incomes tend to have higher inflation forecasts. This was true both before and after the pandemic. The higher predicted inflation rate may be due to the higher inflation rate experienced by these groups (i.e., higher expected inflation rate is associated with higher current inflation rate). recall, CPI is owned by chaebols, that is, it represents the consumption bundle of approximately the 70th percentile of households. It must be noted that, on average, household expectations are more upwardly biased than surveys of professional forecasters.

For levels of educational achievement, it appears that the degree of deviation from the median expectation depends on the time period. For example, respondents who were high school seniors or younger reported higher expectations in 2013-14 and in the 2021 and 2022 midterms. These are the times when gasoline prices are rising. In other words, these households put more weight on gas prices than less educated households.

As for business, Weber et al. (2022) notes:

Observed price signals affect aggregate inflation expectations not only of households but also of firm managers, who focus on the price signals they observe in their industries. For example, firms in industries with higher recent inflation rates tend to form higher beliefs about headline inflation even though these industry-level price changes are unrelated to headline price changes (Andrade et al. forthcoming). The importance of directly observed price changes as individual-level signals that help explain aggregate inflation expectations is a finding that is prevalent in the literature.

{kind=link}

{kind=link}