Michael Kiley (FRB) recently published a work documents It shows that various indicators have greater predictive power in different ranges.Other papers have demonstrated this Different term spreadfor credit spread, foreign term spread; in this case, Kiley shows that unemployment and inflation are more predictive in the long run than in the short run.

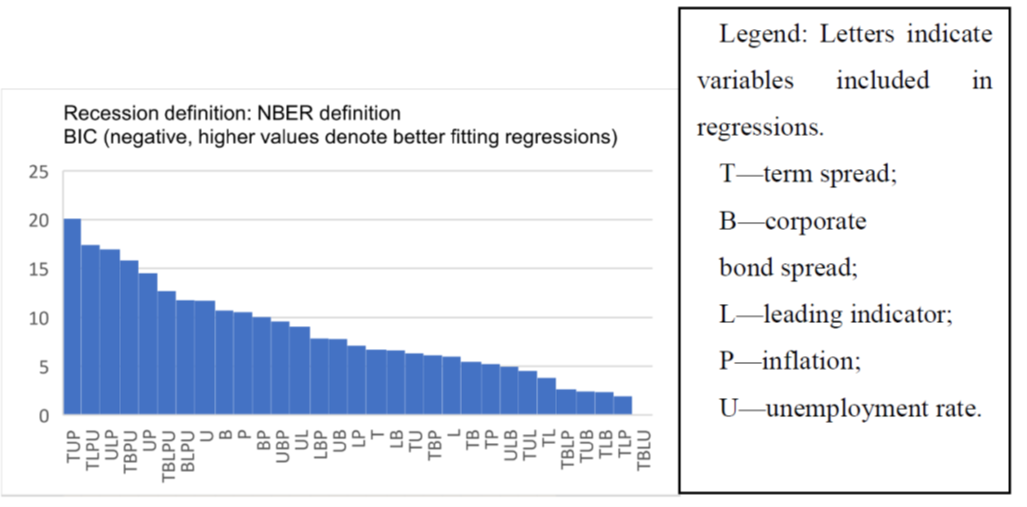

For the four quarters ahead, the term spread works best.

source: Kiley (2023), Figure 4, bottom panel. T is the 10-year fed funds term spread, U is the unemployment rate, and P is the PCE y/y inflation rate.

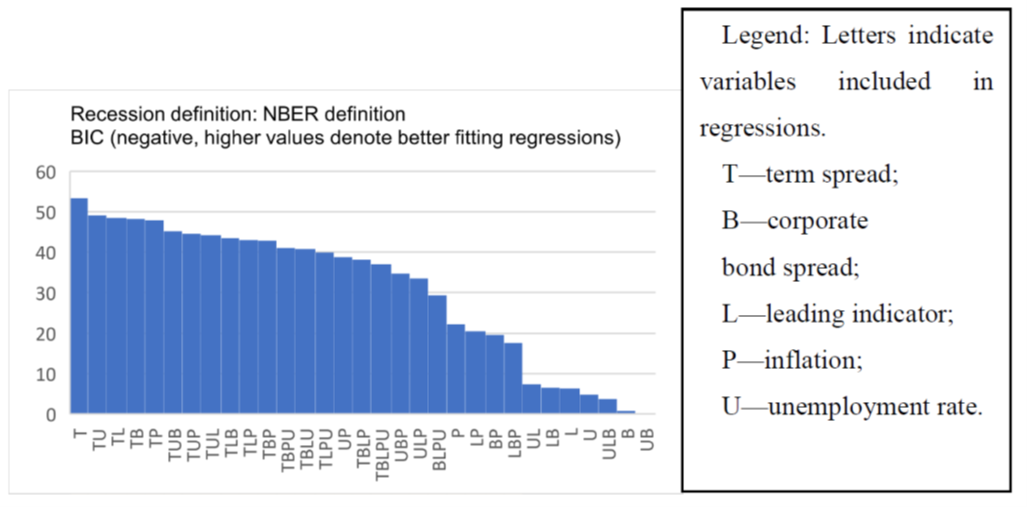

Specifications including inflation and unemployment are most effective for recessions in the four quarters preceding the four quarters.

source: Kiley (2023), Figure 5, bottom panel. T is the 10-year fed funds term spread, U is the unemployment rate, and P is the PCE y/y inflation rate.

Note that Kiley also takes into account predictive power, where a recession is defined as a large increase in unemployment and a large decline in GDP per capita. Here, I focus on NBER-defined recessions.

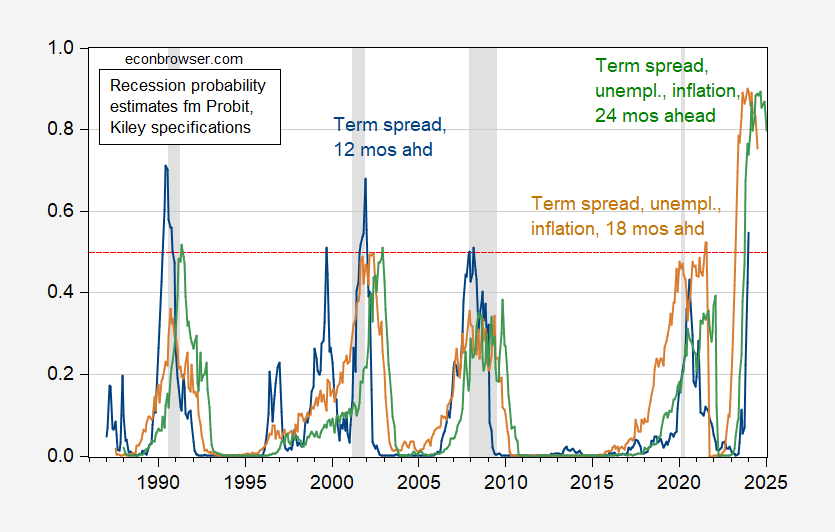

What do Kiley’s results imply for the current situation (i.e., do current levels of inflation and unemployment imply a different estimated recession probability than using term spreads alone)? I run a probabilistic regression on term spreads, term spreads plus PCE inflation plus unemployment for the next 18 and 24 months using data through January 2023 (I assume UE rises to 3.6%, inflation as forecast by the Cleveland Fed).

image 3: Implied recession probabilities using 12-month term spread (blue), 18-month term spread, unemployment, inflation (tan), 24-month term spread, unemployment, inflation (green). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: NBER, author’s calculations.

These probabilities crossed the 50% threshold around 2023M04. (Note that I’m using slightly different specs, in 12 months, not in 12 months).

{kind=link}

{kind=link}