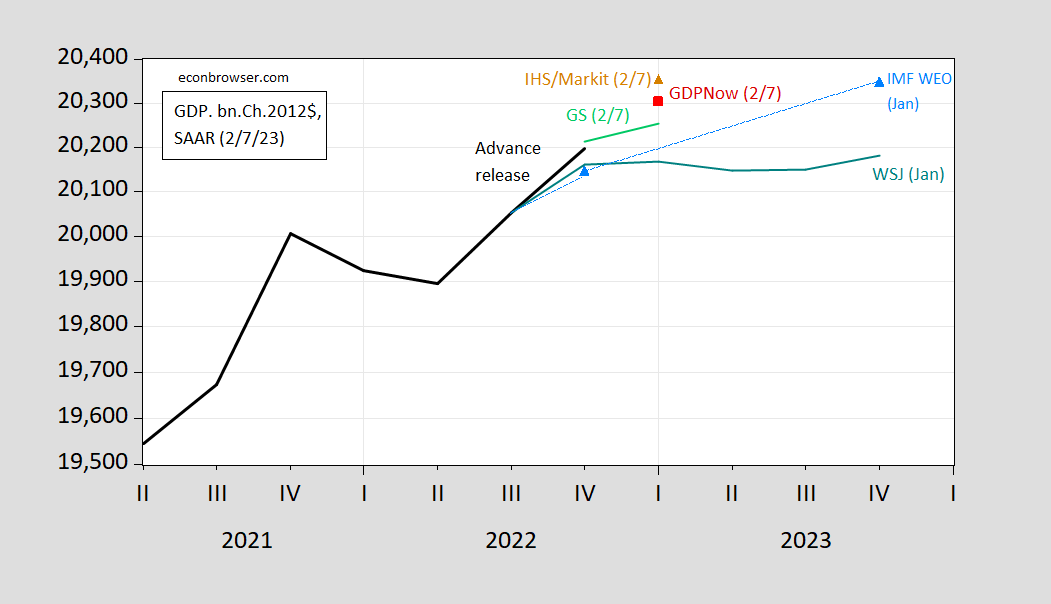

Below are several recent forecasts for first-quarter 2023 GDP, corresponding to the Wall Street Journal’s January average forecast and the IMF’s January 31 World Economic Outlook forecast.

figure 1: GDP (black bold), GDPNow (red squares), IHS Markit/S&P Global (tan triangle), Goldman Sachs (light green line), WSJ January survey mean forecast (green line), IMF WEO forecast (sky blue triangle ). Source: BEA 2022Q4 advance, Federal Reserve Bank of AtlantaIHS-Markit/S&P Global, Goldman Sachs, WSJ January survey, IMF WEO update, and author’s calculations.

These estimates now incorporate the latest available trade data (ie December).

Interestingly, the nowcast/tracking estimates for Q1 growth vary considerably, between 0.8% SAAR (GS) and 3.1% (IHS Markit), with GDPNow at 2.1%. IHS Markit’s baseline is a mild recession starting in Q1 and a recovery in Q3 (so I’m guessing they’re talking about a peak in Q1 and a trough in Q3). Deutsche Bank’s baseline is a mild recession in the second half of 2023, seeing strong job growth against an impending recession. Jan Hatzius of Goldman Sachs said yesterday that there was a 25% chance of a recession in the next 12 months (compared to a consensus of around 65%).

{kind=link}

{kind=link}